Thomas Barwick/DigitalVision through Getty Photos

Overview

Amadeus IT Group (OTCPK:AMADF) is without doubt one of the main suppliers of IT options to the airline trade, offering airways with entry to one of many world’s largest international distribution techniques [GDS] and providing a spread of software program options to the airline trade.

Beforehand, I mentioned my beliefs that AMADF is a promising lengthy for these in search of publicity to the airline trade and the expertise providers that help it. Regardless of the mature nature of the worldwide distribution techniques trade, AMADF has room for growth by means of cross-selling and new buyer acquisition. As well as, its hospitality enterprise can also be a promising space of progress.

Simply as I anticipated, the enterprise continues to do nicely in Air Info Expertise [IT] which I proceed to see compelling medium-term structural air journey progress tailwinds. Despite the fact that quantity was barely weak, AMADF has maintained its pricing energy within the Distribution sector by capitalizing on the product’s stickiness. Though the bear case will proceed to concentrate on the bookings restoration trajectory in Distribution, I consider that Air IT’s continued robust efficiency, with revenues now above pre-COVID ranges, will develop into the primary bulk of the AMADF thesis going ahead. Lastly, administration has resumed its share buyback program, which is in keeping with my expectation and additional helps my view that enterprise is prospering and has resumed its cash-generating mode. I reiterate my purchase ranking.

Journey restoration

For my part, AMADF has not but reaped the total advantages of the uptick in air journey demand. Though the worldwide air visitors restoration development is continuous as anticipated, it’s now dominated by home short-haul flights as shoppers change to low-cost carriers (LCCs) that rely much less on the GDS channel (comparable to AMADF). Moreover, AMADF doesn’t instantly profit from the latest months’ vital restoration of air visitors as a result of it doesn’t embody home China visitors in its portfolio. Nonetheless, which means that AMADF will develop at a sooner charge when the economic system improves, because the restoration of long-haul flights will necessitate a larger reliance on GDS. The resumption of trans-Asian transportation hyperlinks to and from China is nice information for AMADF as nicely. That is vital for AMADF as a result of the it has a big place in Asia because the preeminent distributor and supplier of Passenger Service Methods.

Share buyback program

AMADF has formally introduced the beginning of its share repurchase program. The utmost buyback underneath this system is €433.3 million, or about 1.3% of the corporate’s present market cap. Though this buyback will enhance returns barely, the truth that administration is assured sufficient to return capital is the extra essential takeaway. Which is a mirrored image of the robustness of underlying demand. Given its capability to lever up its stability sheet (see my earlier submit for particulars), I anticipate AMADF will ultimately return to its historic share buyback profile.

Laborious to resolve if AI is nice or unhealthy at the moment

It’s at present tough to find out whether or not AI poses a danger to AMADF. As there are a number of views on this which are tough to validate, I consider it’s best to stay impartial on generative AI till we see extra proof of how issues play out. The destructive narrative is that it’s going to result in consolidation amongst journey businesses as a result of the bigger participant will have the ability to use AI to additional scale the enterprise (bigger participant has extra information and advertising energy, for instance). The subscale participant, however, will merely be swallowed by a bigger participant as a result of they lack the mandatory scale to amass stock and distribute it. In consequence, a bigger journey company buyer would have extra bargaining energy when it got here to incentive charges. This may very well be a significant problem, however I am undecided how a lot negotiating energy the journey brokers can have as a result of the entrance desk employees is already well-trained to make use of AMADF. It is going to even be tough for them to tear out and substitute with one other system, as AMADF is conscious.

There’s additionally the likelihood that giant tech gamers with superior AI will enter the GDS area. That is potential, however the worth of GDS lies within the reside connections to airline stock, not in search. In consequence, the massive tech corporations will nonetheless have to make use of AMADF information, for which AMADF can cost a payment. Moreover, coaching the fashions should be based mostly on journey information, and the GDS is the trade’s common information aggregator.

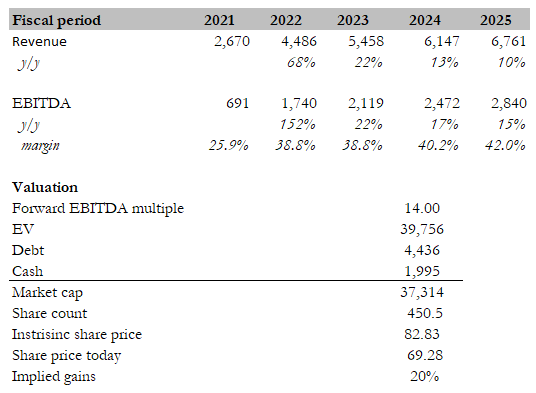

Valuation

I modelled AMADF to develop at an elevated tempo in FY23 and FY24 because it experiences the total restoration of long-haul and Asia flights, and progress to return to historic excessive single digits – low-teens progress. This will probably be accompanied by margin growth as AMADF continues to boost costs (excessive margins) and see larger combine from Air IT providers. Given AMADF scale and potential for elevated progress, I consider it deserves to commerce at a premium to Sabre Corp (SABR) which is buying and selling at 12x EBITDA at the moment.

Personal mannequin

Dangers

Firstly, the potential influence of worse-than-expected macro circumstances poses a danger to the corporate’s total outlook. Financial elements comparable to inflation, rates of interest, and international market volatility can considerably affect enterprise operations and shopper habits, thereby affecting the corporate’s monetary efficiency.

Secondly, one other key danger lies within the slower restoration of air journey following the COVID-19 pandemic. As the corporate operates in an trade carefully tied to air journey, any delays or setbacks within the restoration of this sector may have hostile results on its income and profitability. Elements like extended journey restrictions, lowered shopper confidence, or the emergence of latest variants can hinder the resumption of air journey to pre-pandemic ranges, probably prolonging the corporate’s restoration timeline.

Conclusion

I count on AMADF to proceed driving the wave of journey restoration. Regardless of the present dominance of home short-haul flights and the exclusion of home China visitors from its portfolio, AMADF’s robust efficiency within the Air IT sector, with revenues surpassing pre-COVID ranges, stays a compelling issue. The corporate’s share buyback program and its capability to leverage its stability sheet point out confidence in its underlying demand. Whereas the influence of AI on AMADF is unsure, you will need to stay impartial till extra proof emerges.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please pay attention to the dangers related to these shares.

{kind=link}