Shutter2U

Tectonic Therapeutic, Inc. (NASDAQ:TECX) is a pioneering biotechnology firm devoted to discovering and creating therapeutic biologics concentrating on G-protein-coupled receptors (GPCRs) by way of its proprietary platform, GPCRs Engineered for Optimum Discovery (GEODe). TECX emerged after a current merger with Avrobio, Inc. (AVRO), combining AVRO’s gene remedy experience with Tectonic’s GPCR-targeted protein improvement. At the moment, TECX’s main drug candidate is TX45, a Fc-relaxin fusion protein in Section 1 for pulmonary hypertension resulting from coronary heart failure with preserved ejection fraction (HFpEF). I imagine TECX trades at a comparatively low-cost valuation in comparison with friends, however its early-stage analysis tempers my optimism. I in the end lean impartial on the inventory as a result of I see the professionals and cons offsetting one another.

TX45: Enterprise Overview

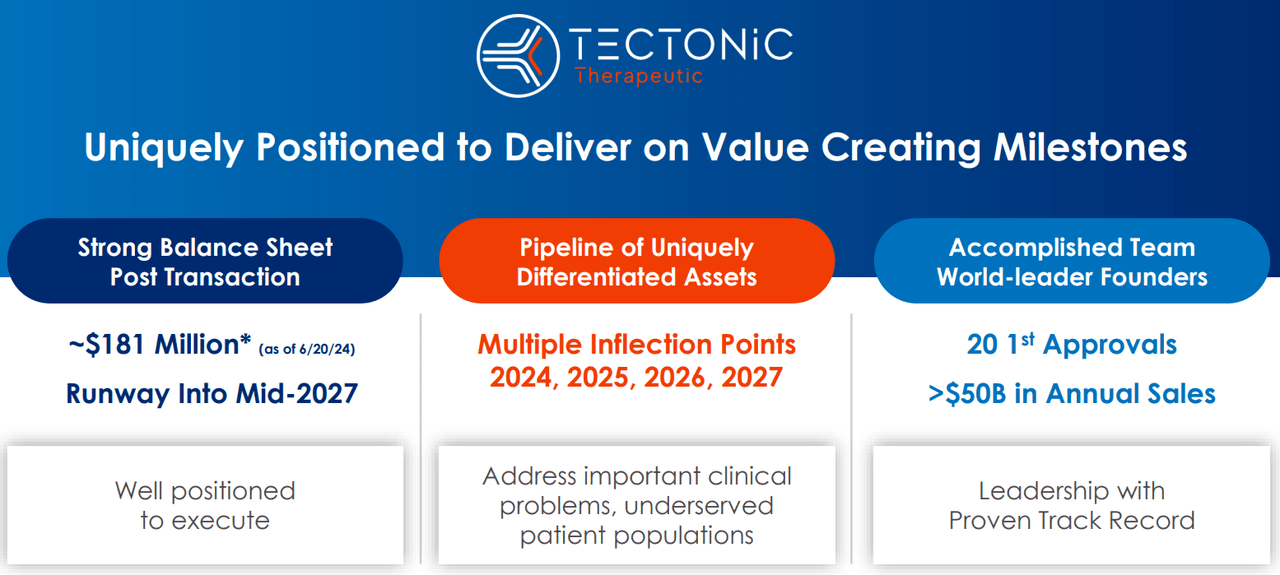

Tectonic Therapeutic is a biotechnology firm that discovers and develops therapeutic biologics concentrating on G-protein-coupled receptors (GPCRs) utilizing its proprietary platform, GPCRs Engineered for Optimum Discovery (GEODe). Tectonic Therapeutic is headquartered in Watertown, Massachusetts. The corporate was based in 2018 and went public after it closed a reverse merger with AVRO on June 20, 2024. Following the merger, the brand new entity started buying and selling below the ticker TECX. The merger mixed Avrobio’s gene experience with Tectonic’s revolutionary GPCR-targeted proteins. The corporate additionally did a $130.7 million personal placement to finance medical trials.

In whole, the reverse merger break up AVRO inventory at a ratio of 1:12 and altered its title to Tectonic Therapeutics, Inc. Nevertheless, the corporate retained TECX’s legacy operations, property, and analysis applications. Extra not too long ago, on July 30, 2024, TECX acquired FDA authorization for its Investigational New Drug [IND] software for TX45. Since then, TECX has been engaged on TX45 for pulmonary hypertension [PH] resulting from coronary heart failure with preserved ejection fraction [HFpEF]. It’s value mentioning that this extreme situation impacts over 600,000 individuals within the US, and there aren’t any presently out there authorized remedies.

