Jeremy Poland/E+ through Getty Photos

Funding Rundown

The place a lot of the enchantment of investing within the oil trade has come from is that firms very often ship robust dividend yields and buyback packages. That appears to stay true with BP p.l.c. (NYSE:BP), an organization that had a really strong begin to 2023 and introduced they’re shopping for again shares value $1.75 billion earlier than they even announce the Q2 outcomes of 2023. That form of information makes BP out to be a really intriguing funding for individuals in search of publicity to the trade, but in addition desire a place that persistently appreciates.

The basics of BP stay strong and with 40% of extra FCF devoted to enhancing the steadiness sheet, the corporate has accomplished strong work over the previous couple of years. The trade has historically traded at a reasonably low a number of, however even now BP is valued beneath the trade’s 5-year common p/e of 8.7. For my part, BP deserves a richer a number of given the strong fundamentals and the devoted capital going in the direction of buybacks and dividends. I’m score BP inventory a purchase.

Firm Segments

Inside BP, there are three main enterprise teams, these being Fuel & low carbon power, Manufacturing & operations, and lastly prospects & merchandise.

Inside the first phase, they concentrate on low-carbon power options akin to wind, photo voltaic, and hydrogen. Just lately, they’re additionally transferring into CCS tasks aiming to seize carbon and scale back air pollution. This can be a comparatively new market however one which sees robust demand and capital going in the direction of. The place BP sees itself creating worth right here and producing revenues is thru its built-in gasoline & LNG enterprise, but in addition with gasoline buying and selling and energy buying and selling.

The second enterprise group is the operational coronary heart of BP because it focuses on the manufacturing of hydrocarbon power. Discovering new prospects proper now principally circling current tasks and exiting hubs. This enterprise group can be concerned within the operations of oil and gasoline manufacturing property, in addition to refineries, terminals, and pipelines.

Lastly, the client & merchandise group focuses on driving new enterprise initiatives for his or her prospects and creating worth by partnerships, and optimizing their many fuels worth chains.

Earnings Highlights

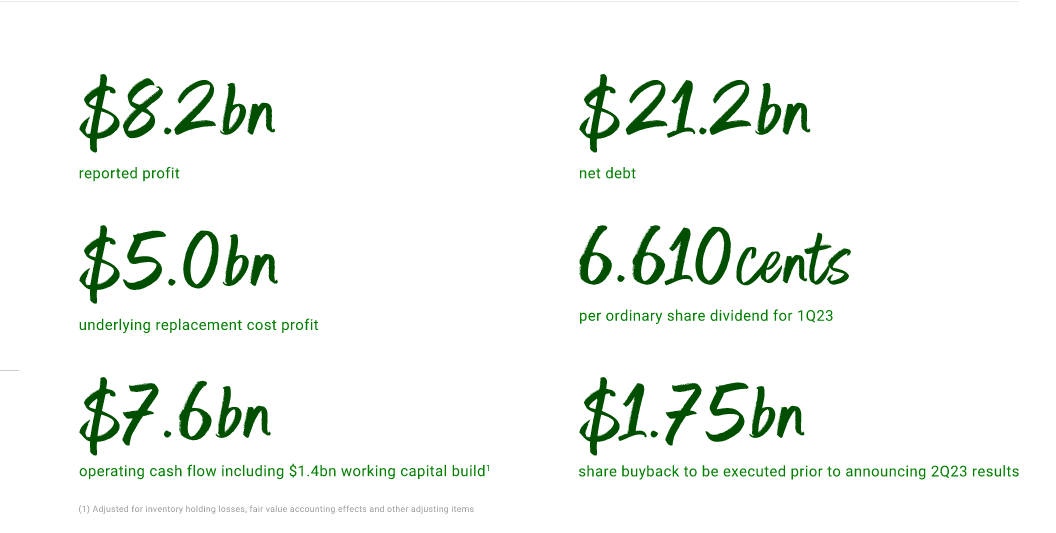

Wanting on the newest earnings from the corporate, they made it very clear they’re intending on sustaining a powerful conversion of FCF to distribute to shareholders. For Q1 2023, they distributed a dividend of $6.6 per share to their shareholders, they usually have persistently maintained a powerful dividend yield for his or her buyers. With that dividend, BP has a yield of 4.56%, making it very interesting as a dividend addition to a portfolio for my part. Now there are higher yields provided by different firms in the identical trade, however the place BP pulls forward is the numerous buybacks. The dividend and buyback plans appear to stay robust as BP generated $7.6 billion in working FCF to begin the 12 months.

