Sky_Blue

Funding Thesis

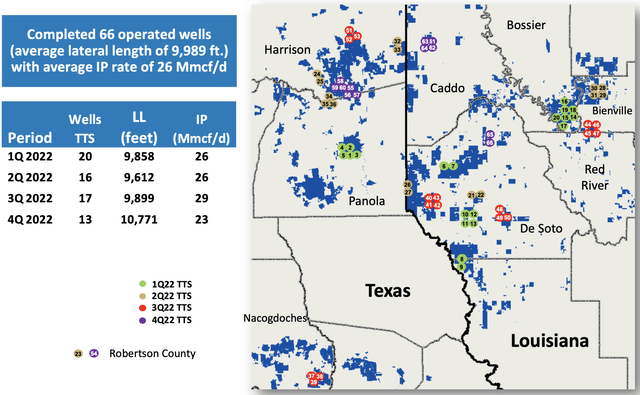

Comstock Sources (NYSE:CRK) is a Haynesville Basin pure-play pure fuel producer carefully situated to the Gulf Coast hall and close to a number of giant LNG (Liquified Pure Gasoline) terminals. CRK operates 1,600 wells throughout 372,000 acres with a mean lateral size of 9,989 ft.

For all of FY22 CRK generated $673 million in free money stream from operations. CRK moreover operates the trade’s lowest working price construction, which drives its very excessive 83% EBITDAX margin. CRK intends to retain the present dividend quantity of $0.50 per yr within the present pricing surroundings.

As a result of its excessive FCF technology, and low prices, we consider that CRK is an efficient alternative for dividends. We anticipate the droop in pure fuel costs to be momentary, and thus additionally assume CRK could be a sensible choice for capital appreciation.

Estimated Honest Worth

EFV (Estimated Honest Worth) = E24 EPS (Earnings Per Share) occasions P/E (Worth/EPS)

EFV = E24 EPS X P/E = $4.25 X 5.0 = $17.60

We’ve got used a low-end P/E throughout the 4-10x vary that oil and fuel exploration firms often fall. With its progress, CRK might simply commerce on the excessive finish.

|

Comstock Sources |

E2023 |

E2024 |

E2025 |

|

Worth-to-Gross sales |

1.3 |

1.2 |

1.2 |

|

Worth-to-Earnings |

2.3 |

3.3 |

2.7 |

Operations

Manufacturing was at 1,445 MMcfe/d (hundreds of thousands of cubic foot equal per day) of pure fuel in 4Q22, with manufacturing rising at a 21% 3-year-CAGR. Yr over yr, there was a 9% enhance in day by day manufacturing, with a much more favorable pricing surroundings permitting for higher monetary outcomes.

FY23 quarterly manufacturing is anticipated to be at the very least the identical as in 4Q22 however might go as excessive as 1,550MMcfe/d.

CRK is an advantageous geographic location, with direct entry to gulf coast markets, promoting roughly 71% of pure fuel within the native geographic space. This consists of 17% of manufacturing immediately bought to LNG shippers. In 4Q22, the typical realized worth was $5.57/Mcf at 47% of manufacturing hedged. The $5.57/Mcf quantity is disappointing given the 3Q22 worth realization of $7.72/Mcf, however it’s nonetheless a 6.5% enhance yearly. Hedging is decrease in FY23, with solely 30% of manufacturing hedged to date at $3.00/Mcf.

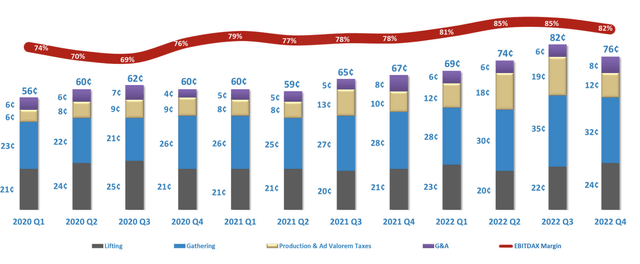

For FY22, the typical lateral size of wells was 9,989 ft. Complete D&C prices (drilling and completion) averaged $1,425 per lateral foot drilled over the identical interval. This interprets to only over $1 billion in D&C prices. 4Q22 steering is anticipated to be increased than the yearly common of 1,400 MMcf/d, at roughly 1,470 MMcf/d. All in prices are anticipated to be equal to FY22, which had been $1.63 per Mcf (1000’s of cubic ft). Nicely-level money working prices are $0.82 per Mcf.

We do not anticipate a block-busting drilling enlargement to happen in FY23. Nevertheless, it’s actually price noting that the Western Haynesville enlargement into Robertson County had an IP (preliminary manufacturing) of 42 MMcf/d. Whereas IP numbers path off as soon as the effectively reaches full manufacturing, that is nonetheless a lot increased than the typical IP of 25 MMcf/d CRK often sees within the different fields. On the 4Q22 earnings name, administration mentioned it was too early to take a position on potential output or prices for the world.

