Lawrence Glass

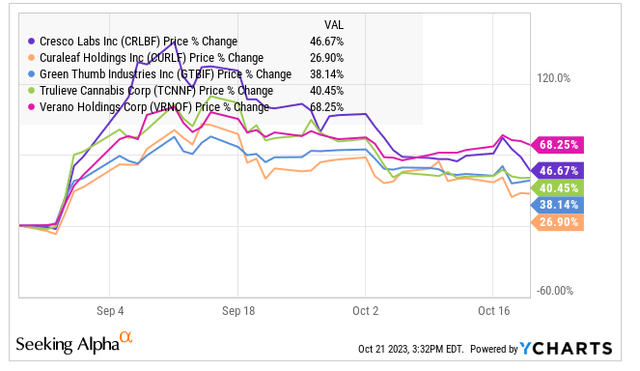

I’ve been damaging all yr on Curaleaf (OTCPK:CURLF). Most not too long ago, forward of the potential rescheduling, I predicted that it might break $2 to the draw back when the inventory was at $2.90 in late August. I truly referred to as out $2.20 as my year-end goal. The inventory has rallied on the potential excellent news, closing at $3.68, up 27%. In that article, I referred to as out its excessively excessive relative valuation, and it has lagged all of its massive MSO friends:

YCharts

For the reason that finish of 2022, the inventory has declined 14.4%, rather less than the International Hashish Inventory Index. In mid-January, I referred to as it out for its excessive relative valuation. The inventory has declined 8.2% since then.

Whereas the inventory could not hit that $2 space that I used to be predicting, it’s nonetheless very costly relative to its friends. In at this time’s piece, I evaluate the outlook, focus on the valuation and assess the chart.

Wanting Forward

In late August, analysts, based on Sentieo, had been in search of 2023 income to be $1.36 billion, with 2024 income projected to develop to $1.47 billion. Now they count on 2023 income to nonetheless develop 2% to $1.36 billion, however the 2024 outlook is a bit much less robust, with analysts projecting 6% development to $1.44 billion. Adjusted EBITDA is anticipated to shrink 1% in 2023 to $301 million and to develop 20% in 2024 to $361 million.

For forming year-end targets, I consider the 2025 estimates will play a key position. Proper now, solely 4 analysts have offered them. They’re projecting that income will develop 21% to $1.74 billion with adjusted EBITDA rising 45% to $522 million, a 30% margin that sounds too excessive. In 2021, the prior peak annual margin, the corporate had an adjusted EBITDA margin of 25%

In fact, how rescheduling performs out will impression the corporate’s money move, however it’s going to haven’t any impression on the EBITDA as a result of taxes are excluded. If the DEA follows the advice from the HHS to maneuver hashish from Schedule 1 to Schedule 3, the onerous tax 280E would cease. 280E forces hashish firms to pay tax on gross earnings quite than internet earnings. For 2024, analysts presently undertaking diluted EPS of simply $0.09 per share.

One factor that has modified since my evaluate in August after the Q2 report is that the corporate has utilized for itemizing on the TSX. I do not suppose that this may matter a lot if the corporate is profitable.

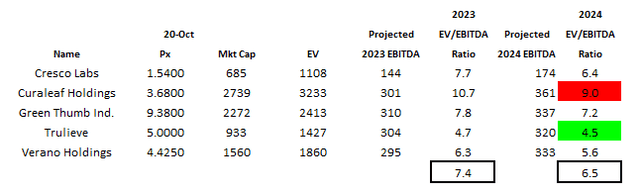

Comparatively Costly

Curaleaf trades at an enterprise worth to adjusted EBITDA for 2023 of 10.7X, which appears low relative to its historical past. It trades at 9.0X the projected 2024 adjusted EBITDA.

Whereas the valuation appears low, it’s excessive relative to its 4 friends:

Alan Brochstein, utilizing Sentieo

As I look out to the top of 2024, about 14 months from now, I feel that Curaleaf might commerce at 12X projected adjusted EBITDA if 280E goes away, nevertheless it may pull again to 6X if not. The corporate has a whole lot of debt excellent, even after the latest capital elevate. On the present worth, I assume that the share-count will probably be boosted by 7.9 million shares, because the $2.89 choices are within the cash. That money would cut back the web debt to $494 million.

