Movement Loop/iStock through Getty Photographs

C4 Therapeutics, Inc. (NASDAQ:CCCC) pioneered focused protein degradation [TPD] with its TORPEDO platform to design molecules to interrupt down disease-causing proteins. Its pipeline contains CFT7455, CFT1946, and CFT8919, that are biodegradable oral catalytically environment friendly degraders for goal proteins inflicting situations like A number of Myeloma, Non-Hodgkin’s Lymphoma, and varied cancers marked by mutations like BRAF V600X and EGFR L858R. These medicine are in Section 1 medical trials and have a transparent plan for 2024. Additionally, the corporate collaborates with Merck (MRK) based mostly on some great benefits of the revolutionary TORPEDO platform. Nonetheless, after its valuation, CCCC seems fairly costly, which tempers my optimism concerning the inventory. Thus, I lean in the direction of a impartial score, balancing each side.

Enterprise Overview

C4 Therapeutics is an early clinical-stage biopharmaceutical firm based in 2015 and based mostly in Watertown, Massachusetts. The corporate develops drug candidates for focused protein degradation [TPD] within the battle towards oncological, autoimmune, and neurological situations provoked by disease-causing proteins. Nonetheless, C4 nonetheless hasn’t generated any income from product gross sales since inception and has posted a $132.5 million loss for 2023. Furthermore, the corporate expects to proceed requiring further funding to pursue its enterprise goals, largely centered across the TORPEDO platform.

Supply: Company Presentation, February 2024.

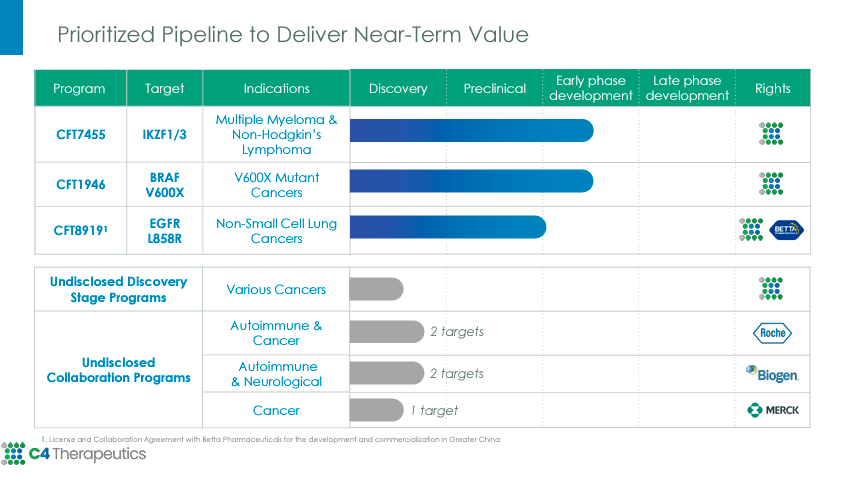

As for CCCC’s product pipeline, the corporate’s portfolio largely contains CFT7455 for IKZF1/3 protein goal for A number of Myeloma & Non-Hodgkin’s Lymphoma remedy and CFT1946 towards BRAF protein with the V600X mutation for V600X Mutant Cancers. Nonetheless, these therapies are within the early stage of medical growth. Additionally, CFT89191 is one other degrader for remedy towards EGFR with L858R mutation that produces Non-small-cell lung cancers. Luckily, CFT89191 is on the finish of the preclinical trials however continues to be removed from any concrete FDA approvals. Moreover, CCCC has two further packages in an undisclosed discovery stage for varied different cancers and autoimmune and neurological issues.

