koto_feja

The bear market shouldn’t be over. This has been our possible thesis because the begin of 2023. With the 10-year charges breaking out to new highs, and on-going inflation reviews displaying a re-acceleration beneath the headline numbers, it was obvious that the FOMC would want to boost the terminal charge to additional struggle cussed inflationary pressures. This realization marked the February high, which has since been intensified by the unexpected collapse of two giant regional banks.

We’re open to the bullish narrative; nonetheless, it could require a transparent and dramatic reversal within the month-to-month inflationary developments, coupled with no extra banks coming beneath strain. The needle the FOMC should thread is without doubt one of the most delicate in trendy historical past. With inflation nonetheless elevated and displaying little indicators of decelerating in key areas, how a lot can the Fed drop charges, in need of a financial institution contagion? Both manner, it doesn’t look good for equities, and till we get indicators of this bullish state of affairs enjoying out, we are going to stay cautious and defensive.

Broad Market Evaluation

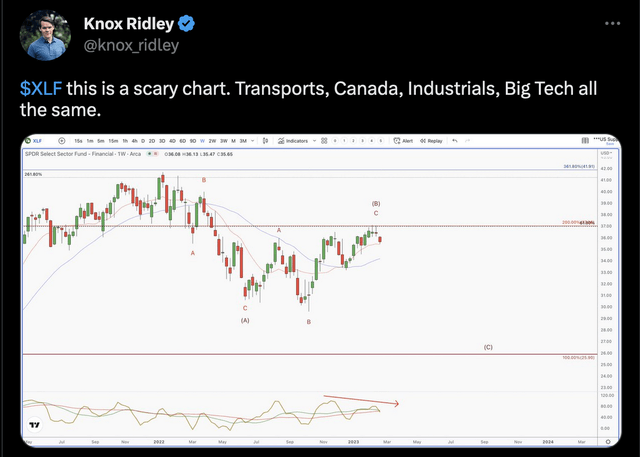

We’ve got been warning our members since early 2023 that this market is unhealthy. Our automated hedge sign went to promote, and we’ve got been hedged since early February; nonetheless, the warnings have been current lengthy earlier than. We have been seeing warning indicators in Financials lengthy earlier than the present regional banking disaster. On February twenty second, we even posted a public warning about this sector flashing warning indicators.

Twitter

We have been seeing a transparent bearish sample forming off the October low, which was confirmed during the last 2 weeks.

Creator

We have been additionally seeing related warnings in worldwide markets. The explanation this was regarding was that if we have been on the verge of beginning a brand new bull market, this might seemingly be signaled throughout the globe. This was not what we have been seeing.

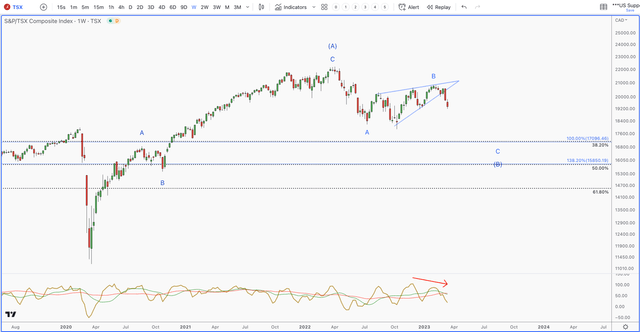

For instance, the Canadian TSX has an extended historical past of main the US markets. This was a really clear bear pennant enjoying out, which has now been confirmed.

Creator

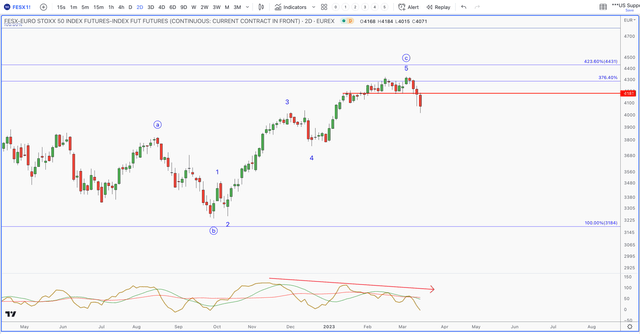

European markets have been comparatively robust this yr. For these watching, it was really just a bit behind US markets. In different phrases, the identical bearish setup was enjoying out, simply with a lag. So, whereas many have been speaking a few US breakout, we have been seeing topping patterns in European markets, which didn’t line up with a brand new bull market forming.

