DNY59

The Citi Funding Thesis Is Nonetheless Enticing Right here

Now we have beforehand coated Citigroup Inc. (NYSE:C) in March 2023, throughout the worst of the banking disaster. The financial institution inventory sell-off earlier this yr triggered a drastic plunge in its inventory worth to the pandemic and eight Yr lows, suggesting a extremely engaging risk-reward ratio at the moment.

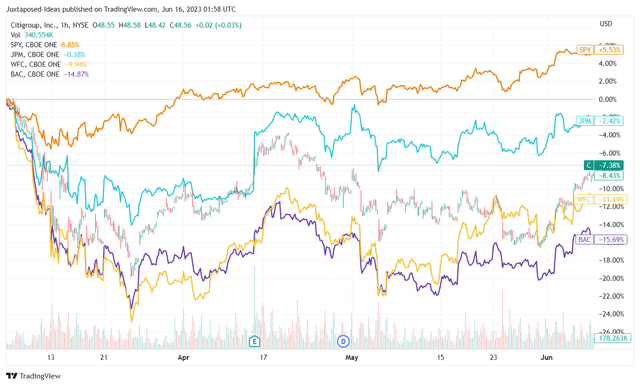

C 3M Inventory Value

Buying and selling View

True sufficient, C has recovered by over +12% since then, as equally noticed with different large financial institution shares, comparable to JPMorgan (NYSE:JPM) at over +14%, Financial institution of America (NYSE:BAC) at over +8%, and Wells Fargo & Firm (NYSE:WFC) at over +16%. Whereas the restoration will not be full but, this cadence is considerably aided by the optimism surrounding the SPY bull run of over +20% because the October 2022 backside.

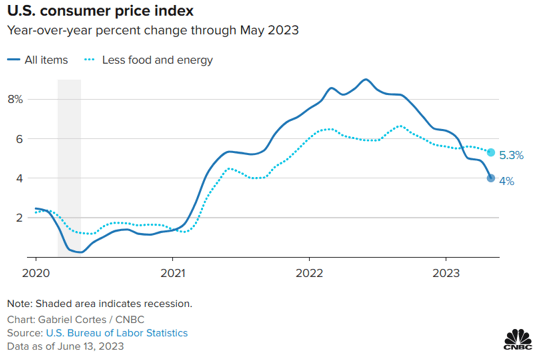

The US Shopper Value Index By Might 2023

CNBC

The Might 2023 CPI has additionally moderated to 4% YoY, down from the 9% reported in June 2022. On account of the optimistic improvement, the Fed lastly paused the speed hike in June 2023, after 10 consecutive will increase in 15 months.

Whereas Jerome Powell could have guided to 2 extra price hikes in 2023, triggering an approximate terminal price of 5.50% and 5.75%, we’re not overly involved for now, because the forward-looking inventory market has already priced in an eventual pivot anticipated someday in 2024.

Naturally, all of it is determined by C’s efficiency within the upcoming FQ2’23 earnings name by mid-July 2023, since it could be extra telling of the financial institution’s efficiency after the Silicon Valley Financial institution meltdown. Then once more, we have now already gathered optimistic hints from the administration’s commentaries to this point.

For instance, the financial institution reiterated $1.03T of accessible liquidity sources (-1.4% QoQ/ +7% YoY), together with $584.3B of HQLA (+1.5% QoQ/ +8.1% YoY) and 120% of LCR (+2 factors QoQ/ +4 YoY) by the newest quarter.

Effectively, it stays to be seen if C could recoup the $5B of uninsured deposits beforehand made with First Republic Financial institution, a query that could be answered throughout JPM’s upcoming earnings name.

Both approach, the previous’s well-diversified portfolio stays extremely strategic in making certain the stickiness of its multinational consumer base, as greatest highlighted by Jane Fraser, CEO of C, within the latest earnings name:

Most of those deposits are significantly sticky as a result of they sit in working accounts which might be totally built-in into how our multinational shoppers run their companies around the globe from their payrolls, their provide chains, their money and liquidity administration. 80% of those deposits are with shoppers who use all three of our built-in providers: funds and collections, liquidity administration and dealing capital options.

The information that we combination from these deposits and their associated flows is key to how our shoppers handle their effectivity, danger and compliance. And this drastically will increase our deposit stickiness. It is also why almost 80% of those deposits are from consumer relationships which might be 15 years previous or extra. (Searching for Alpha)

That is on prime of C’s sustained efforts in enhancing the working effectivity to 68.6% (-12.4 factors QoQ/ -3.5 YoY) and adj ROTCE to 9.3% (ex divestiture) by the newest quarter (+0.4 factors QoQ/ +0.3 YoY). Whereas there should be an important distance from pre-pandemic ranges of 64.2% and 12.1% in FY2019, respectively, the development from FY2022 ranges of 73.3% and eight.9% is noticeable certainly.