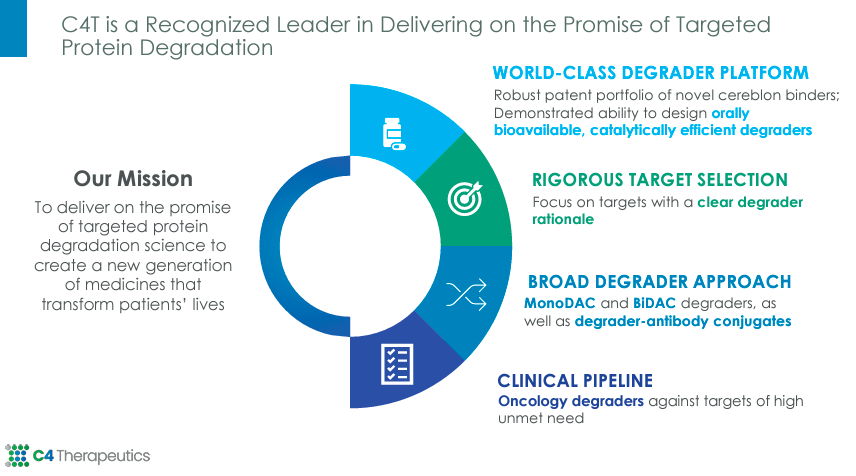

Due to this fact, we should always concentrate on CCCC’s scientific platform, TORPEDO (Goal Oriented Protein Degrader Optimizer). That is truly fairly an enchanting know-how that permits focusing on nearly any disease-causing protein, so its implications might be vital for researchers. TORPEDO makes use of computer-based instruments to design molecular glues with two useful ends: one binds to the goal protein and the opposite to an E3 ubiquitin ligase, a key enzyme within the ubiquitin-proteasome system. As soon as the E3 ubiquitin ligase is near the goal protein, it catalyzes the switch of a small molecule of ubiquitin that serves as a tag that prompts proteasome to degrade and recycle proteins. Thus, this breaks them down into its part peptides.

Supply: Company Presentation, February 2024.

This issues as a result of lowering dangerous proteins normally alleviates signs of assorted illnesses. Extra importantly, TORPEDO lets researchers selectively take away damaging proteins past conventional inhibitors that solely block the protein perform. This mechanism may theoretically skip inflicting undesirable uncomfortable side effects because it avoids different pathways. Apparently, TORPEDO’s degraders are additionally taken orally and are bioavailable, handy, and cost-effective with out further drug administration prices. CCCC’s degraders appear extra handy than different protein degraders, normally administered intravenously. So, C4’s platform is revolutionary, though it’s nonetheless experimental.