I feel that the analysts are too excessive of their estimate of 2025 adjusted EBITDA, however I’m utilizing their estimate nonetheless. The inventory might attain $7.75 if 280E will get worn out, nevertheless it might additionally fall to $3.55 at 6X. Once more, I feel that the projection is just too excessive, so the worth might be decrease. I proceed to consider that the inventory might take a look at $2.

I proceed to seek out the steadiness sheet to be regarding. The corporate has tangible fairness that’s fairly damaging at -$722 million on the finish of Q2. The latest capital elevate and the potential choices train brings this to -$687 million. The corporate might want to elevate capital in my opinion as a result of massive debt.

One other concern is that the AdvisorShares Pure US Hashish ETF (MSOS) owns a whole lot of the inventory, far more than it ought to in my opinion at 19.8% of the fund. Solely GTI, at 24.2%, is bigger. The highest 6 holdings of MSOS whole 83% of it. The ETF has seen some inflows not too long ago after seeing outflows in late 2022 and into 2023. If it suffers redemptions once more, it might want to promote CURLF.

The Chart

Curaleaf had an enormous bounce not too long ago, doubling in only a few weeks, nevertheless it has misplaced most of these positive factors:

Charles Schwab

I see help simply above $3 after which beneath it. I see resistance simply above $4.

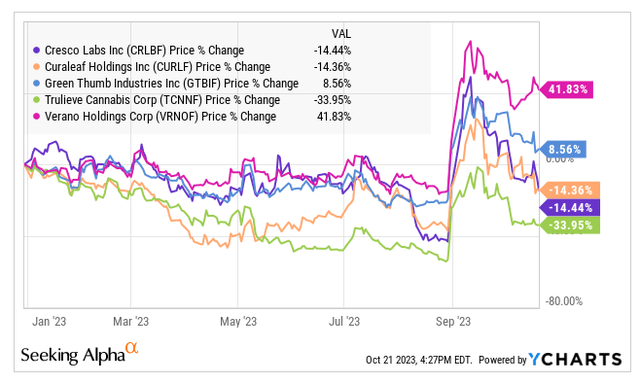

Above, I confirmed how the chart has in comparison with its 4 massive friends since late August. Right here is the year-to-date perspective:

YCharts

Cresco Labs (OTCQX:CRLBF), which I favor, and Trulieve (OTCQX:TCNNF), which I additionally favor, have misplaced extra, whereas Verano (OTCQX:VRNOF) and Inexperienced Thumb Industries (OTCQX:GTBIF) have carried out higher and are up year-to-date.

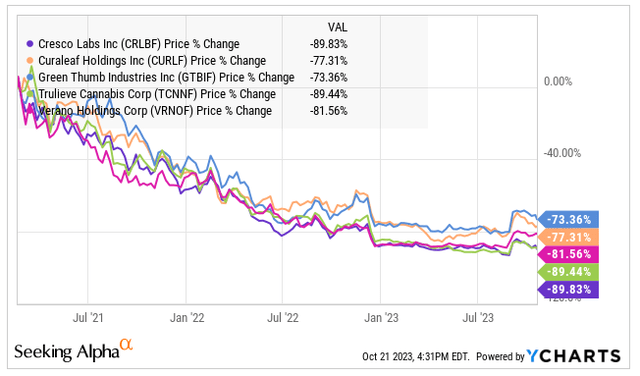

For the reason that peak in February 2021, Curaleaf, down 77%, has carried out higher than all however GTI:

YCharts

Conclusion

Curaleaf has declined quite a bit over the previous few years and seems to be low-cost. It’s comparatively costly, although, to its friends. With the elimination of 280E, the inventory would doubtless go up. If 280E stays, the inventory will doubtless decline.

Traders who wish to take part within the hashish market can take much less threat with CURLF friends or different varieties of hashish firms and probably make larger returns too. I’ve written about some Canadian LPs that commerce beneath tangible e book worth and have a whole lot of money and no debt. One in all these federally authorized firms trades at a decrease enterprise worth to projected adjusted EBITDA a yr forward too. I additionally discover some higher concepts among the many ancillary firms.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please concentrate on the dangers related to these shares.

{kind=link}