Q1 Highlights (Investor Presentation)

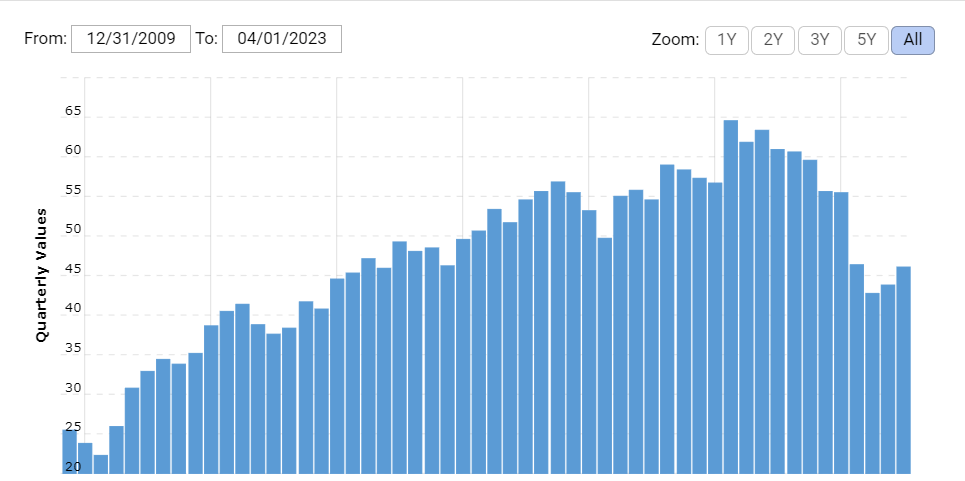

Over the previous couple of years, BP has made robust progress in the direction of paying down their long-term money owed, and Q1 was no totally different within the TTM as BP has paid down over $13 billion in money owed which ends up in them reaching a web debt of $21 billion. Meaning BP has a really low web debt/EBITDA of simply 0.35 proper now, highlighting the strong place the corporate is in at the moment.

Debt Historical past (Macrotrends)

The online money owed peaked at round $63 billion however have since come down a good bit. Wanting forward, I believe that BP stays robust sufficient to take care of its present FCF plan the place 60% of the excess goes to shareholders.

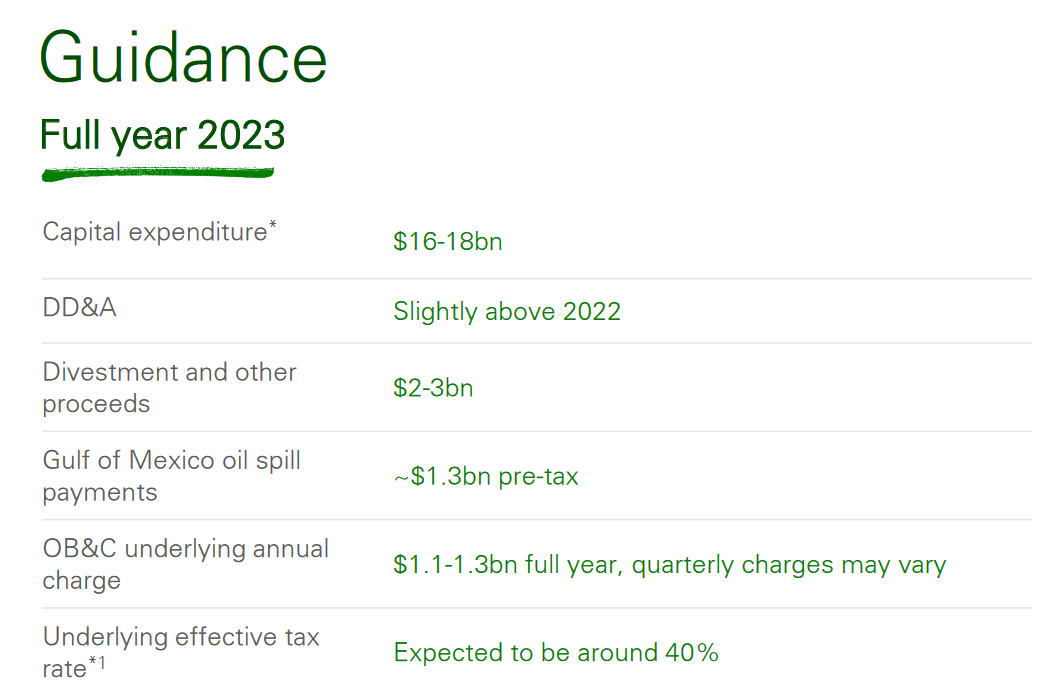

2023 Steerage (Q1 Earnings Presentation)

As for the place BP sees the remaining 12 months going, capital expenditures are to be between $16 – $18 billion, up considerably from 2022 which was $12 billion. I discover it doubtless that we do not see vital progress within the FCF given this upswing within the capital expenditures on a YoY foundation. The outlook the corporate had relating to buybacks is that they are going to have the ability to commit no less than $4 billion in the direction of repurchasing if Brent barrel costs stay at $60. However it will additionally embody an annual increase of 4% for its dividend yield.

