Vladimir_Timofeev/iStock through Getty Pictures

Ceragon Networks Ltd (NASDAQ:CRNT) has carved a distinct segment in wi-fi backhaul options, a sector that ought to profit from the appearance of 5G. For my part, this positions CRNT’s numerous choices, from voice providers to IoT connectivity, to revenue from secular tailwinds. CRNT’s current monetary knowledge signifies a promising margin enchancment. Moreover, particulars from their most up-to-date earnings name recommend they’re gearing up for brand spanking new product launches, aligning with the anticipated world wi-fi backhaul market progress. Nevertheless, the broader telecommunications trade has challenges, particularly with consolidation. I consider CRNT’s comparatively modest dimension would possibly problem navigating this panorama. General, primarily based on my valuation evaluation, CRNT’s truthful worth is round $161.3 million. Given this evaluation, I believe that its present market valuation would not supply a very attractive funding proposition, main me to take care of a impartial stance on CRNT.

Enterprise Overview

Ceragon Networks operates within the Know-how and Communications trade, with a distinct segment in wi-fi backhaul options. These options are designed to help mobile operators and numerous service suppliers in enhancing their networks, particularly as we transition into the 5G period. The corporate’s portfolio contains voice, Machine-to-Machine (M2M) options, broadband, and IoT connectivity. Given the fast digital transformation, such choices have gotten more and more important. Apparently, CRNT’s attain is not restricted to simply telecommunications; in addition they serve public security and offshore drilling sectors. With operations from Asia-Pacific to the Americas and headquartered in Rosh Ha’Ayin, Israel, I consider CRNT’s world presence permits them to cater to a broad spectrum of market calls for, positioning them for potential progress within the evolving tech panorama.

Between December 2022 and June 2023, the corporate skilled a delicate but noteworthy progress in its whole belongings, rising from $289.3M to $294.5M. This increment, albeit modest, presents a buffer towards unpredictable market shifts. A pivotal facet of the corporate’s current monetary trajectory is the exceptional restoration in web revenue, which transitioned from a $3.8M loss to a $4.1M revenue in a mere six months. This upward shift, accentuated by a minor rise in whole present belongings from $210.7M to $215.8M, signifies enhanced operational efficiencies. It is believable that these efficiencies stem from well-executed cost-reduction methods (extra on this later). Additionally, CRNT’s money circulate dynamics corroborate this optimistic development, with web money from working actions transitioning from a $4.9M deficit to a $6.7M surplus.

CRNT’s web site.

Outlook and Promising Margin Enlargement

Throughout CRNT’s newest earnings name, the corporate mentioned its upcoming product roadmap, highlighting its technique to scale back BOM prices utilizing ASIC developments as 2024 approaches. Doron Arazi, the CEO of CRNT, underscored the corporate’s dedication to introducing a revamped model of choose merchandise. These improvements are designed to adeptly merge technological necessities with concerns of whole value of possession (TCO). For my part, Arazi’s affirmation that these merchandise are set for a business debut shortly enriches the corporate’s present choices and indicators a proactive strategy to market calls for. CRNT’s CEO additionally hinted {that a} next-generation chip with superior capability options is scheduled for a 2024 launch. Whereas Arazi anticipates that the income contribution from this chip could be restricted in its debut yr, I consider CRNT’s aggressive value construction from the get-go is encouraging. This positions the product favorably available in the market, and as gross sales volumes rise, there’s potential for even more healthy gross margins.

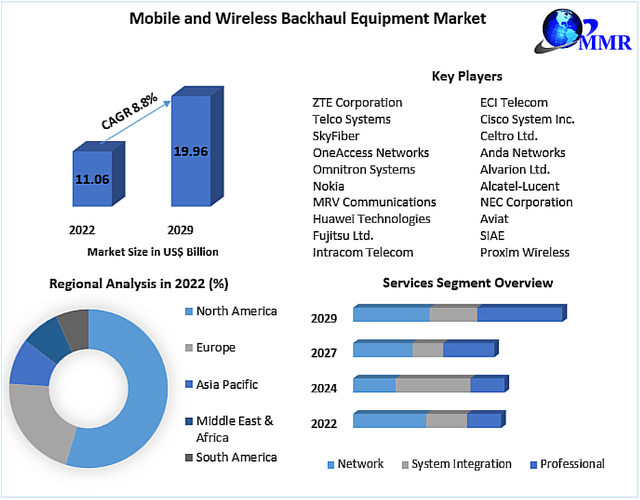

Maximize Market Analysis (maximizemarketresearch.com)