A lot of the success is attributed to the financial institution’s efforts in divesting higher-cost companies, such because the latest exit from 14 client banking nations, and optimizing working bills each in headcount and capex depth, whereas equally simplifying its administration positions.

Maybe that’s the reason the CFO has lately reiterated FY2023 revenues of $78.5B (+11.2% YoY) and EBIT of $24.5B (+1.9% YoY) on the midpoint, suggesting an working effectivity of 68.7% (-4.6 factors YoY). Regardless of being dragged down by divestitures bills, FDIC insurance coverage prices, and one-time prices from the headcount reductions, the power of the administration’s execution has been evident certainly.

Due to this fact, we stay assured that C could ultimately obtain its medium-term working effectivity of ~60% and ROTCE of 11.5% on the midpoint, particularly aided by the deliberate Banamex IPO in 2025, because the macroeconomic outlook normalizes and working prices are optimized.

In the meantime, with the rates of interest remaining excessive and inflationary stress nonetheless elevated, we might even see the delinquency charges, sadly, rise because the financial institution’s charge-offs enhance.

For instance, C already reported a rise within the complete client mortgage delinquencies, that are 90+ days late at $2.37B (+10.2% QoQ/ +30.9% YoY), with a ratio of 0.76% (+0.08 factors QoQ/ 0.13 YoY) by the newest quarter. That is on prime of the rising Web Credit score Losses and Ratios to $1.28B (+20.7% QoQ/ +52.1% YoY), with a ratio of 1.43% (+0.26 factors QoQ/ 0.46 YoY).

As well as, the financial institution additionally made a better allowance for credit score losses on complete loans at -$17.16B (+1.1% QoQ/ +11.5% YoY), with a share of two.65% (+0.05 factors QoQ/ +0.30 YoY).

Whereas a few of these numbers should be decrease than the FY2019 Shopper Mortgage Delinquencies ratio of 0.98% and Web Credit score Losses Ratios of two.49%, C traders should additionally be aware that the allowance for credit score losses ratio has risen from the 1.84% reported then.

Because of this, whereas the elevated rate of interest atmosphere could have triggered the financial institution’s larger web curiosity revenue of $13.34B (in line QoQ/ +22.7% YoY), effectively balancing the credit score losses to this point, it stays to be seen how lengthy these macro headwinds could final, probably placing stress on its execution within the close to time period.

So, Is C Inventory A Purchase, Promote, or Maintain?

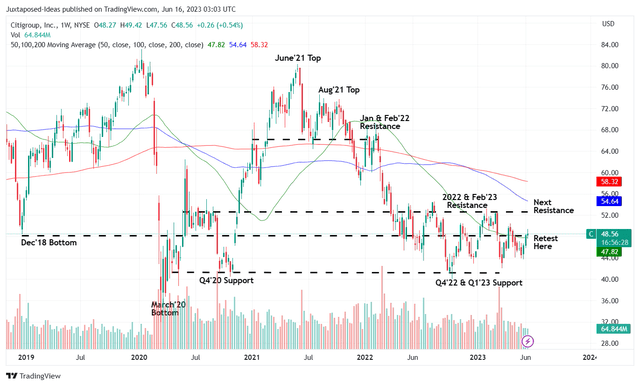

C 5Y Inventory Value

Buying and selling View

C appears to be retesting its earlier resistance stage of $49 within the close to time period, which is probably going a non-issue because of the bullish market pattern to this point. Because of this, we might even see the inventory additional rally to the subsequent resistance stage of $56s and settle there.

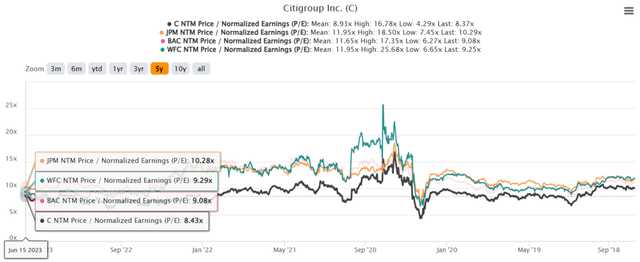

C 5Y P/E Valuations

S&P Capital IQ

C inventory can also be buying and selling at an NTM P/E of 8.37x, down from its 5Y imply of 8.93x and nonetheless average in comparison with its large financial institution friends, suggesting its engaging risk-reward ratio.

Primarily based in the marketplace analysts’ FY2025 adj EPS projection of $6.65 (ex-Banamex IPO) and the inventory’s NTM P/E of 8.37x, we’re nonetheless taking a look at a worth goal of $55.66, suggesting a good upside potential of +15.5% from present ranges.

Due to this fact, we proceed to price C inventory as a BUY right here.

{kind=link}