Up to date on February 1st, 2023 by Jonathan Weber

At Certain Dividend, we imagine long-term buyers ought to deal with the highest-quality dividend progress shares. Broadly talking, these are firms with lengthy histories of elevating their dividends, and the aggressive benefits and progress potential to gas continued dividend progress within the years forward.

Due to this fact, we are inclined to steer buyers towards the Dividend Aristocrats, a bunch of 68 firms within the S&P 500 Index, with 25+ consecutive years of dividend will increase. We now have compiled an entire checklist of all Dividend Aristocrats, together with related monetary metrics comparable to dividend yields and price-to-earnings ratios.

You’ll be able to obtain your free checklist of all of the Dividend Aristocrats by clicking on the hyperlink under:

We assessment every of the 68 Dividend Aristocrats yearly. The following inventory to be reviewed on this yr’s version is AbbVie (ABBV).

AbbVie is coming off a multi-year interval of fantastic progress, due to the large success of its flagship product Humira. There are questions concerning the corporate’s future progress as a result of growing competitors for Humira within the U.S. and Europe, however the firm has an formidable plan to proceed its progress in the long term.

This text will talk about AbbVie’s enterprise mannequin, progress potential, and why we price the inventory as a maintain for dividend progress buyers.

Enterprise Overview

AbbVie is a world pharmaceutical large. It has a $260 billion market capitalization, that means it’s a mega-cap inventory.

AbbVie started buying and selling as an unbiased firm in 2013, after it was spun off from fellow pharmaceutical Dividend Aristocrat, Abbott Laboratories (ABT).

AbbVie has generated sturdy progress for the reason that spin-off. Due to success with medication comparable to Humira, the corporate grew income and adjusted EPS by 14% and 18%, respectively, within the 2013 to 2022 time-frame (utilizing the midpoint of administration’s steerage for 2022, as This fall outcomes haven’t been reported but).

Further Useful resource: Inventory Spin-Off Calendar from Inventory Spin-Off Investing.

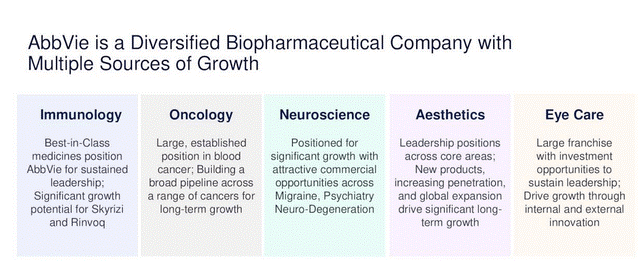

AbbVie is a pharmaceutical merchandise firm that’s centered on a few key remedy areas, together with immunology, oncology, and neurological well being

Supply: Investor Presentation

Due to the expansion it skilled because it was spun off, AbbVie now generates annual income of round $58 billion.

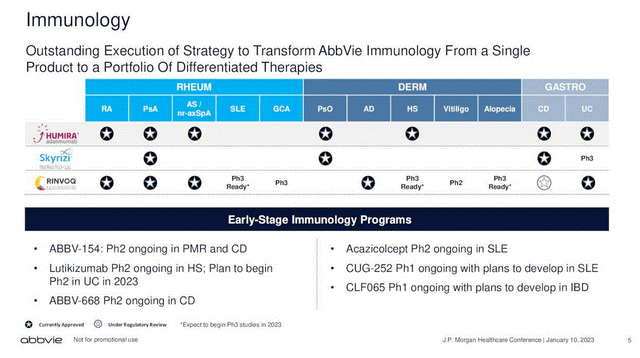

AbbVie’s most essential product is Humira. Humira is an immunology drug that’s used for the remedy of rheumatoid arthritis, Crohn’s illness, and a number of other extra indications, and that has been the top-selling drug on the earth for a few years. The problem for AbbVie is that Humira is now dealing with biosimilar competitors in Europe and the US (since January 2023), which is why Humira’s income contribution will decline in 2023 and past.

AbbVie reported its third-quarter earnings outcomes on October 28, 2022. Quarterly income of $14.8 billion elevated 3% year-over-year, which was primarily the results of progress from new medication comparable to Skyrizi and Rinvoq, which deal with the identical indications Humira treats, and that are seen as an inside substitute of Humira’s income in the long term. Earnings-per-share elevated 29% for the third quarter.

The corporate guides for adjusted EPS to fall into a spread of $13.76 to $13.96 in 2022 — since This fall outcomes haven’t but been launched, we use this as a base case assumption for that yr’s income. On the midpoint of firm steerage, adjusted EPS could be up 9% yr over yr.

Development Prospects

The foremost threat for world pharmaceutical producers is patent loss. When a selected drug loses its patent, the market is often flooded with competitors, particularly for the world’s top-selling merchandise.

