Spencer Platt

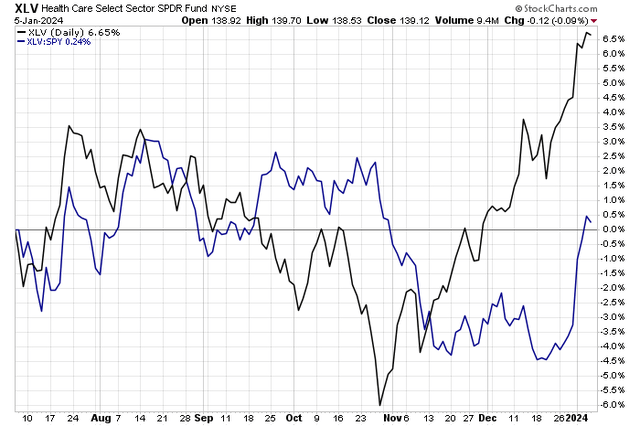

The Well being Care sector was one to usually keep away from in 2023. Except you had been considerably chubby (no pun meant) in shares of Eli Lilly (LLY) and Novo Nordisk (NVO), it’s possible that you simply underperformed the S&P 500 given the Well being Care Choose Sector SPDR ETF’s (XLV) weak returns. Has the tide turned in favor of defensive Well being Care equities? XLV has crushed SPY by about 5 share factors simply since mid-December.

I see extra upside forward in CVS Well being (NYSE:CVS). Following steerage that was reiterated final week and with a brand new everlasting CFO on the helm, the corporate seems undervalued to me whereas the technicals have turned extra favorable.

Healthcare Shares Spring Again to Life

StockCharts.com

In keeping with Financial institution of America International Analysis, CVS Well being Company offers well being providers within the US. It operates by Well being Care Advantages, Pharmacy Companies, and Retail/LTC segments and is among the many largest Well being Care corporations within the nation, offering retail, mail, and specialty pharmacy meting out providers and pharmacy advantages. It is likely one of the most vertically built-in publicly traded Well being Care corporations.

The Rhode Island-based $105 billion market cap Well being Care Companies trade firm throughout the Well being Care sector trades at a low 9.5 ahead 12-month non-GAAP price-to-earnings ratio and pays an above-market 3.3% dividend yield as of January 5, 2024. Forward of earnings in early February, the inventory has a low implied volatility share of twenty-two% whereas its quick curiosity is modest at simply 1.2%.

Again in November, CVS reported a powerful Q3 report. Quarterly non-GAAP EPS verified at $2.21, topping the Wall Road consensus expectation of $2.13 whereas income of $90 billion, up almost 11% from year-ago ranges, beat by a whopping $1.6 billion. For its full-year steerage, the administration staff issued its adjusted EPS outlook of $8.50 to $8.70 vs. $8.75 consensus whereas confirming money move from operations within the $12.5 billion to $13.5 billion vary. Shares wobbled following the report as segment-level performances had been combined. Its Well being Companies and Pharmacy & Client Wellness EBIT quantities had been sturdy, however Healthcare Advantages ensured some softness as a result of the next medical advantages ratio.

Then simply final week, the administration staff reaffirmed its FY 2023 and FY 2024 steerage to be within the higher finish of the $8.50 to $8.70 vary for FY 2023. What was bullish was that it introduced a $3 billion accelerated buyback program and appointed a everlasting CFO. These indicators of stability are encouraging, although dangers from rising competitors within the pharmacy advantages area stay together with opioid-related litigation dangers.

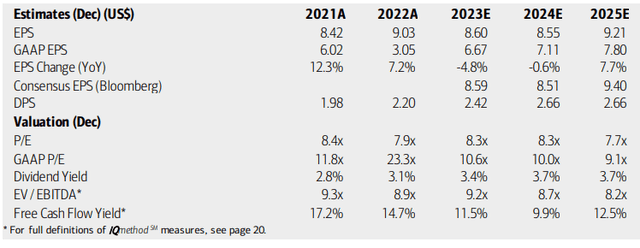

On valuation, analysts at BofA see earnings falling simply barely this yr earlier than per-share revenue progress returns in 2025. The present consensus forecast, per Looking for Alpha, reveals that 2024 EPS will fall by lower than 1% following final yr’s flat earnings progress. With gross sales advancing 2% this yr and 6% within the out yr, some working leverage is anticipated by 2025.

