Shutter2U

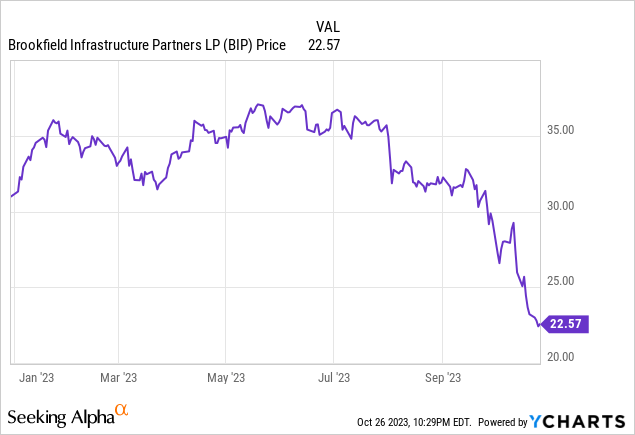

The sharp selloff of Brookfield Infrastructure Companions (NYSE:BIP) (NYSE:BIPC) over the past month has been shocking, an depth that at occasions has appeared like we have been again within the early days of the pandemic. On the core of the pullback is the 20 September Federal Open Market Committee assembly which noticed charges paused at their present 22-year excessive of 5.25% to five.50% however with a reiteration of a better for longer mantra that the market has translated as carte blanche to wipe off 30% from the worth from BIP since this date. To be clear, nothing has essentially modified with the September pause more likely to be adopted by the primary consecutive price pause for the reason that Fed began elevating charges once they subsequent meet in a couple of days on 1 November 2023. The market is at the moment pricing in a 99.9% likelihood that the Fed retains charges unchanged.

We’re at the moment within the age of macro, a interval JP Morgan’s Jamie Dimon has described as essentially the most harmful time in many years. We’re within the age of the macro and shares may proceed to commerce down or flat towards an unsure macro backdrop. BIP owns a various portfolio of infrastructure belongings from ports, knowledge facilities, pipelines, and toll roads. The corporate additionally owns transmission and telecommunication traces and lately added Triton Worldwide (TRTN), the world’s largest container leasing firm, in a money and inventory acquisition during which BIP invested $1.3 billion. BIP is rated funding grade BBB+ by Fitch with a complete debt-to-equity ratio of 136% as of the top of its fiscal 2023 second quarter.

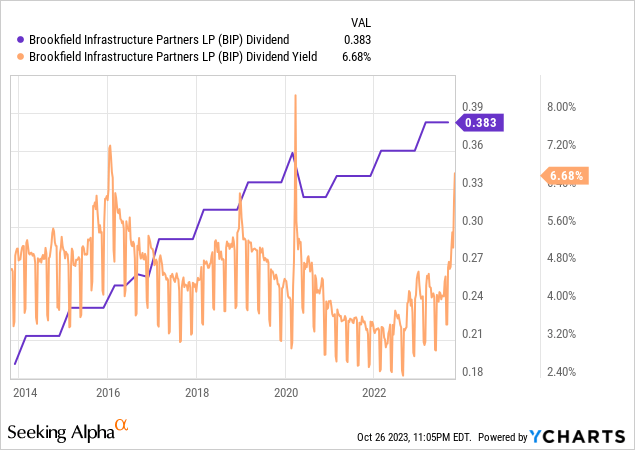

Round 90% of its long-term debt is at fastened charges with one other $2.3 billion in liquidity accessible throughout the third quarter whose earnings BIP is about to report on 1 November 2023, earlier than the market opens. The corporate final declared a quarterly money distribution of $0.3825 per unit, unchanged from its prior distribution for what at the moment works out to be a 6.8% annualized dividend yield. This has grown at a 5.8% 3-year compound annual development price with BIP focusing on continued dividend development on the again of what is anticipated to be a 12% funds from operation per unit CAGR over the following 3 years.

