Scharfsinn86

Be aware: I’ve coated Ballard Energy Techniques (NASDAQ:BLDP) beforehand, so traders ought to view this as an replace to my earlier articles on the corporate.

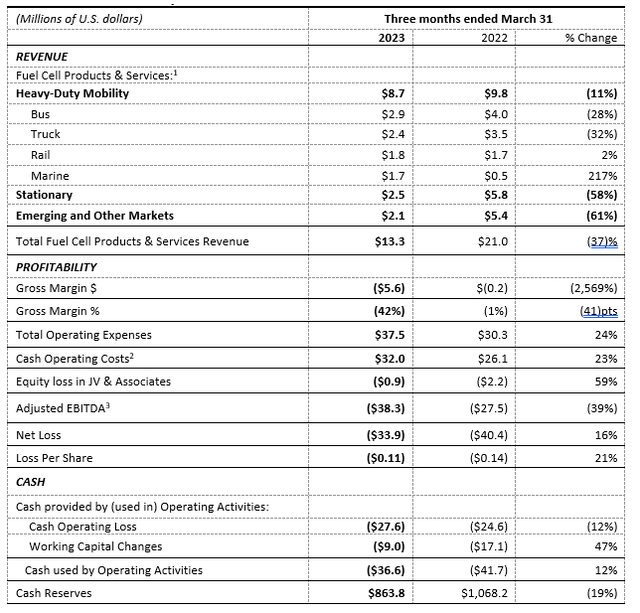

On Tuesday, main Canadian gas cell programs developer Ballard Energy Techniques (“Ballard” or “Ballard Energy”) reported one other set of abysmal quarterly outcomes:

Firm Press Launch

As soon as once more, the corporate missed consensus income expectations by a mile. As well as, consolidated gross margin of damaging 42% represented a brand new multi-year low for Ballard Energy with strain anticipated to persist nicely into subsequent yr:

As beforehand communicated, we proceed to see gross margin pressures into 2024 given our income combine, pricing technique, investments in manufacturing capability, and timing lag earlier than our manufacturing volumes ramp and our product price discount initiatives transfer into manufacturing.

The corporate’s money utilization remained important as the corporate recorded damaging free money circulation of $49.1 million.

That mentioned, Ballard Energy nonetheless instructions greater than $860 million in money and money equivalents, adequate to fund the enterprise for as much as 4 years on the present tempo of money burn.

Firm Press Releases and Regulatory Filings

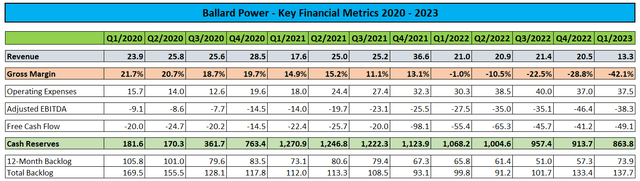

Whereas the corporate’s whole backlog elevated barely to new multi-year highs in Q1, order consumption was truly down considerably from the very sturdy This fall quantity.

That mentioned, Ballard Energy managed to extend its 12-month backlog by virtually 30% sequentially however based mostly on administration’s statements on the convention name, full-year revenues are prone to are available in between $85 million and $90 million, nicely under the present analyst consensus.

Assuming damaging gross margin of 20% and utilizing administration’s projections for working bills ($135 million to $155 million) and capital expenditures ($40 million to $60 million), I might estimate the corporate’s money burn to be between $200 million and $235 million this yr.

The corporate’s struggles in China continued through the fourth quarter with product revenues derived from the corporate’s much-touted three way partnership with Weichai Energy a measly $0.3 million for Q1.

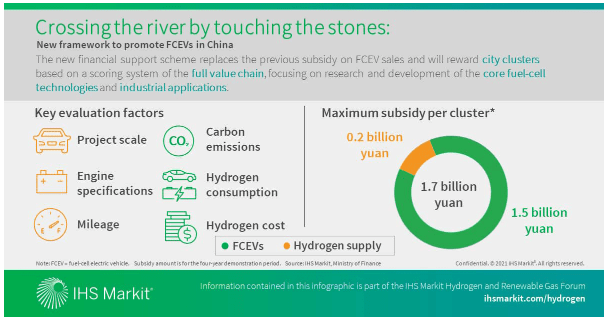

Even worse, the Chinese language market is unlikely to choose up anytime quickly because the central authorities’s newest subsidy strategy is directed in the direction of establishing an entire home gas cell know-how and hydrogen provide chain over time thus leading to restricted impression on near-term FCEV adoption.

IHS Markit

The truth is, the Chinese language authorities’s revised subsidy strategy has resulted within the requirement for the corporate to ascertain home operations in a hydrogen cluster eligible for presidency subsidies to keep away from aggressive disadvantages and circumvent anticipated import tax will increase.

Consequently, Ballard Energy has determined to speculate $130 million in a brand new, large-scale MEA manufacturing and R&D facility in Shanghai regardless of the obvious danger of the corporate’s core MEA mental property being accessed by home opponents now.

However even with the beginning of Chinese language manufacturing operations not scheduled earlier than 2025, administration nonetheless expects utilization of the brand new facility to be “comparatively low” initially.

Given the continued uncertainties in China, administration has delayed funding within the new Shanghai facility in the intervening time.

Backside Line

Ballard Energy Techniques reported one other disappointing quarter with revenues nicely under consensus expectations, sizeable money burn and abysmal gross margins.

Primarily based on administration’s statements on the convention name, the corporate is prone to miss each Q2 and full-year income expectations by a large margin.

As well as, Ballard Energy stays caught between a rock and a tough place in China with the federal government’s newest subsidy framework principally forcing the corporate to ascertain home manufacturing operations for its core MEA product with the obvious danger of home opponents accessing Ballard’s IP.

Given the continued lack of near-term catalysts, traders ought to proceed to keep away from the shares.

{kind=link}