Creator

So, the place does that depart the US markets? From a technical perspective, the 2022 bear market doesn’t seem like over. We appear to be tracing a fairly advanced sample, which suggests another giant diploma 5 wave drop to finish the sample.

These advanced patterns are inclined to have shallow restoration rallies, very similar to we noticed in July/August, after which once more in October/January. Additionally, one other key function is that the size of every leg tends to be proportionate.

For the primary leg, which is marked “W” within the chart beneath, it broke down into 3 legs, marked A, B, C. Observe how the C wave, which bottomed in June, is strictly 150% the size of the A. Relating to the 2nd leg of this bear market, which is marked “Y”, we should always anticipate related proportions.

Apparently, if we apply the identical measurements, from the current high in February of 2023, 150% targets the 3050 SPX area. This traces up with a number of strategies mentioning the importance of this assist area. If this sample is enjoying out, we are going to loosely goal this zone for some indicators of a low being put in.

Creator

Nonetheless, we’d like affirmation that this leg is enjoying out. The first pivot shall be 3765-3750. If we break beneath right here, I might anticipate the drop to unfold fairly quickly. So long as we keep above this pivot, there may be an off likelihood that we may see another try at a bullish push greater, earlier than the subsequent leg decrease.

Peak Inflation?

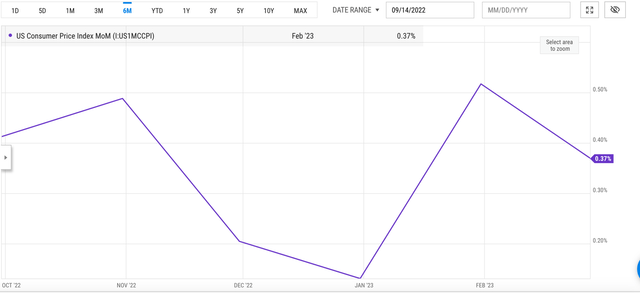

On Tuesday, the market celebrated a YoY CPI studying that was in step with expectations. Whereas equities have been up, lengthy length bonds alternatively have been down, which was a warning. That is fascinating as a result of what drives the value of lengthy length bonds shouldn’t be the Fed, however the progress and inflation outlook set by the bond market. With the Fed making an attempt to decrease charges, and the CPI print coming in as anticipated, signaling inflation is cooling, you’ll assume the bond market would rally with equities.

What the headlines weren’t discussing was that the CPI print was really a lot hotter than the YoY print was suggesting. Inflation is finest measured on a sequential foundation, not a YoY foundation. What issues is the development, not annual comparability. It is rather more necessary to see if inflation is bettering from month to month, not yr over yr, when monitoring the development.

I want to take the 3-month annualized readings to get the most effective really feel for the precise development. If you add up the prior 3 month readings and annualize them, the quantity comes out to 4.08%, in contrast with final month’s studying at 3.4%. This can be a regarding charge of acceleration, and marks the 2nd month in a row of an accelerated development throughout the CPI information.

Creator

Much more regarding, we’re seeing an analogous acceleration in vitality, core costs, core items, shelter, in addition to providers, which has been the largest concern relating to inflation. The explanation why providers is so regarding is as a result of it accounts for ~85% of the US GDP and it’s nonetheless increasing above its 12 month development.

Creator

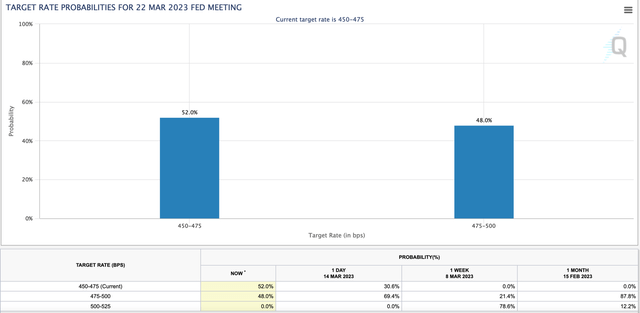

With an on-going financial growth comes inflation, which continues to indicate up within the CPI numbers. There isn’t a query the Fed, in need of a banking disaster, must enhance their terminal charge effectively above 5%, contemplating each the resilience of the US economic system and the stubbornness of inflationary pressures within the providers sector. Because of this, in mild of the troubles within the banking sector, the futures market remains to be priced in a 25 bps increase at a 50% likelihood.

