DestinoIkigai/iStock by way of Getty Pictures

Introduction

At our Conservative Earnings Portfolio service, we’re always taking a look at all sectors and asset courses to seek out relative mispricing alternatives to extend our member’s portfolio yields and/or to scale back danger. Discovering mispricings not solely supplies alternatives to swap considered one of your securities for a greater one however may also be helpful in figuring out undervalued shares/bonds for outright buy and not using a have to swap.

There are not any objectively low-cost or costly securities. Securities are solely low-cost or costly relative to different securities. Thus, with a purpose to establish the perfect values available in the market, you really want to cowl all sectors and all asset courses (most well-liked shares, child bonds and conventional bonds). If you’re solely protecting a sure sector or a sure asset class, or a subset of securities, then it is vitally troublesome to evaluate whether or not a safety is undervalued or not.

For instance, should you solely cowl child bonds and never conventional bonds, chances are you’ll discover that you’re not in the perfect bonds. If you happen to solely take a look at most well-liked shares and never child bonds, you might also discover that you’re not in the perfect securities. And should you solely cowl financial institution most well-liked shares or REIT most well-liked shares, additionally, you will possible discover that you’re not in the perfect investments.

We perceive that it is vitally time consuming for people, and even different inventory companies, to cowl such a variety of securities which is likely one of the causes that our Conservative Earnings Portfolio exists. On this article we current alternatives for swaps or for merely taking lengthy positions in numerous sectors and asset courses.

Mortgage REITs

Mortgage REITs, or mREITs, personal mortgages. They’ll personal company (authorities assured) residential mortgages, non-agency residential mortgages in addition to industrial mortgages. And a few can maintain a mixture of company and non-agency mortgages.

mREITs earn a living by borrowing at low rates of interest and utilizing that cash to purchase increased yielding mortgages, hopefully making a revenue on the rate of interest unfold. Whereas company mREITs like Cherry Hill (NYSE:CHMI) and Armour Residential (NYSE:ARR) maintain solely company mortgages, and thus haven’t any credit score danger, different mREITs maintain mortgages that may default in order that they do carry credit score danger. Each varieties of mREITs carry rate of interest danger and pre-payment danger.

Cherry Hill Mortgage

Firm web site

Cherry Hill Mortgage (CHMI) owns residential mortgages which might be backed by the U.S. authorities, in order that they carry no credit score danger. Moreover they personal some mortgage servicing proper (MSRs) by which they earn a charge for servicing these mortgages. MSRs must be very secure now as a result of the massive danger with MSRs is that the mortgages that they service get refinanced or paid off when the house is offered.

At the moment, we’re in a superb atmosphere for MSRs that had been bought when rates of interest had been a lot decrease. No person is refinancing their loans now with charges presently a lot increased than their present mortgages. Moreover, individuals might be very reluctant to maneuver and lose their low curiosity mortgage and must tackle a a lot increased price mortgage with a purpose to buy a special house.

So MSRs ought to present a really secure stream of earnings to CHMI, whereas the mortgages owned by mREITs are topic to the dangers of an inverted yield curve, increased long run rates of interest hammering e-book worth, the next price of quick time period borrowing, failed hedging methods and a potential continuation of a widening yield unfold between treasuries and mortgage backed securities (MBS).

Armour Residential Mortgage

Firm Web site

Armour Residential Mortgage (ARR) was as soon as a hybrid mREIT proudly owning each company and non-agency mortgages. Nevertheless, they had been by and huge an company mREIT since over 90% of their mortgages had been company mortgages. Through the COVID inventory market meltdown, they took a beating and needed to promote plenty of their mortgages at hearth sale costs. Shortly after the COVID market backside, they determined to promote their non-agency mortgages and turn into a strictly company mREIT.