Supply: Company Presentation. July 2024.

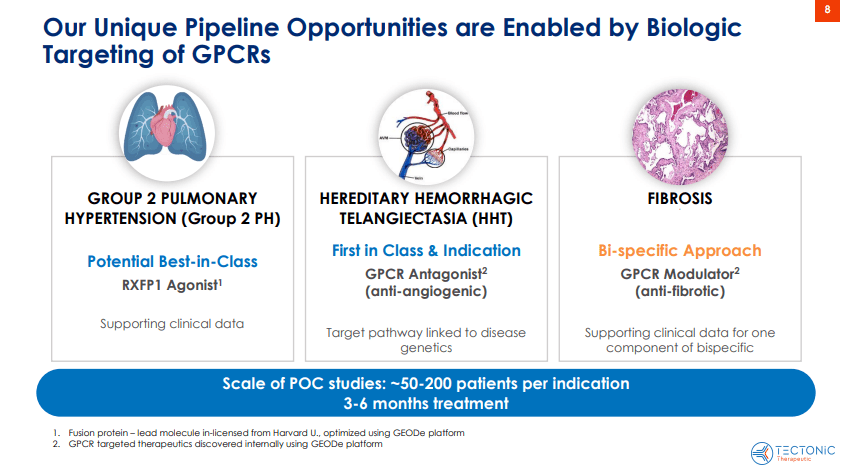

Subsequently, TECX’s pipeline presently contains TX45, a doubtlessly best-in-class Fc-relaxin fusion protein that prompts the relaxin/insulin-like household peptide receptor 1 (RXFP1). This receptor is a part of the GPCR household and is said to vasodilation and anti-fibrotic results. TX45 targets this receptor and induces its vasodilatory and anti-fibrotic results, theoretically treating cardiovascular and fibrotic circumstances. It’s value noting that the Fc area enhances the steadiness and length of relaxin’s results, additionally enabling much less frequent dosing and enhancing efficacy.

Most important Worth Driver: TX45

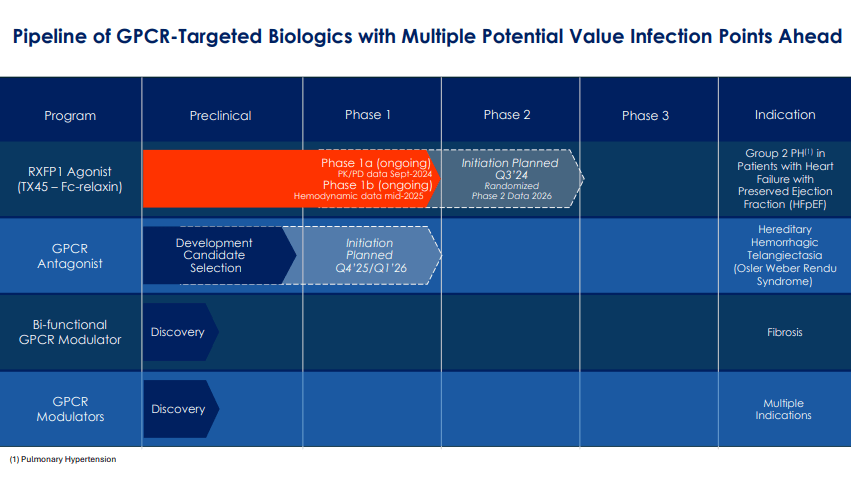

At the moment, TX45 is a Section 1 drug candidate for PH in sufferers with HFpEF. On this situation, the guts’s left ventricle retains its capacity to pump blood however can not calm down and fill with blood throughout diastole, resulting in signs similar to shortness of breath and fluid retention. TECX’s Section 1a trial outcomes on pharmacokinetic/pharmacodynamic (PK/PD) results are anticipated by September 2024, and TX45’s Section 1b outcomes will present proof-of-concept knowledge by mid-2025. TECX plans to begin a Section 2 trial, with topline knowledge anticipated by 2026. From a technical perspective, TX45 leverages insights from prior medical trials on serelaxin’s potential advantages and challenges in treating acute coronary heart failure [AHF]. Since TX45 is an Fc-relaxin fusion protein, it builds on earlier AHF knowledge. Nevertheless, this analysis on AHF confirmed challenges, primarily concerning pharmacokinetic limitations similar to a brief half-life.

