Up to date on January twenty sixth, 2023 by Jonathan Weber

At Positive Dividend, we regularly discuss in regards to the deserves of the Dividend Aristocrats. We imagine this unique group of shares broadly has robust manufacturers, constant earnings even throughout recessions, and sturdy aggressive benefits. These qualities enable the Dividend Aristocrats to boost their dividends yearly, whatever the state of the economic system.

Of the five hundred shares comprising the S&P 500 Index, simply 68 qualify as Dividend Aristocrats. You’ll be able to obtain a duplicate of the complete record of all 68 Dividend Aristocrats, full with metrics like dividend yields and P/E ratios, by clicking on the hyperlink beneath:

Annually, we individually assessment all of the Dividend Aristocrats. The subsequent within the sequence is Illinois Instrument Works (ITW). Illinois Instrument Works has a protracted historical past of dividend progress even by means of recessions, which is particularly spectacular given the cyclical nature of its enterprise mannequin. This text will focus on the foremost components for Illinois Instrument Works’ lengthy dividend historical past.

Enterprise Overview

Illinois Instrument Works has been in enterprise for greater than 100 years. It began out all the best way again in 1902. A bunch of inventors shaped with an thought to enhance gear grinding, and Illinois Instrument Works was born.

As we speak, Illinois Instrument Works has a market capitalization of $70 billion and generates annual income of practically $16 billion. Illinois Instrument Works consists of seven segments: Automotive, Meals Tools, Take a look at & Measurement, Welding, Polymers & Fluids, Building Merchandise, and Specialty Merchandise.

These segments have carried out properly in opposition to its friends, which has allowed Illinois Instrument Works to attain “better of breed” standing in its business.

Illinois Instrument Works’ portfolio is concentrated in product segments that every maintain above-average progress potential of their respective markets. The overarching strategic progress plan for Illinois Instrument Works is to constantly reshape its enterprise mannequin, when needed. The corporate steadily makes use of bolt-on acquisitions to develop its attain.

Development Prospects

Whereas 2020 was a really tough 12 months for the worldwide economic system, because of the coronavirus pandemic which weighed closely on financial progress, Illinois Instrument Works continued to generate regular earnings. In 2021, the corporate continued to develop its earnings, and 2022 was even higher. Ultimate outcomes for the fourth quarter haven’t been launched but, however based mostly on the outcomes that Illinois Instrument Works generated in the course of the first three quarters of the 12 months, 2022 was most definitely the strongest 12 months within the firm’s historical past.

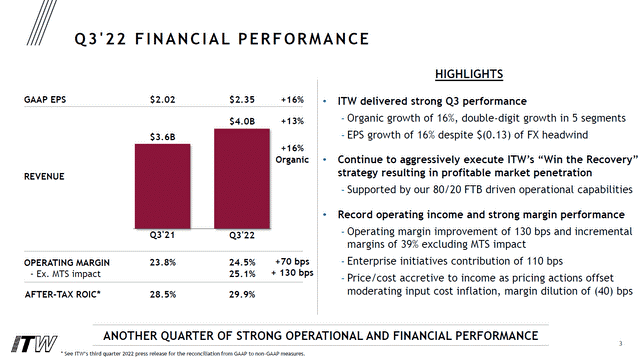

On October 25, 2022 Illinois Instrument Works reported Q3 and first-nine-months outcomes for the interval ending September 30, 2022. For the third quarter, income got here in at $4.0 billion, which was up by a compelling 13% in comparison with the earlier 12 months’s quarter. Optimistic leads to Automotive, Polymers & Fluids and Building Merchandise was offset by declines in Meals Tools, Take a look at & Measurement, Welding and Specialty Merchandise.

Supply: ITW presentation

Third-quarter internet revenue totaled $2.35 per share, in comparison with $2.02 per share within the earlier 12 months’s quarter, which made for a compelling 16% enhance year-over-year.

For the 12 months, Illinois Instrument Works has guided for income of $15.8 billion to $16.0 billion, which makes for a 9% to 10% enhance 12 months over 12 months. Natural progress is seen at 11% to 12%, however foreign money fee actions are a headwind for Illinois Instrument Works as a result of a strengthening US Greenback. Illinois Instrument Works additionally guided for earnings-per-share to fall into a spread of $9.45 to $9.55, which represents a lovely progress fee of 11% to 12% in comparison with what the corporate earned in fiscal 2021.

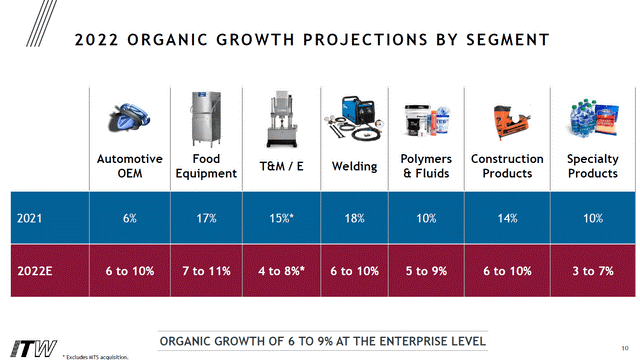

Administration has forecasted that the entire firm’s segments will present stable to engaging natural progress in 2022:

Supply: ITW Presentation

This means that the enterprise setting for the corporate as a complete was constructive throughout 2022, which will be defined by the continued restoration from the COVID-induced financial slowdown.