Dividends, in the meantime, are forecast to rise to carry at $2.66 yearly (a $0.665 quarterly payout comes on Thursday, February 1). With very low working and GAAP earnings multiples, the inventory is priced fairly pessimistically. Furthermore, CVS encompasses a low EV/EBITDA ratio, a number of turns underneath the common of the S&P 500 whereas its free money move yield could be very excessive.

CVS: Earnings, Valuation, Dividend, Free Money Circulation Forecasts

BofA International Analysis

If we assume working earnings per share of $8.70 over the subsequent 12 months and apply the inventory’s 5-year historic earnings a number of of 9.8 then CVS ought to commerce close to $85. That’s about what I figured in my earlier evaluation, however contemplating that the inventory trades at a major low cost to its long-term common price-to-sales ratio, together with CVS having each a excessive dividend yield and strong free money move, there are upside dangers to my valuation ought to earnings proceed to return in robust – CVS has topped estimates in every of the final 12 experiences.

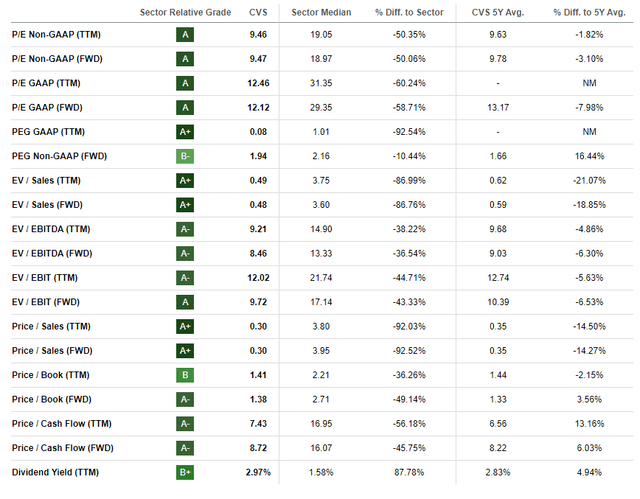

CVS: Compelling Valuation Metrics

Looking for Alpha

In comparison with its friends, CVS options among the many prime valuation grades by Looking for Alpha, although latest progress developments have been weak. Nonetheless, with earnings rebound anticipated beginning subsequent yr, there’s motive for optimism when it comes to its valuation a number of going ahead. Furthermore, CVS options very robust absolute and relative profitability developments whereas its share-price momentum has turn out to be a lot more healthy over the previous a number of months – I’ll element the technicals intimately later within the article. Lastly, EPS revisions have been combined, and I wish to see a quicker flip in earnings momentum.