C4’s R&D And Collaborative Milestones

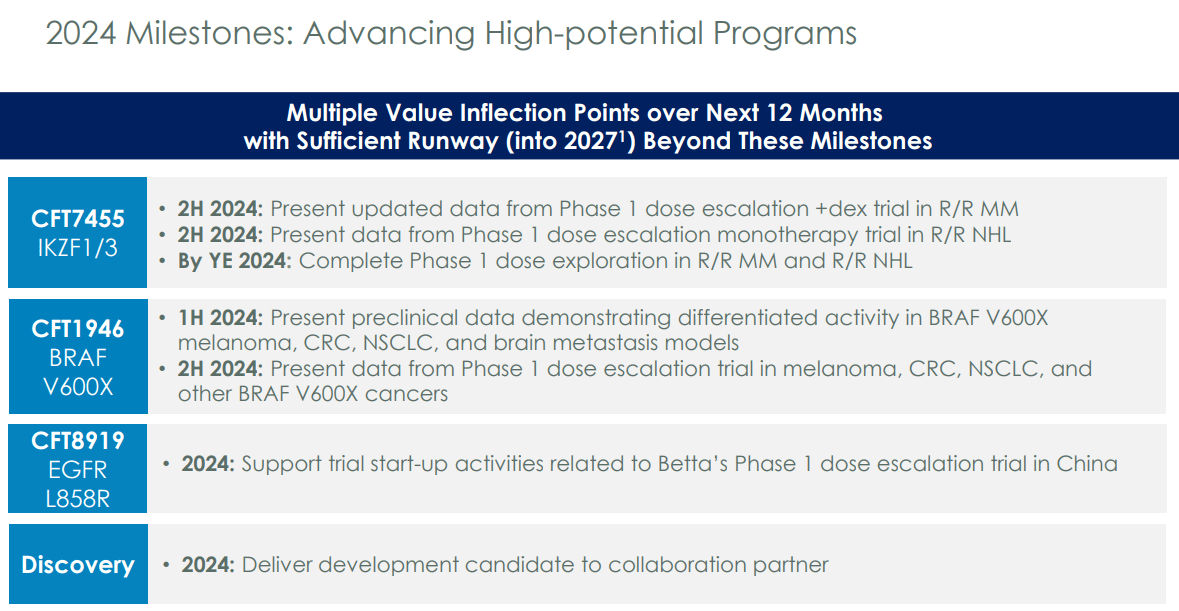

On C4’s February 2024 Company Presentation, they introduced their plan to concentrate on two analysis packages: 1) CFT7455 / IKZF1/3 and a pair of) CFT1946 / BRAF V600X. There, CCCC outlined its plans for the second half of 2024, which I consider might be understood as the 2 most promising packages in its analysis pipeline.

Supply: Company Presentation, February 2024.

For the primary analysis program, CCCC goals to current up to date information from Section 1 for relapsed/refractory a number of myeloma [R/R MM]. Additionally, on this interval, the corporate expects to current information from Section 1 for relapsed/refractory non-Hodgkin lymphoma [R/R NHL]. By the tip of 2024, the completion of Section 1, dose exploration, for R/R MM and R/R NHL is deliberate. As for the second a part of their analysis program (i.e., CFT1946 / BRAF V600X), CCCC will current preclinical information throughout 1H2024 to distinguish the exercise in BRAF V600X melanoma, colorectal most cancers [CRC], non-small cell lung most cancers [NSCLC], and mind metastasis fashions. Then, In 2H2024, CCCC plans to current Section 1 information, dose-escalation trial leads to melanoma, CRC, NSCLC, and different BRAF V600X cancers.

Other than these two most important analysis packages, CCCC can be creating CFT8919 / EGFR L858R with trial start-up actions for Betta’s Section 1 dose escalation trial in China. Additionally in 2024, the corporate will ship a growth candidate to a collaboration accomplice for autoimmune, neurological, and most cancers illnesses.

C4’s Partnership With Merck

On December 12, 2023, CCCC made an unique license take care of Merck to develop degrader-antibody conjugates [DACs] for most cancers with its proprietary TORPEDO platform to find degrader payloads. Merck can be accountable for antibody conjugation to generate DACs and develop them by preclinical and medical trials and commercialization. CCCC will obtain $10 million upfront plus tiered royalties on gross sales and roughly $600 million milestone funds for DACs directed to the oncology goal.

Supply: Company Presentation, February 2024.

Furthermore, Merck may additionally lengthen the collaboration to incorporate three further targets, producing additional funds for exercising this feature and potential milestones and royalties for as much as round $2.5 billion. Thus, the take care of Merck might be a most important worth driver for CCCC in the long term if the collaboration is prolonged to three extra goal proteins. Nonetheless, it’s value noting that this partnership relies on the outcomes that the TORPEDO platform guarantees. To this point, this proprietary know-how appears to be gearing as much as ship capabilities for designing molecules that degrade nearly any disease-causing protein, however its final success is just not assured.

Fairly Costly: Valuation Evaluation

From a valuation perspective, C4 presents a combined image. On the one hand, it looks like it’s implementing cost-cutting measures that might enhance its money runway and, by extension, the percentages of succeeding in its partnership with Merck. For context, on January 10, CCCC inventory appeared to react positively to the announcement of a restructuring plan that features a 30% workforce discount, prioritizing the event of the protein degraders CFT7455 and CFT1946. The plan additionally goals to assist Section 1 medical trials for CFT8919 developed by Betta Prescription drugs in China. After this announcement, the inventory traded larger, possible as a result of buyers appeared optimistic about prioritizing this portion of their IP. Since then, the inventory has traded decrease, from the post-announcement excessive of $7.66 to roughly $5.30 per share by the fifth of February.

