SweetBunFactory

Funding motion

I really helpful a purchase score for Analog Gadgets, Inc. (NASDAQ:ADI) once I wrote about it the final time. As I anticipated, FY24 to be the trough of this cycle, the enterprise ought to begin to see optimistic development inflection. Primarily based on my present outlook and evaluation, I like to recommend a purchase score. 1Q24 efficiency strengthened my view that FY24 is more likely to see a restoration, and FY25 ought to see development speed up. The robust gross margin efficiency, continued deal with driving down stock surplus, and intention to herald the manufacturing course of additionally led me to consider margin will develop from right here and can stay structurally increased transferring ahead.

Evaluation

In 1Q24, ADI reported income of $2.513 billion, down 7.5% sequentially and 22.7% vs. 4Q22, coming simply modestly above the consensus estimate of $2.5 billion. Breaking down by segments, automotive noticed 2% sequential development; customers noticed 7% sequential decline; communications noticed 10% sequential decline; and industrial noticed 12% sequential decline. This was just about anticipated as clients continued to work down stock within the quarter. Non-GAAP gross margin got here in at 69%, 30bps above the consensus 68.7% estimate. Non-GAAP EPS was additionally modestly above estimates, at $1.73 vs. $1.71.

I proceed to view the outlook as optimistic for ADI, reiterating my purchase score. First, the reserving momentum remains to be going robust. In 1Q24, administration famous a lower in cancellations and a broad-based sequential enhance in complete bookings. The extra vital factor to notice right here is that book-to-bill may surpass 1x in FY24 (normalized sample), as I anticipate shoppers to start out inserting orders that higher signify precise consumption charges, making it simpler for traders to mannequin the restoration trajectory forward. This could occur in 2H24, since 1Q24 exhibits that there’s nonetheless stock to be processed. Moreover, ADI witnessed a sturdy discount in stock. In keeping with the newest steadiness sheet figures, ADI managed to scale back its stock by $90 million within the quarter, and administration’s intention is to additional scale back stock by $50–100 million in 2FQ24. Although the stock correction will damage income within the brief time period, I feel it is a sensible transfer by administration to handle the corporate’s elevated stock and the unsure demand backdrop. For reference, stock days are nonetheless at 131, so the deal with drawing down stock is the suitable transfer, I consider.

Encouragingly, first quarter bookings improved sequentially, rising our confidence that inventory-related headwinds will largely subside this quarter.

And that offers us the boldness, because the book-to-bill approaches unity, that we have seen the worst of the stock correction, and within the second half, we’ll get again to a extra normalized development sample. 1Q24 name

Shifting down the P&L, I believed one of many line gadgets that deserves complement is the gross margin resiliency regardless of aggressive manufacturing cuts (the concept is that decrease quantity means decrease fastened price protection, so margins ought to get depressed). Nonetheless, that’s not the case. Regardless of decreased income, manufacturing cuts, and decrease industrial income (product combine headwinds), I feel administration did a very good job of defending margins. If we check with my earlier publish, the place I confirmed the historic downcycle influence on gross margin, I consider 1Q24 efficiency and administration 2Q24 steerage for 67%—simply 200bps sequential decline vs. the bigger sequential decline—counsel that the trough to gross margin is close to (excessive 60+% is my guess). Trying forward, as quantity recovers, I anticipate margins to be structurally increased than previously as administration intends to shift manufacturing away from exterior foundries and towards inside capability.

Lastly, concerning money move, it was nice to listen to that Capex is on the best way to reaching a normalized degree in FY25. Administration intends to drastically minimize capital expenditure after FY2024, since they’ve achieved their goal of doubling front- and back-end inside capability. Primarily based on the data offered at their 2022 Investor Day, I’m anticipating ADI to spend 4–6% of their income on CAPEX on a normalized foundation. This can be a lower from 10% in FY2023 and 7-8% in FY24 (the steerage for FY24 was for $700 million, and with consensus income estimates of $9.1 billion, this quantities to roughly 7.6%). What this implies is that we should always see a powerful enchancment in FCF that can be utilized to proceed the share buyback development up to now (share excellent diminished from 537 million in FY21 to 498 million in FY23).

During the last two years we have invested document ranges of CapEx to develop our capability and to boost resiliency. Now, with line of sight to reaching our aim of doubling entrance and back-end inside capability in 2025, we’ll start to considerably scale back our capital spend. 1Q24 name

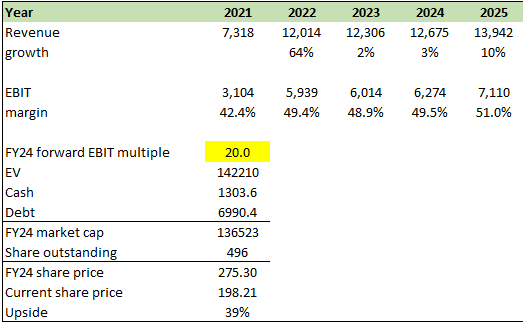

Valuation

Creator’s work

I nonetheless consider ADI can see a restoration in FY24, because the efficiency in 1Q24 confirmed that the decline in development is a restoration, and the underlying state of affairs with stock is working in the suitable course. My expectation on the restoration trajectory stays the identical as in my earlier mode: 3% in FY24 and 10% in FY25. This follows my earlier evaluation of ADI historic development efficiency post-each downturn. Nonetheless, I’ve adjusted my EBIT margin expectations down by 200bps to replicate the 67% gross margin expectation for FY24. My earlier expectation was that 69% gross margin was the trough; therefore, to replicate this variance, I adjusted my expectations down. That stated, the trajectory stays the identical, in that I anticipate EBIT margin to proceed increasing as quantity improves and ADI brings manufacturing in home. For valuation, I now anticipate valuation to commerce at 20x ahead EBIT, a 3x enchancment from my earlier assumption, as I underestimate the market capability to look ahead into FY25 and past (ADI absolutely acquired previous this down cycle), as could be seen from the present ahead EBIT a number of of 27x. That stated, I’m staying conservative, assuming that ADI solely trades on the excessive finish of its valuation vary (14x to 21x ahead EBIT).

Threat and last ideas

I quote from my earlier publish, the foremost danger for traders investing in ADI in the present day: timing of restoration. My complete thesis is predicated on a restoration in 2H24. If this doesn’t occur, which may simply consequence from any of the present macro crises (the Crimson Sea battle inflicting freight prices to go means up; the Russia/Ukraine battle blowing up, thereby underlying demand; the China/Taiwan battle blowing up, which causes a significant shock to the complete semiconductor trade; and so forth.), On condition that valuation is at very excessive ranges, the market may very nicely re-rate this downwards on an unsure outlook (identical to the way it re-rates it upwards as a result of optimistic expectations).

All in all, my purchase score for ADI stays. The reserving momentum in 1Q24 suggests a restoration is underway. Regardless of decrease volumes reported within the quarter, administration did a very good job of defending gross margins. Moreover, administration’s intention to normalize capital expenditures in FY25 signifies a possible surge in free money move. Whereas the precise timing of the restoration hinges on exterior components, ADI seems well-positioned to capitalize on a development trajectory that begins in 2H24 and accelerates in FY25. Whereas the present valuation is excessive, even when I have been to imagine a conservative a number of, the upside remains to be engaging.

{kind=link}