Sooner or later, Illinois Instrument Works will develop its earnings-per-share by way of a number of drivers. First, ongoing natural enterprise progress ought to add to earnings time beyond regulation. On high of that, the corporate can develop by way of M&A, and effectivity and scale benefits may result in some margin progress as the corporate grows. Final however not least, share repurchases will add to the corporate’s earnings-per-share as properly. General, we anticipate 7% annual EPS progress over the following 5 years.

Aggressive Benefits & Recession Efficiency

Illinois Instrument Works has a big aggressive benefit. It possesses a large financial “moat”, which refers to its skill to maintain competitors at bay. It does this with a large mental property portfolio. Illinois Instrument Works holds over 17,000 granted and pending patents.

Individually, one other aggressive benefit is Illinois Instrument Works’ differentiated administration technique. The corporate has employed a administration course of known as “80/20”. That is an working system that’s utilized to each enterprise line at Illinois Instrument Works. The corporate focuses on its largest and finest alternatives (the “80”) and seeks to remove prices or divest its much less worthwhile operations (the “20”).

On the similar time, Illinois Instrument Works has a decentralized, entrepreneurial company tradition. This additionally units the corporate other than the competitors. Illinois Instrument Works empowers its varied companies with important flexibility, to customise their very own approaches to serving clients in one of the simplest ways attainable.

One potential draw back of Illinois Instrument Works’ enterprise mannequin is that it’s weak to recessions. As an industrial producer, Illinois Instrument Works is reliant on a wholesome world economic system for progress.

Earnings-per-share efficiency in the course of the Nice Recession is beneath:

- 2007 earnings-per-share of $3.36

- 2008 earnings-per-share of $3.05 (9% decline)

- 2009 earnings-per-share of $1.93 (37% decline)

- 2010 earnings-per-share of $3.03 (57% enhance)

That stated, the corporate remained extremely worthwhile in the course of the Nice Recession. This allowed it to proceed rising its dividend annually in the course of the recession, even when earnings declined. And, because of its robust model portfolio, the corporate recovered shortly. Earnings-per-share soared 57% in 2010. By 2011, earnings-per-share surpassed 2007 ranges.

An identical sample was seen in 2020 because the coronavirus pandemic brought about an financial recession. Illinois Instrument Works’ earnings-per-share declined in 2020, however the decline was manageable and the corporate continued to boost its dividend, whereas its earnings-per-share recovered shortly in 2021 and hit a brand new report excessive in that 12 months.

Valuation & Anticipated Returns

Utilizing the present share worth of ~$230 and the midpoint for earnings steering of $9.45 for the 12 months, Illinois Instrument Works trades for a price-to-earnings ratio of 24.3. Given the corporate’s cyclical nature, we really feel {that a} goal price-to-earnings ratio of 19 to twenty is acceptable. That is roughly consistent with the corporate’s 10-year historic common.

In consequence, Illinois Instrument Works is at present overvalued. Returning to our goal price-to-earnings ratio by 2028 would cut back annual returns by round 4% over this time period. Apart from modifications within the price-to-earnings a number of, future returns can be pushed by earnings progress and dividends.

We anticipate 7% annual earnings progress over the following 5 years. As well as, Illinois Instrument Works inventory has a present dividend yield of two.3%.

Whole returns may encompass the next:

- 7% earnings progress

- -4% a number of reversion

- 2.3% dividend yield

Illinois Instrument Works is predicted to return round 5% per 12 months by means of 2028. This isn’t too compelling, which is why we fee Illinois Instrument Works a “maintain” in the present day, though the corporate’s skill to boost dividends by means of a number of recessions is spectacular. The corporate now has 58 consecutive years of dividend progress after rising its dividend once more in 2022.

Ultimate Ideas

Illinois Instrument Works is a high-quality firm and an excellent higher dividend progress inventory. It has a strategic progress plan that’s working properly, and shareholders have been rewarded with rising dividends over 58 years.

The inventory has a good however not spectacular 2.3% dividend yield in the present day. Shares usually are not attractively priced in the mean time, which is why we don’t deem Illinois Instrument Works as a “purchase” at present costs.

Illinois Instrument Works is a basic instance of an excellent firm, however not a inventory to purchase proper now. Regardless of its standing as a Dividend Aristocrat and King, we advise traders look ahead to a greater entry level prior earlier than buying shares of Illinois Instrument Works.

Moreover, the next Positive Dividend databases comprise probably the most dependable dividend growers in our funding universe:

When you’re in search of shares with distinctive dividend traits, take into account the next Positive Dividend databases:

The foremost home inventory market indices are one other stable useful resource for locating funding concepts. Positive Dividend compiles the next inventory market databases and updates them month-to-month:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}