C4 inventory elevated to an area prime on January 10. (Supply: TradingView.)

However, I consider that this restructuring effort labored, because the earnings report on February 22 confirmed an enchancment in internet earnings over expectations. The market had anticipated a $0.70 loss per share, and C4 reported a $0.68 loss per share as an alternative. Naturally, losses are nonetheless piling up, however this enchancment possible implies higher margins because of the cost-cutting measures introduced. Nonetheless, quarterly revenues got here in beneath expectations by roughly $410.97 thousand.

Supply: Searching for Alpha.

On January 5, CCCC reported $253.7 million in money, money equivalents, and marketable securities that the corporate believes will fund its operations till 2027. I estimate their quarterly money burn at $24.2 million, which suggests a yearly money burn of $96.8 million. I obtained this determine by including the corporate’s quarterly CFOs and CAPEX and annualizing them. Thus, my calculations recommend a money runway of roughly 2.6 years. This implies there’s sufficient money to final till 1H2026, however I think about that CCCC anticipates money circulation enhancements by then. So, their declare of getting sufficient money till 2027 appears a bit optimistic, however not inconceivable.

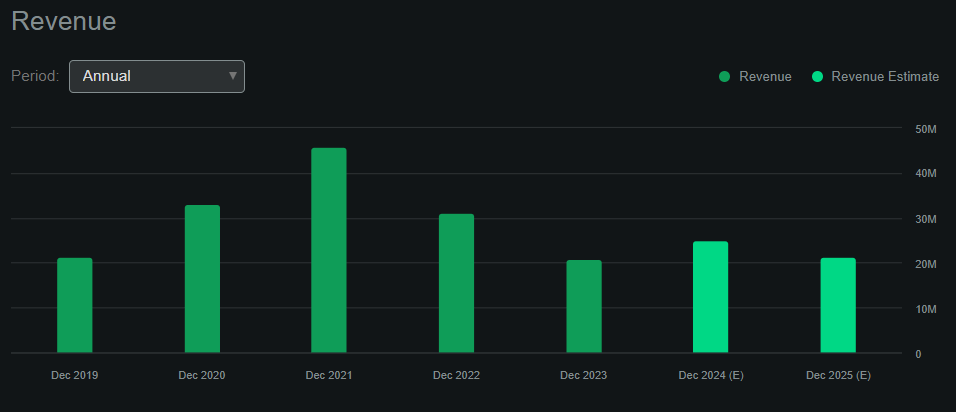

That’s key as a result of if CCCC’s guess on TORPEDO and the remainder of its product portfolio works out, its revenues may bounce considerably. In spite of everything, the partnership with Merck alone might be value billions of {dollars} if it’s totally exploited. Nonetheless, as of at this time, CCCC is anticipated to generate roughly $21.24 million in revenues by 2025. Therefore, the present market cap of $753.24 million implies a ahead P/S ratio 35.5. If we examine this valuation a number of to C4’s sector median ahead P/S ratio of three.99, it instantly appears to be like considerably overvalued. Actually, since CCCC is burning money and accumulating losses, most of its valuation multiples are considerably above its sector friends. All this leads me to mood my optimism on CCCC inventory, giving it a “maintain” score.

Conclusion: A Blended Bag

CCCC is a promising biopharmaceutical that might repay if its guess on TORPEDO and the remainder of its product pipeline works out. Nonetheless, at its present stage, CCCC trades at a major premium in keeping with most valuation multiples as a result of it continues to pile up losses and burn money. Due to this fact, there are tangible considerations relating to the corporate’s long-term success, though it seems to have the funds for to see by its analysis. I’m optimistic about TORPEDO and its doubtlessly revolutionary know-how, however on the identical time, the funding perspective is plagued with extreme dangers. Thus, I lean in the direction of a impartial score on CCCC and provides it a “maintain” for now.

{kind=link}