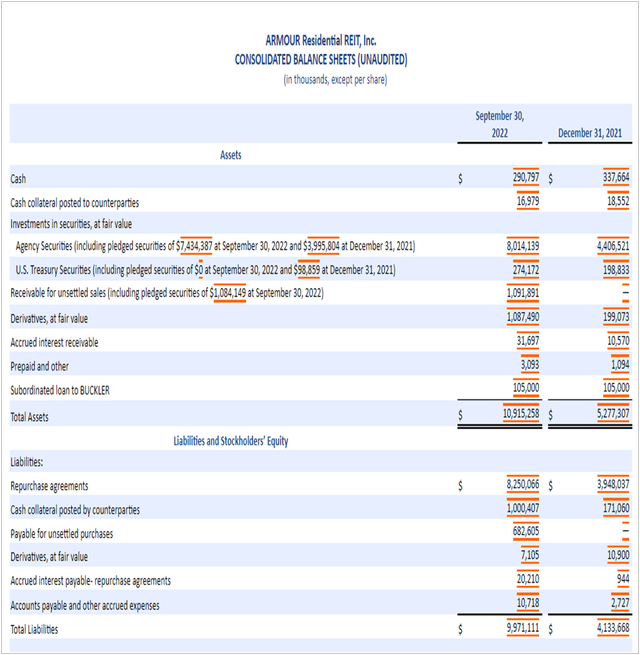

Whereas ARR operated at pretty low leverage for a while, ARR has quickly been growing their leverage this yr. It looks like buyers haven’t observed this and are nonetheless keen to buy ARR Most popular “C” (NYSE:ARR.PC) at a a lot decrease yield than Cherry Hill Most popular “A” even supposing ARR’s leverage is now increased than CHMI’s. Right here is the latest ARR stability sheet which additionally reveals a comparability of the present quarter’s leverage to the leverage initially of this yr.

SEC

As you possibly can see, initially of the yr, ARR’s whole liabilities had been solely 78.5% of whole property. Nevertheless, as of September 30th, whole liabilities at the moment are 91.3% of whole property.

Purchase Cherry Hill Most popular “A”, Promote Armour Residential Most popular “C”

What makes these 2 most well-liked shares simple to check is that they each function in the identical enterprise, and these are the one 2 company mREIT most well-liked shares which have a set dividend. Most mREIT preferreds which have IPO’d in latest instances have been fixed-to-floating price preferreds. So should you like proudly owning an company mREIT most well-liked inventory the place you possibly can lock in a excessive fixed-income, CHMI Most popular “A” is the one to personal. Right here is why:

- The primary and most blatant purpose to purchase Cherry Hilll Most popular “A” (CHMI.PA) and promote Armour Residential Most popular “C” (ARR.PC) is the very giant distinction in yield. Whereas ARR.PC yields solely 8.67%, CHMI.PA yield’s 9.8%.

- CHMI operates at decrease leverage. Whereas CHMI’s whole liabilities, together with most well-liked inventory, are 8.8 instances its widespread stockholder’s fairness, ARR’s whole liabilities plus most well-liked inventory are 12.1 instances its widespread stockholder’s fairness. That’s fairly excessive leverage for ARR.

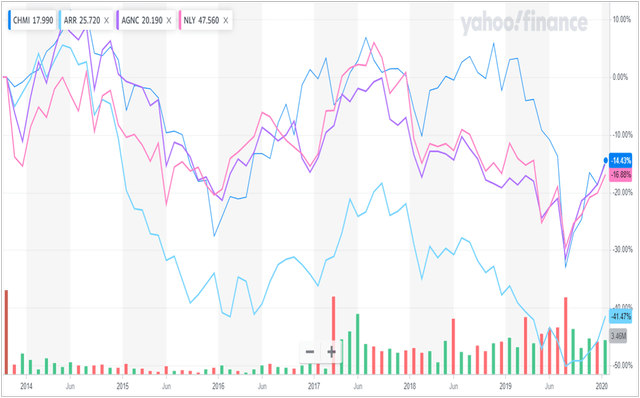

- Cherry Hill’s widespread inventory has properly outperformed ARR’s widespread inventory because the charts beneath present.

Yahoo Finance

Here’s a value chart evaluating CHMI to ARR earlier than the COVID meltdown when ARR was principally an company mREIT however not fully. The interval is from the inception of CHMI in 2013 to the start of 2020 earlier than the COVID market meltdown. As you possibly can see, CHMI carried out considerably higher than ARR as ARR was down 41% throughout this era. I threw within the charts of the massive company mREITs, NLY and AGNC, to indicate that CHMI carried out equally properly to their extra well-known friends.

For the reason that March 18th, 2020 COVID backside available in the market, CHMI has additionally outperformed ARR.

I imagine company mREIT preferreds are very protected. They haven’t any credit score danger and since they problem widespread inventory to boost money when leverage begins to rise, this mitigates stability sheet danger. Thus, I imagine that CHMI.PA is an excellent worth with a 9.8% mounted yield. Whereas many personal the fixed-to-floaters of company mREITs AGNC and NLY, these presently contain a wager on LIBOR (or its alternative) remaining excessive. This isn’t a wager that I’d personally make. I imagine that locking in a 9.8% yield will look actually good when the Fed slows the economic system and charges begin coming down. And given its giant low cost from par, there may be plenty of room for CHMI.PA to maneuver increased in value.

And I imagine that ARR.PC must be offered. It’s merely overpriced relative to its closest peer, and you’ve got a superb different in CHMI.PA.

Different Swapportunities

Promote OPINL and Purchase the OPI 2025 Bond

OPINL is a bond from Workplace Properties, an workplace REIT. It doesn’t mature till 2050 and carries a 9.3% yield to maturity (YTM). But you should purchase their a lot shorter time period conventional bond, a bond that matures on February 1st, 2025, at a present YTM of 12.28%. The CUSIP of this bond is 81618TAC4.