Supply: Company Presentation. July 2024.

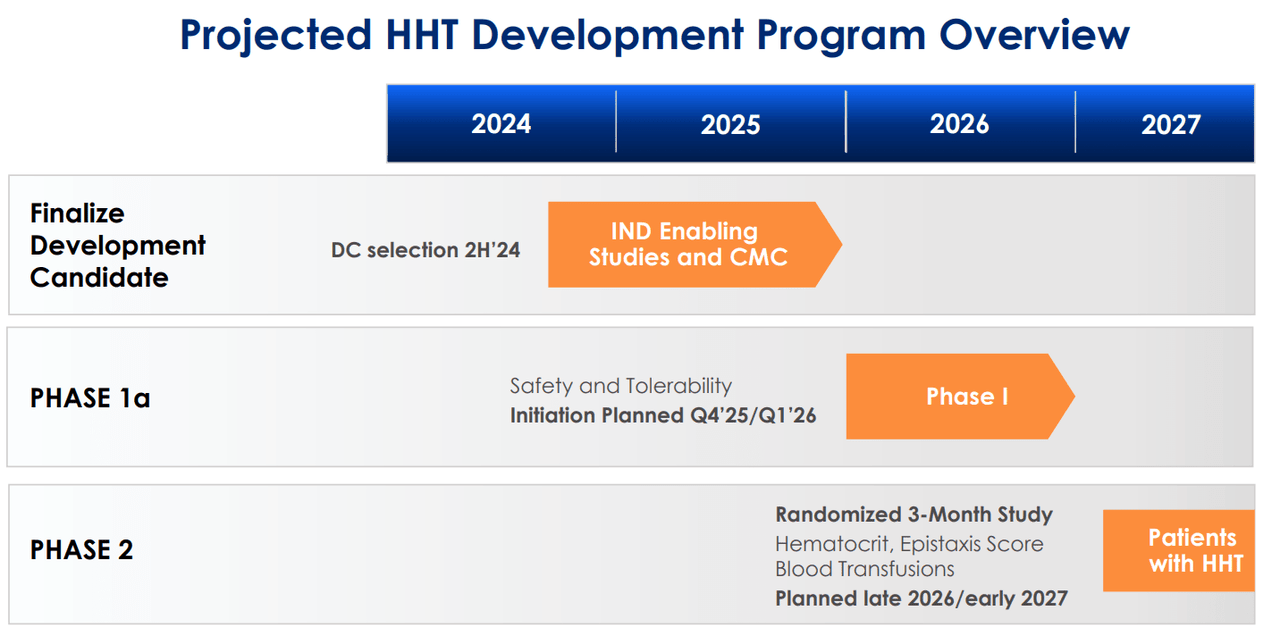

Moreover, TECX’s pipeline additionally features a GPCR antagonist for hereditary hemorrhagic telangiectasia [HHT], often known as Osler-Weber-Rendu Syndrome. HHT is a genetic dysfunction that impacts blood vessels and is characterised by creating dilated blood vessels within the pores and skin or mucous membranes, which may trigger bleeding. HHT sometimes causes bigger irregular blood vessels within the lungs, liver, mind, and intestines, which may result in severe issues. Thus, TECX is engaged on a Section 1 trial for a GPCR antagonist deliberate for This fall 2025 or Q1 2026. The corporate can also be creating a bifunctional GPCR modulator for fibrosis and different GPCR modulators that would goal a number of ailments. Nevertheless, these GPCRs are nonetheless within the discovery stage.

TECX’s Science: Potential and Challenges

Subsequently, TECX’s underlying strategy facilities round GPCRs, that are cell-surface receptors concerned in mobile communication and sign transduction. GPCRs convert extracellular indicators into practical responses. Thus, TECX’s GEODe platform discovers and optimizes proteins and antibodies concentrating on these GPCRs. The GEODe platform features a receptor engineering and purification system and an in-vitro yeast show library that screens antibody interactions in opposition to GPCRs. It additionally supplies a protein reengineering technique that optimizes protein pharmacology and modifies antigen constructions for agonists and antagonists. This manner, the GEODe platform discovers and develops biologics particularly concentrating on GPCRs.

Supply: Firm’s web site.