Moreover, contemplating broader trade tendencies, the worldwide wi-fi backhaul market reveals optimistic momentum. Elements such because the surge in smartphone adoption, the rollout of 5G know-how, and the rise in on-line media consumption drive this progress. These developments spotlight an rising demand for environment friendly knowledge transportation options. For my part, the information underscores the market’s promising potential. It’s anticipated to develop at a 12.5% CAGR from 2023 to 2028, with projections indicating a market valuation of roughly $71.77 billion by 2028. I consider that this progress trajectory aligns with CRNT’s technique to profit from this rising market.

CRNT’s web site.

Sadly, the telecommunications sector is present process a marked transformation, characterised by a transparent development in direction of consolidation. Notable mergers, such because the union of T-Cell (TMUS) and Dash (S) within the U.S., spotlight this shift. This case presents potential challenges for firms like CRNT. As an illustration, a big concern is the attainable lack of gross sales to longstanding clients, particularly once they merge with firms that favor competitor merchandise or have current infrastructures that negate the necessity for additional providers. This uncertainty can pause new partnerships or product orders, impacting income and progress plans. Furthermore, there is a rising development towards network-sharing agreements, the place operators mix their infrastructure sources. Whereas this can be financially useful for operators, it reduces the demand for community tools, doubtlessly impacting revenues for corporations on this sector.

Valuation Evaluation

For my part, we should depend on valuation multiples to evaluate CRNT’s valuation, because it’s unprofitable. For this, I consider that given the corporate’s enterprise mannequin, it’s affordable to deal with the EV/Gross sales and EV/EBITDA metrics, which are sometimes used for firms within the Know-how sector. CRNT’s ahead EV/Gross sales a number of stands at 0.59, considerably decrease by roughly 77.59% in comparison with the sector median of two.63. This case means that the market values CRNT’s gross sales at a reduction relative to its friends. Moreover, the ahead EV/EBITDA a number of for CRNT is 6.22, which can be significantly decrease by about 54.75% than the sector median of 13.76.

CRNT’s monetary self-discipline is obvious in its dealing with of working bills. The corporate has maintained its R&D prices at $7.6 million, representing 8.8% of income, down from 10.6% within the prior yr. This shift implies that CRNT is reaching extra with its R&D investments. Moreover, gross sales and advertising bills have been streamlined to $9.4 million or 10.9% of income, a lower from the earlier yr’s 12.8%. Nevertheless, a slight uptick in Normal and Administrative bills from 6.5% to 7.0% suggests the necessity for continued oversight.

Looking for Alpha plus writer’s elaboration.