CRK 2022 Drilling Outcomes Map (4Q22 CRK report)

Pure Gasoline Costs

BuildingBenjamins, EIA

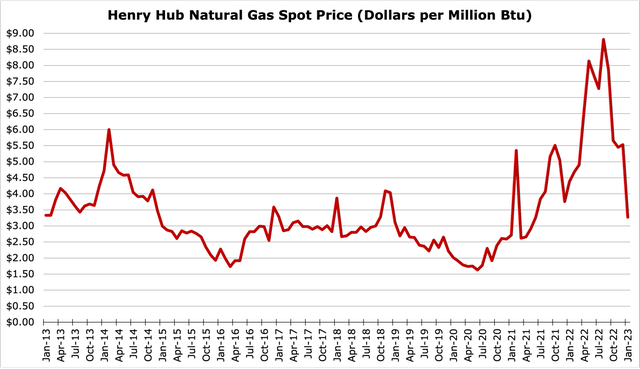

Freeport LNG terminal being closed after an explosion broken it over the summer time has harm export quantity and US home pure fuel pricing. The Freeport terminal accounts for round 20% of US LNG Exports. Re-opening was anticipated to restart in early February, and the primary tankers arrived in early February. Freeport’s operator hopes to hurry up regulatory approval for restarting business operations, at 1/4 capability. The prevailing sentiment now could be that Freeport can be prepared for full export capability once more in 2H23.

We anticipate pure fuel costs to recuperate by the top of this yr, 2023. We estimate a worth at or above $5.00/MMBtu with seasonal surges because the climate will get colder within the latter a part of the yr. With demand surging, international progress in LNG transport capability can be restricted in comparison with earlier years. FY23 enlargement to the worldwide LNG chain is anticipated to be the bottom since 2013, including just one Bcf/d in capability. On the identical time, home consumption of LNGs is anticipated to surge to file highs in January 2024. The EIA estimates a home pure fuel demand of 86 Bcf/d, with pure fuel remaining roughly 40% of US electrical technology into 2024. Thus, it’s unlikely to us that the 70% worth collapse of pure fuel within the final 6 months will final for very lengthy.

US LNG is in demand because of the European Vitality Disaster. LNG exports have reached international highs, with a mean of 11.8 Bcf/d (billion cubic ft per day). This can be a 10% enhance from 2021 and a 70% enhance from 2019. In January of FY23 Europe skilled traditionally excessive winter temperatures, which considerably dampened the demand for pure fuel. This dampening pushed fuel costs again right down to what they had been earlier than the invasion of Ukraine. Nevertheless, pure fuel exports are nonetheless anticipated to extend but once more because the struggle in Ukraine drags on and as an extra 8-10 Bcf/d in anticipated US LNG capability comes on-line by 2026. This demand needs to be creating a robust again for pure fuel costs.

Financials

CRK’s excessive free money stream technology allowed the retirement of $506 million of long-term debt, to 1.1x debt-to-EBITDA. The remaining debt on the books matures in 2029.

Working Prices Per Mcfe / EBITDAX Margin (CRK 4Q22 Report)

Restricted hedging of solely 47% of manufacturing and favorable pricing allowed CRK to take part within the pure fuel worth surge midyear. 4Q22 Yr over yr, FCF elevated by 22% to 129 million and EPS by 184% to $1.05. Pricing is far decrease than in the course of FY22, and FCF will in all probability decline in early 2023. However, as now we have mentioned beforehand, that is prone to be a short lived droop.

Danger and Conclusion

Worth is probably the most obvious threat because the pure fuel worth per MCF has fallen to an unfavorable stage under $3. If the worth had been to remain at these ranges as hedges roll off, FCF would get crushed leading to gradual or no further debt compensation. Nevertheless, debt will not be actually an issue given how a lot was repaid in FY22. At present, CRK has plans to retain the dividend even in a cheaper price surroundings.

Traditionally when firms had excessive costs and masses of cash stream, they invested closely and with leverage. The previous couple of down cycles bankrupted many firms and made the survivors extra conservative. Therefore within the combination, there may be not sufficient capital going to growth that means provide is not going to overshoot demand and excessive costs are extra sustainable. An antagonistic regulatory surroundings has additionally starved the trade of capital. Larger costs are the end result and can make the trade much less increase and bust. Dividend funds as an alternative of Capex are drawing the ire of Washington however are favorable to shareholders as using capital for dividends makes excessive costs extra sustainable and thus the dividends extra sustainable than previous cycles.

CRK is immensely low cost, doubtless due to the 70% droop in pure fuel costs over the past 6 months. CRK generates an enormous quantity of free money, has a geographically advantageous place, and has a robust steadiness sheet and sector-best price construction.

{kind=link}