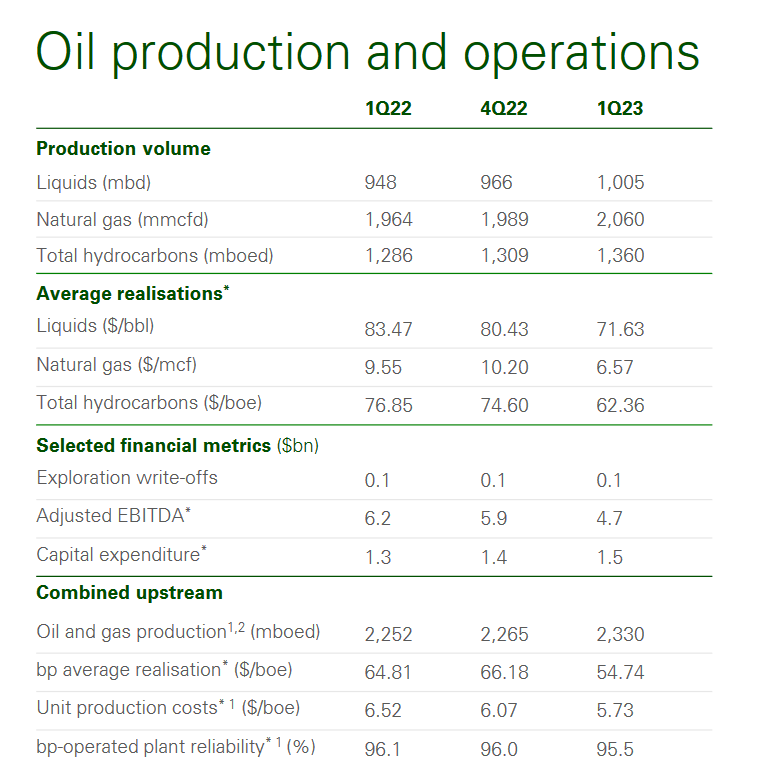

Oil Manufacturing (Q1 Report)

Lastly, the predictions from the quarter stay for my part very robust given the decrease Brent oil costs we’ve got in comparison with the 2022 ranges. Manufacturing volumes have been up throughout all elements of BP, the liquids, pure gasoline, and hydrocarbons all confirmed indicators of power. Now it is as much as BP to take care of this momentum and show that investing on this sector stays enticing.

Dangers

Because the revenues of BP are largely pushed by commodity costs, the danger that buyers must face is shopping for an organization that may expertise volatility in revenues on account of an unstable market setting. That has been the case with BP the place revenues have been largely up and down the final 10 years or so. However I believe the expansion trajectory stays robust as oil continues to be a really prevalent method for us to generate power and can proceed to be for a lot of extra years. The costs for Brent oil appear to have been in a constant decline for the final 12 months and that does make the EPS estimates for BP exhausting to make sure of. Downward revisions are very a lot potential if the market reveals weak point or demand diminishes.

CCS Tasks Potential

Touching briefly on the CCS tasks that BP is transferring into, it appears to be like promising. BP has signed an settlement the place they are going to take a 40% stake within the Viking carbon seize and storage venture within the North Sea. That makes for 3 BP-led tasks that revolve round hydrocarbon and CCS within the North-East of England which the UK authorities has chosen BP for.

However aside from that, BP additionally introduced plans for a low-carbon inexperienced power cluster in Valencia, Spain. The venture goals to refine as much as 2GW of electrolysis in complete capability by 2030. All in an try to make the BP Castellon refinery a world-scale inexperienced hydrogen web site.

I discover the brand new invitations to maneuver into CCS very interesting as the marketplace for it appears to be rising at a really quick fee proper now, with a 14% CAGR now till 2032. Authorities incentives are making this progress practical as helpful as funding tax credit and funding are being pushed, and for BP and others to capitalize on this, they’re proper now taking the required steps for my part.

Ultimate Phrases

As for my remaining phrases about BP, I believe the valuation proper now appears to be like very interesting. A p/e of beneath 6 makes it commerce beneath the sector’s common of 8.7. Some dangers are Brent oil has been on a gentle decline, however I believe that in years, it would finally normalize and BP could have loads of time to build up robust money flows and distribute a good portion of it to shareholders. The inducement right here for shareholders is to stay invested as BP is spending closely on shopping for again shares. Till Q2 2023 the excellent shares are anticipated to be diminished by practically 2% as BP goals to deploy $1.75 billion for buybacks.

The large presence that BP has accrued over its 113 years within the power enterprise makes its place nearly grown too massive to fail. A phrase that should not be thrown round too simply. However BP has accomplished very properly in pursuing and being chosen for a number of governmental tasks, just like the CCS tasks within the North-East of England. In consequence, BP is a purchase for me, and so long as Brent oil costs stay above $60, BP will proceed to ship strongly by way of FCF and EPS progress.

{kind=link}