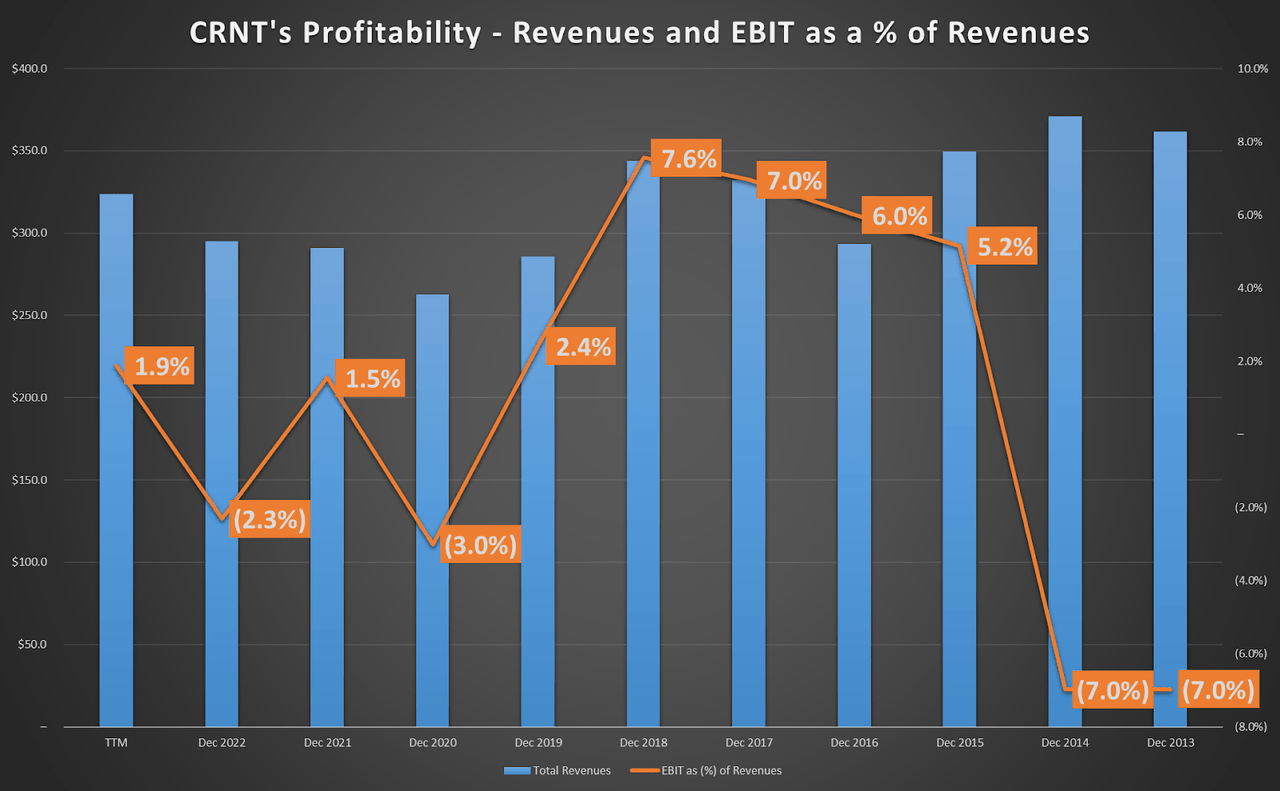

I consider CRNT’s forward-thinking strategy is highlighted by its forecasted working bills, which vary between $22 million and $23 million for the second half of 2023. This might lead to an annualized determine of as much as $92 million, marking an enchancment from the typical of $95.9 million since 2013. For context, CRNT’s EBIT margins have hovered round 1.1% since 2013, with a current uptick to 1.9% within the TTM, suggesting a optimistic trajectory influenced by operational enhancements. The preliminary indicators of margin enlargement and a decent CAGR of 6.0% in revenues since 2020 recommend CRNT is near reaching profitability.

TradingView.

Given its ongoing margin enhancements, I believe it is affordable for CRNT’s EBIT margin to stabilize at 2.5% of annual run charge revenues of $350 million. Therefore, contemplating the sector’s median EV/EBIT ratio of round 18, I derive an annual EBIT run charge of $8.75 million. Utilizing a conservative EV/EBIT a number of of 15, CRNT’s enterprise worth is estimated at $131.3 million. After accounting for money and debt changes, the implied truthful worth is $161.3 million. Thus, CRNT appears pretty priced in comparison with its market capitalization of $170 million. Whereas CRNT showcases promising enterprise fundamentals, its present inventory valuation would not current a compelling purchase alternative, main me to offer it a impartial ranking.

Conclusions

General, CRNT presents a various portfolio that appears well-suited to satisfy the calls for of an more and more digital world. The corporate’s current monetary milestones and forward-thinking product initiatives recommend the potential for margin enchancment. Plus, I consider the anticipated progress of the worldwide wi-fi backhaul market underscores these alternatives. Nevertheless, the continued development of consolidation within the telecommunications sector presents challenges. And, given CRNT’s present lack of profitability, these challenges warrant cautious consideration. Thus, primarily based on my valuation evaluation, CRNT seems to be buying and selling near its intrinsic worth, main me to take care of a impartial stance on the inventory. The rationale for that is the stability between the corporate’s progress prospects and the inherent dangers within the sector.

{kind=link}