For AbbVie, its greatest threat is the competitors about to hit its flagship drug Humira, a multi-purpose drug that’s used to deal with rheumatoid arthritis, plaque psoriasis, Crohn’s illness, ulcerative colitis, and extra.

Humira at one level generated over half of AbbVie’s annual gross sales. Lack of patent exclusivity within the US in early 2023 is a big overhang. AbbVie expects its complete gross sales will decline in 2023 because of this — revenues are seen declining by round 7% this yr. On the identical time, AbbVie expects to return to gross sales progress in 2024 on the again of power from different portfolio property.

Happily, the corporate ready for the lack of patent exclusivity on Humira, by investing closely in new merchandise in addition to acquisitions to spice up its progress. For instance, AbbVie has seen sturdy progress from two of its oncology medication, Imbruvica and Venclexta.

Rinvoq and Skyrizi are two extra merchandise that signify long-term progress catalysts. These immunology medication are used to deal with comparable indications relative to Humira, however promise higher effectivity and fewer unwanted effects:

Supply: Investor Presentation

AbbVie has guided for mixed revenues of greater than $21 billion from Rinvoq and Skyrizi a few years from now, which might make them greater than Humira at its peak.

AbbVie’s $63 billion acquisition of Allergan additionally stays a supply of future enterprise and earnings progress. Allergan’s flagship product is Botox, which diversifies AbbVie’s portfolio with publicity to world aesthetics and neurological indications. Each of those markets proceed to expertise progress, thereby permitting AbbVie to learn from rising spending in these areas.

Debt discount and share repurchases are different drivers that would affect AbbVie’s earnings-per-share positively in the long term. However as a result of near-term headwinds from the Humira patent loss, we imagine that earnings-per-share progress could possibly be considerably subdued, within the 3% vary, over the approaching 5 years.

Aggressive Benefits & Recession Efficiency

A very powerful aggressive benefit for AbbVie, and every other pharmaceutical firm, is its patent portfolio. Pharmaceutical giants have to spend closely to innovate new medication and therapies when one among their blockbusters loses patent safety.

Analysis and improvement bills totaled greater than $7 billion yearly in recent times, not but together with AbbVie’s acquisitions of extra pipeline property from different firms. Due to that heavy spending on new therapies, AbbVie is well-positioned in progress markets comparable to oncology and immunology.

AbbVie was not a standalone firm over the past monetary disaster, so there isn’t any recession observe document, however since sick individuals require remedy whether or not the financial system is powerful or not, it’s extremely possible that AbbVie would proceed to carry out effectively throughout a recession. The COVID pandemic has not impacted AbbVie negatively, as the corporate hit new document income in 2020, 2021, and 2022.

Even when AbbVie’s earnings had been to say no barely in a recession, the dividend ought to stay safe. AbbVie’s trailing dividend payout ratio is simply 43%, in any case.

Valuation & Anticipated Returns

AbbVie is predicted to have generated adjusted EPS of $13.86 for 2022, on the midpoint of steerage. At this EPS stage, the inventory is presently buying and selling for a price-to-earnings ratio of 10.5.

AbbVie is valued significantly under the S&P 500 Index. As well as, AbbVie is undervalued right this moment when in comparison with its historic common PE of round 12. Our honest worth estimate for AbbVie is a price-to-earnings ratio of 10.0, as a result of growing leverage from the Allergan acquisition and the Humira patent exclusivity that expired within the U.S. in January, which is able to most definitely result in decrease gross sales this yr.

We thus view AbbVie as barely overvalued. A compressing P/E a number of may lower shareholder returns by roughly 1% per yr over the following 5 years.

As well as, we anticipate annual earnings progress of three% by the following 5 years. Lastly, the inventory has a present dividend yield of 4.1%. In complete, we anticipate annual returns of round 6% per yr over the following 5 years, making AbbVie inventory a maintain.

Remaining Ideas

AbbVie is a really high-quality enterprise, with a powerful pharmaceutical pipeline and long-term progress potential. Additionally it is a shareholder-friendly firm that returns extra money circulation to buyers.

AbbVie faces a big problem in changing misplaced Humira gross sales because it faces competitors within the U.S. and Europe. Happily, the corporate has ready for this with heavy R&D investments. From this, it has created a big portfolio of latest merchandise that ought to enable AbbVie to begin to develop once more in 2024 and past as soon as the Humira patent expiration has been lapped.

With anticipated returns of 6% per yr going ahead, together with a 4.1% dividend yield, we imagine AbbVie is a maintain for long-term worth buyers and revenue buyers.

In case you are serious about discovering high-quality dividend progress shares appropriate for long-term funding, the next Certain Dividend databases might be helpful:

The foremost home inventory market indices are one other strong useful resource for locating funding concepts. Certain Dividend compiles the next inventory market databases and updates them month-to-month:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}