Nevertheless, TECX’s analysis faces key challenges: 1) maintaining the GPCR construction, 2) purifying the goal receptor sufficiently, 3) inducing an immune response, and 4) stabilizing the receptor for drug discovery. Nevertheless, it’s key to notice that GPCRs are extremely complicated and dynamic proteins embedded in cell membranes. Replicating them reliably in vitro is extremely complicated, so I believe this analysis strategy is susceptible to blended trial outcomes or ineffective drug candidates. In spite of everything, the candidates are generated based mostly on in vitro GPCRs, not GPCRs in cell membranes.

Whereas it’s true that TECX purifies its GPCRs, the purification course of is difficult as a result of it should keep the GPCR’s native construction outdoors the mobile atmosphere. The purpose is to make use of these GPCRs to elicit particular immune responses with out triggering hostile results. Nevertheless, this requires secure GPCRs, that are inherently extremely unstable outdoors mobile membranes. I imagine this provides a danger layer to TECX’s funding thesis, particularly for an organization with just one Section 1 drug candidate.

Blended Image: Valuation Evaluation

From a valuation perspective, there are roughly 14.7 million shares excellent. TECX’s present inventory value is $17.15, so the implied market cap is $252.7 million, making it a microcap biotech. On March 31, 2024, its post-merger steadiness sheet held $203.4 million in money and equivalents. The mixed entity had no monetary debt, and its whole liabilities amounted to $33.8 million. Its ebook worth was $179.2 million, indicating an inexpensive P/B a number of of 1.4. For comparability, its sector median P/B is 2.4, so TECX appears low-cost from that viewpoint. Administration not too long ago talked about that they’ve $181.0 million in assets and anticipate having sufficient money runways by mid-2027.

Supply: Company Presentation. July 2024.

That’s not terribly good, but it surely ought to be sufficient to get TX45 into Section 2 trials, assuming all the pieces goes in accordance with plan. Till then, I perceive the market’s seemingly conservative appraisal of TECX’s prospects. However, it’s clear that TECX doesn’t have sufficient assets to fund its analysis all the best way to an FDA approval, so it’ll doubtless faucet the capital markets once more within the subsequent few years. If it reveals better-than-expected knowledge by then, the inventory is perhaps favorably priced to mitigate dilution dangers.

Nevertheless, administration’s money runway expectations sign a comparatively excessive money burn. If it doesn’t yield thrilling outcomes, the inventory may merely decline slowly over time. Since TECX’s valuation is already fairly depressed, it may end in a capital elevate at a comparatively unfavorable valuation. In spite of everything, if $203.4 million in money and equivalents lasts three years, that’s roughly $67.8 million in money burn per 12 months. Sometimes, biotech corporations elevate 2 to three years’ value of money runway, so if TECX hits the capital markets once more at its present $252.7 million valuation or worse, the dilution can be appreciable.

Supply: Company Presentation. July 2024.

Furthermore, getting its analysis as much as Section 2 remains to be considerably early-stage, particularly for this complicated GPCR strategy. Subsequently, I stay skeptical about its value appreciation prospects, even when it obtains promising Section 2 trial knowledge. Furthermore, the timeline for this funding would nonetheless require a few years till significant progress is seen. Consequently, I believe it’s prudent to lean impartial on the inventory, which is why I charge TECX a “maintain” for now.

Caveats: Threat Evaluation

Naturally, the draw back dangers largely give attention to its GPCR-targeted analysis and money burn. As I beforehand famous, GPCR analysis seems comparatively complicated and is perhaps susceptible to blended trial knowledge. Even whether it is in the end confirmed efficient, it’d nonetheless take longer and be costlier than initially anticipated. If any of those dangers materialize, they might doubtless translate into a better money burn or power TECX right into a capital elevate below unfavorable circumstances.

Supply: TradingView.

Nevertheless, there’s a potential upside for TECX at this juncture. Specifically, its valuation a number of seems favorable relative to its friends. Furthermore, if its analysis is profitable and catches the eye of bigger pharma gamers, it’d make TECX an excellent takeover candidate. Subsequently, I believe the positives and negatives offset one another, so I in the end lean impartial on the inventory. Nevertheless, I imagine TECX is value including to your watchlist in case its funding profile adjustments.

Impartial Stance: Conclusion

General, I believe post-merger, TECX has an intriguing strategy with its GPCR analysis. Nevertheless, there are just too many variables at play to make a particular name both manner on the inventory, so I believe it’s prudent to lean impartial on it for now. Whereas I acknowledge its upside potential by way of its analysis and comparatively low-cost valuation, I even have considerations about its early-stage analysis and potential long-term dilution dangers. TECX is value including to your watch record, however not your funding portfolio.

{kind=link}