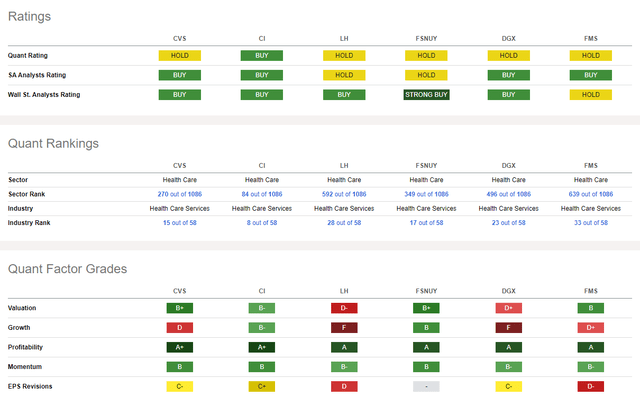

Competitor Evaluation

Looking for Alpha

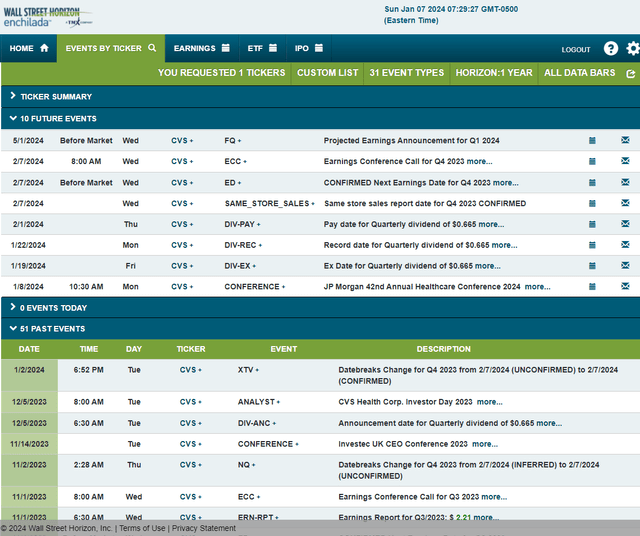

Trying forward, company occasion knowledge offered by Wall Road Horizon reveals a confirmed This autumn 2023 earnings date of Wednesday, February 7 BMO with a convention name instantly after the outcomes hit the tape. You’ll be able to pay attention stay right here. CVS additionally points same-store gross sales inside that report. Close to-term, the administration staff is anticipated to current at one of the crucial necessary trade conferences of the yr: the JP Morgan 42nd Annual Healthcare Convention 2024 from January 8 by 11. Each Karen S. Lynch, President, CEO, Thomas F. Cowhey, CFO are anticipated to talk.

Company Occasion Threat Calendar

Wall Road Horizon

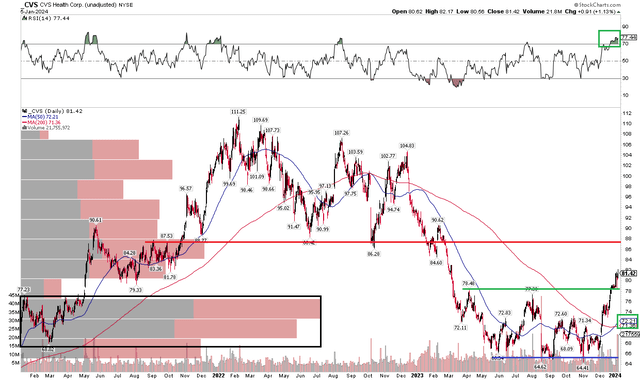

The Technical Take

Final yr, I famous that the higher $60s was more likely to be necessary help for CVS shares. Certainly, the bulls confirmed up round the place we might anticipate. Discover within the chart beneath that CVS met consumers just a few occasions above $64 in 2023. The actually bullish transfer then got here late in This autumn. The inventory jumped from beneath $70 to the mid-$70s in brief order, rising above its long-term 200-day shifting common for the primary time since late 2022. The surge got here on an uptick in quantity, too. Then, only a few periods in the past, the shorter-term 50-day shifting common rallied by the 200dma in what technicians deem a bullish golden cross sample.

Additionally, check out the place the inventory could go subsequent following a breakout by the mid-$70s. With shares at 10-month highs, serving to to steer the S&P 500 since October, I see resistance within the higher $80s. There’s truly not an entire lot of quantity by worth from right here to there, so squeaking out one other 10% upside appears doable. Assist is seen at former resistance, which might be within the $77 to $78 zone. For now, with the RSI momentum oscillator at very excessive marks, a near-term consolidation would make sense, however that may be a mere pause within the development of bigger diploma, which seems larger right this moment.

Total, CVS held help properly final yr and now seems as a market chief.

CVS: Downtrend Reversed, Shares Rally Via Key Resistance, $88 Subsequent Cease

StockCharts.com

The Backside Line

I reiterate my purchase ranking on CVS Well being. I see shares as nonetheless undervalued following a major leap in its inventory worth since late final yr.

{kind=link}