FFO Expectations From Third Quarter And The rest Of 2023

Brookfield Infrastructure Companions September 2023 Investor Day

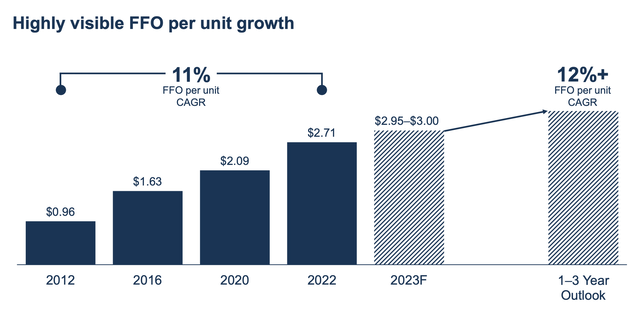

BIP is guiding for a full-year 2023 FFO per unit to vary between $2.95 to $3. This is able to signify development of at the very least 24 cents per unit on the low finish of the vary. The corporate at the moment covers its present quarterly distribution to unitholders by 188% and likewise has two excellent publicly traded most popular items; Brookfield Infrastructure Companions L.P. 5.125 CL A PFD13 Sequence 13 Most popular Partnership Models (NYSE:BIP.PR.A) and Brookfield Infrastructure Companions L.P. 5.00% PFD A 14 Sequence 14 Most popular Restricted Partnership Models (NYSE:BIP.PR.B). They’re each swapping palms with comparable reductions to their $25 par worth with the Sequence 13 buying and selling for 62 cents on the greenback and with an 8.28% yield on price to supply a compelling funding proposition to extra risk-averse traders drawn to BIP’s onerous belongings.

Brookfield Infrastructure Companions Fiscal 2023 Second Quarter 2023 Outcomes

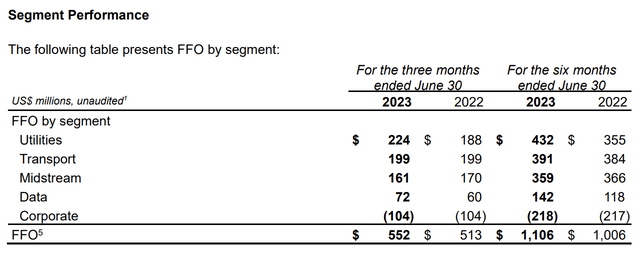

The third quarter ought to see the contribution of BIP’s Canadian diversified midstream enterprise whose Heartland Petrochemical Complicated was offline for a lot of the second quarter which contributed to what was a $9 million decline in FFO year-over-year to $161 million from BIP Midstream phase throughout the second quarter. Nonetheless, Heartland will solely have its full contribution realized within the fourth quarter with this contribution to annual FFO included within the firm’s forecast for full-year FFO.

Valuation And The Dividend

Is BIP undervalued at its present stage? It will depend on what metric is used. The corporate is buying and selling at a worth to FFO per unit of seven.6x, with a ahead FFO yield of 13%. The corporate has been capable of preserve FFO development towards rate of interest headwinds on the again of its largely fixed-rate debt financing construction and belongings with long-term inflation-linked money flows. The utility phase generated $224 million in FFO throughout the second quarter, a rise of 19% over the year-ago interval with roughly half of this development being pushed by natural inflation indexation.

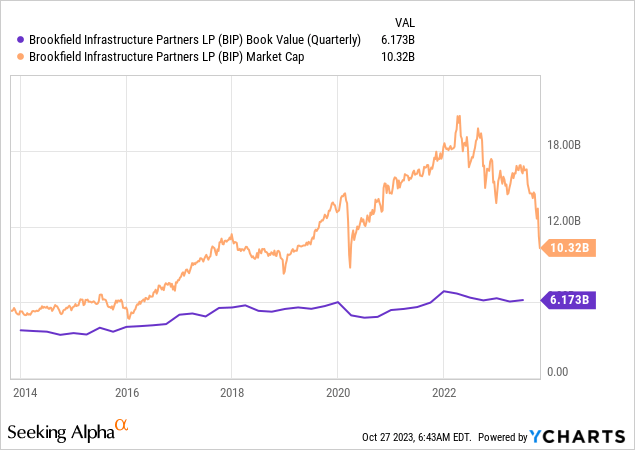

Nonetheless, the corporate remains to be buying and selling at a big 67% premium to its guide worth of $6.17 billion as of the top of the second quarter. I do not assume a transfer to commerce at parity with guide worth is in play. This didn’t occur in 2020 and continued FFO technology power and a string of what is set to be extremely cash-generative acquisitions bolster BIP’s long-term funding case. Critically, there’ll possible be one other near-term dividend elevate, therefore, the dividend yield may transfer as much as 7% assuming the unit worth stays comparatively flat from its present worth. I am not at the moment invested in BIP however will look to construct a place after the FOMC November price resolution.

{kind=link}