CME Group

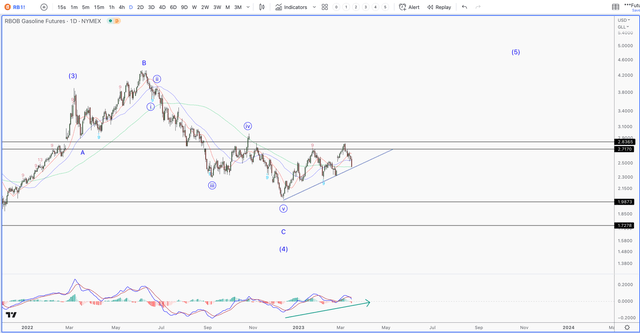

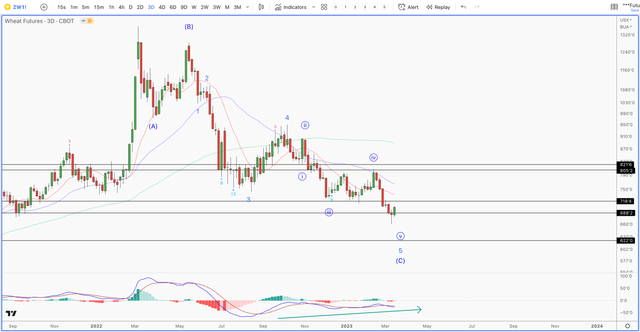

What’s extra regarding is that the present inflation readings have been for February, which was achieved with Wheat and Power commodities at subdued costs. If we have a look at these charts, from a technical perspective, they seem like both coming to the tip of their giant downtrends, or in bullish postures, suggesting a much bigger breakout is brewing.

Take gasoline, for instance. It is holding the ascending triangle sample on bullish momentum.

Creator

If we see a breakout $2.8-$3 value level, we should always see a pointy transfer greater, which might imply greater fuel costs. The identical might be mentioned with Wheat, which seems to be coming to the tip of a big diploma correction.

Creator

These charts are suggesting a transfer greater on the horizon, which might not be good for future inflation readings.

Banks Matter

When the market bottomed on October thirteenth, 2022, it did so on the day that main banks started reporting their earnings for Q3, 2022. Apparently, a number of the bigger banks stunned to the upside and even raised their 2023 steering. What turned obvious was that bigger banks have been thriving within the elevated charge setting.

By means of varied FOMC insurance policies like 0% rates of interest, operation twist, QE applications, and so forth., banks haven’t seen 30-year mortgage charges this excessive in a really very long time. Being artificially suppressed, this affected the margins. So, this modification was really a windfall for banks which have been starved for years to earn more money on the distinction they soak up for loans after which pay out on liabilities, additionally known as web curiosity earnings (NII).

For instance, JPMorgan in Q3 of 2022 reported NII of $17.6 billion, and guided for NII of $61.5 Billion for the yr, beating expectations of $58 Billion. Much more astounding, JPMorgan introduced that they at the moment have $1.2 Trillion in extra money on the time. However, JPM was not the one financial institution reporting related progress, we noticed related tales across the October lows from most main banks.

Because of this, financials led the market greater into late November, which was signaling a stronger economic system than most have been anticipating. This was one of many main the reason why we went on a spending spree in mid-late October. What’s necessary to notice is that when financials are robust, the market tends to be robust, and vice versa.

For reference, there have been two bear markets that noticed a larger than 50% drawdown in trendy market historical past: 1929, 2008. They’re extraordinarily uncommon occasions which have one widespread theme operating all through every narrative – a banking disaster.

In every occasion we noticed a uncommon phenomenon that may be summed up as a lack of confidence within the banking sector. Every occasion additionally noticed the credit score home windows shut for even fairly capitalized corporations, which solely intensified the accompanied recessions.

It is simple to dismiss the monetary sector in at the moment’s tech targeted market. In any case, financials solely account for 11% of the whole market cap of the S&P 500, with 3 sectors forward of it. Nonetheless, all corporations rely upon loans, and when banks get scared, the credit score window shuts, which tends to result in outsized bankruptcies. Bankruptcies result in unemployment, which ends up in much less spending, which snowballs the method right into a panic.

With the current fall of Silicon Valley Financial institution (SIVB), adopted by Signature Financial institution (SBNY), we noticed the 2nd and third largest financial institution failures in US historical past. In reality, the run on SIVB was the most important financial institution run in US historical past, with $2 Billion withdrawn in sooner or later. Previous to this run, Washington Mutual was the most important run, with $16.7 Billion over 10 days.