As a result of OPI is managed by RMR, many buyers are turned off to the widespread inventory and to the corporate on the whole. Whereas I don’t have good emotions about OPI itself, and I wouldn’t need to wager on a bond of theirs that doesn’t mature till 2050, after I see an enormous yield on a bond that matures in a bit of greater than 2 years, I turn into .

Whereas I solely personal a small place on this OPI bond, I believe it is vitally unlikely that this firm goes bankrupt in such a brief time period. RMR actually desires this firm to outlive in order that they’ll proceed amassing administration charges, and I’d be shocked in the event that they didn’t problem inventory to boost money if it turns into obligatory. And workplace property leases are typically a few years in size which provides to the safety of those bonds.

Purchase PEB.PG and Promote Hersha Hospitality (HT) Most popular Shares

Each Hersha Hospitality (HT) and Pebblebrook (PEB) are lodge REITs. For my part, PEB.PG (PEB.PG) presently represents probably the most undervalued lodge REIT most well-liked inventory relative to all others. Nevertheless it appears notably undervalued relative to the HT most well-liked shares as a result of PEB’s a lot better stability sheet. A swap from HT most well-liked shares to PEB not solely will get you a greater yield, however a greater stability sheet and an even bigger low cost from par offering extra long run value upside.

HT has 3 most well-liked shares, HT.PC, HT.PD and HT.PE. The present stripped yield on these is round 8.4% and so they promote at a mean value of $20.00. PEB.PG sells at $17.72 with a 9.12% present stripped yield. It’s the solely lodge REIT most well-liked inventory amongst many with a greater than 9% yield.

But when that isn’t sufficient to make you need to swap into PEB.PG, the distinction in stability sheet leverage ought to persuade you. Whereas HT’s whole liabilities plus most well-liked inventory is 3.1 instances its widespread stockholder’s fairness, PEB’s is just one.55 instances. Moreover, throughout the huge 2020 market selloff, HT suspended its most well-liked inventory dividends whereas PEB has by no means carried out so.

Promote RILYL Most popular Inventory and Purchase a RILY Child Bond (RILYM or RILYT)

This one is fairly easy. The B Riley (RILY) most well-liked inventory with the ticket RILYL appears very overvalued and must be offered. RILY has a lot better securities to swap into then RILYL. Even their different most well-liked inventory is a a lot better worth, however the RILY child bonds current extraordinarily higher values than RILYL.

RILYL present sells for $24.22 for a 7.65% present yield. Even their different most well-liked inventory, RILYP, is a lot better with an 8.32% present yield and rather more value upside at a value of $19.90.

However the perfect values are within the RILY child bonds which offer extra safety, being increased within the capital stack, but additionally maturity dates which makes them a lot much less inclined to rate of interest modifications and the safety that you’re going to get $25 again should you maintain to maturity. Until there’s a chapter, all RILY bonds will find yourself increased in value sooner or later.

My 2 favorites now are:

- RILYM has a superb YTM of 9.77% and a comparatively quick maturity date of two/28/2025. RILYO presently has a YTM of 8.07% YTM and matures 9 months earlier. Getting an entire 1.7% higher yield for merely going out 9 months additional in length appears to be a relative discount.

- RILYM, with a ten.11% YTM which lets you lock on this excessive yield for an extended time period if you want. It matures on 1/31/2028 and presently affords the next YTM than RILYZ which matures later in 2028 than RILYT.

Abstract

As I wrote within the introduction, at Conservative Earnings Portfolio we’re always looking out for undervalued most well-liked inventory, child bond and conventional bond alternatives in all sectors with a purpose to enhance member’s portfolio yields and to scale back danger. On this planet of investing, there are not any objectively low-cost or costly securities. There are solely comparatively low-cost or costly securities. On this article we offered the next mispricing alternatives or “swapportunities” as I name them which lower throughout all sectors and asset courses:

- Shopping for CHMI.PA and promoting ARR.PC, bettering your yield from 8.67% to 9.8%, and decreasing danger with a decrease leveraged firm with a greater monitor file.

- Shopping for a a lot shorter yielding bond from OPI with a 12.28% YTM, and promoting a really long run bond from OPI whose YTM is barely 9.3%.

- Shopping for the Pebblebrook most well-liked inventory image PEB.PG, with a 9.12% present yield and a 1.55 instances leverage, and promoting Hersha Hospitality most well-liked shares, HT.PC, HT.PD, and HT.PE, with their decrease yields of round 8.4% and rather more leverage of three.1 instances.

- Shopping for both RILYM or RILYT with YTMs of 9.77% and 10.12% respectively, and promoting RILY’s most well-liked inventory, RILYL, with solely a 7.65% present yield and little or no value upside potential.

{kind=link}