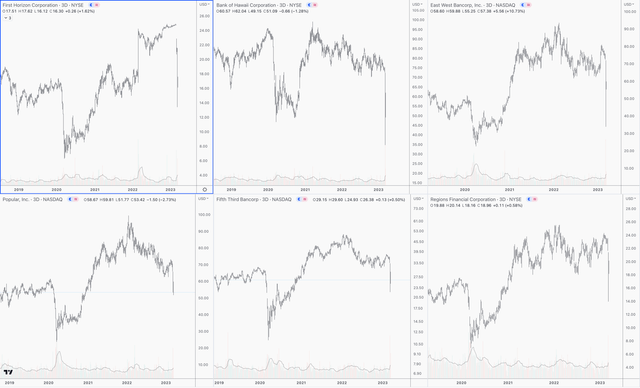

In response to the markets, the issue shouldn’t be localized. The beneath chart is a handful of bigger regional banks within the S&P 500 in addition to the SPYDR Regional Financial institution ETF (KRE). Any such drop off shouldn’t be the signal of a wholesome inventory, and we’re seeing them throughout the board.

Creator

Nobody is aware of what is going to in the end play out. We may see no additional financial institution failures, accompanied with inflation persevering with to development in direction of the Fed’s 2%. This could permit them the liberty to begin a contemporary liquidity cycle and rescue equities from any extra volatility. Nonetheless, the above charts are fairly telling and really unhealthy. They look like incomplete, and in the event that they break beneath the current panic low, anticipate the banking disaster to solely intensify.

In conclusion, markets climb a wall of fear. This was the phrase that championed one of many biggest bull markets in US historical past from 2009-2022. In any case, the market shrugged off Grexit, Brexit, the downgrading of US debt, two world slowdowns, China crash 1 and a couple of, in addition to a world pandemic (!) Why would traders not imagine it may shrug off a regional banking disaster in addition to inflation?

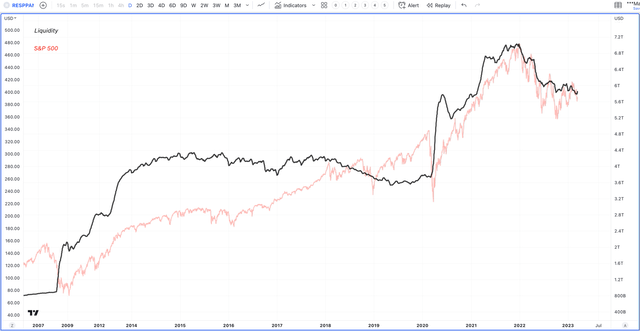

Nonetheless, the one widespread theme throughout the final bull market was that the Fed was allowed to keep up an expansive liquidity cycle as a consequence of low inflation. Even in 2016, 2019 and 2020, the Fed was capable of begin contemporary liquidity cycles earlier than the selloff result in extreme harm within the markets and economic system. Right now, the Fed is aggressively draining liquidity from the system as a method to struggle inflation, as proven within the beneath chart that compares liquidity within the system to the S&P 500

Creator

What’s troubling is that the aggressive actions taken by the Fed are beginning to have an effect on the banking sector. Nonetheless, these aggressive actions are merely not doing sufficient to quell inflation.

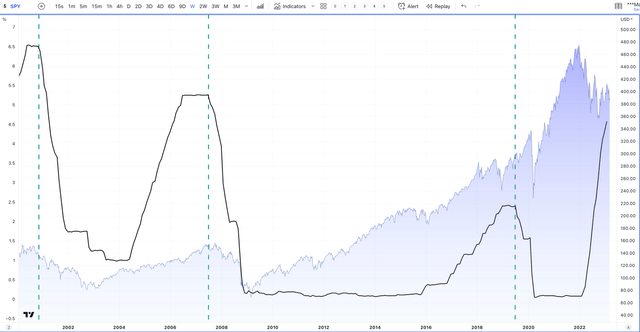

It might be argued that the FOMC will drop charges, begin a brand new liquidity cycle and save the day. Historical past means that this isn’t the case as soon as the harm is completed. It takes months for charge adjustments to filter into the economic system, and as soon as an aggressive mountain climbing cycle breaks one thing, it tends to run its course within the fairness markets earlier than a backside is discovered. The beneath chart compares the Fed Funds charge to the S&P 500. Observe when the Fed began decreasing charges, which began a contemporary liquidity cycle. Then have a look at how lengthy it takes for equities to lastly reply.

Creator

Possibly inflation will development decrease going ahead, and possibly no extra banks may have hassle; possibly, we’re lacking out on a chance to purchase equities at decrease costs simply earlier than a brand new bull market is about to begin up. This can be a very skinny needle that should be threaded, and till we get proof it’s manifesting, we stay cautious.

{kind=link}