Spreadsheet data updated daily

Updated on October 14th, 2022 by Bob Ciura

Individual products, businesses, and even entire industries (newspapers, typewriters, horse and buggy) go out of style and become obsolete.

Perhaps more than any other industry, agriculture is here to stay. Agriculture started around 14,000 years ago. It’s a safe bet we will be practicing agriculture far into the future.

And, the growth of the global population is tied to increasing agricultural efficiency. The agricultural revolution allowed greater population growth (and led to the industrial revolution).

As the global population grows, so does the need for improved agricultural production. This creates a long-term demand driver for agriculture stocks.

You can download the complete list of all 43 agriculture stocks (along with important financial metrics such as price-to-earnings ratios, dividend yields, and dividend payout ratios) by clicking on the link below:

The agriculture stocks list was derived from two major exchange-traded funds. These are the AgTech & Food Innovation ETF (KROP) and the iShares Global Agriculture Index ETF (COW).

Investing in farm and agriculture stocks means investing in an industry that:

- Has stable long-term demand

- Has withstood the test of time, and is extremely likely to be around far into the future

- Benefits from advancing technology

This article analyzes 7 of the best agriculture stocks in detail. You can quickly navigate the article using the table of contents below.

Table of Contents

We have ranked our 7 favorite agriculture stocks below. The stocks are ranked according to expected returns over the next five years, in order of lowest to highest.

Even better, all 7 agriculture stocks pay dividends to shareholders, making them attractive for income investors. Interested investors should view this as a starting off point to more research.

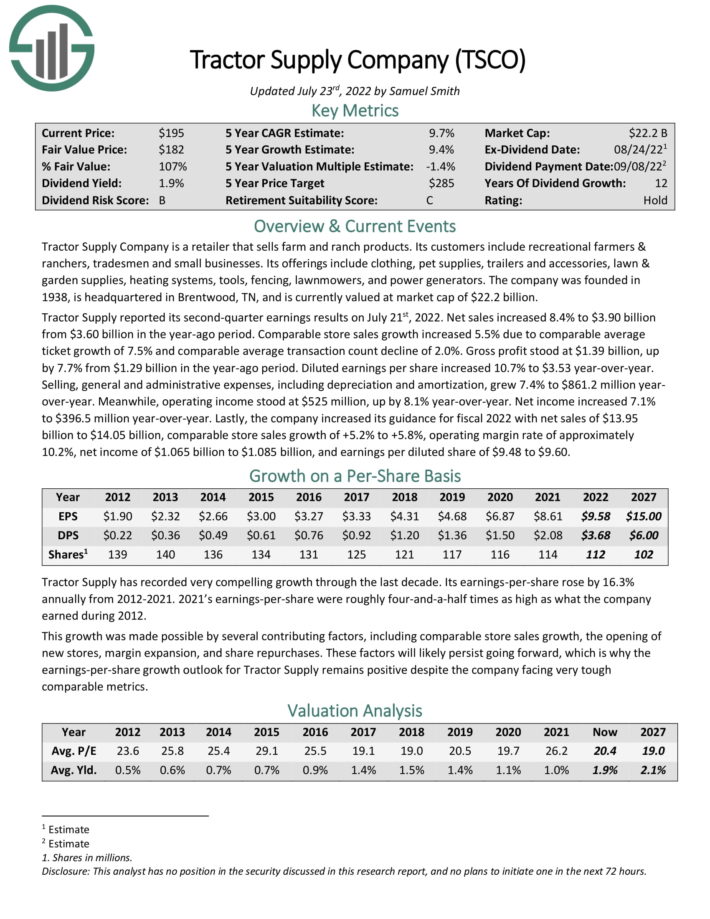

Agriculture Stock #7: Tractor Supply Company (TSCO)

- 5-year expected annual returns: 8.9%

Tractor Supply Company is a retail stock that sells farm and ranch products. Its customers include recreational farmers & ranchers, tradesmen and small businesses. Its offerings include clothing, pet supplies, trailers and accessories, lawn & garden supplies, heating systems, tools, fencing, lawnmowers, and power generators.

Tractor Supply reported its second-quarter earnings results on July 21st, 2022. Net sales increased 8.4% to $3.90 billion from $3.60 billion in the year-ago period. Comparable store sales growth increased 5.5% due to comparable average ticket growth of 7.5% and comparable average transaction count decline of 2.0%.

Source: Investor Presentation

Diluted earnings per share increased 10.7% to $3.53 year-over-year. Net income increased 7.1% to $396.5 million year-over-year. Lastly, the company increased its guidance for fiscal 2022 with net sales of $13.95 billion to $14.05 billion, comparable store sales growth of +5.2% to +5.8%, operating margin rate of approximately 10.2%, net income of $1.065 billion to $1.085 billion, and earnings per diluted share of $9.48 to $9.60.

We expect annual returns of 8.9% per year, consisting of 9.4% expected EPS growth, the 1.8% dividend yield, partially offset by a small negative annual return from a declining P/E multiple.

Click here to download our most recent Sure Analysis report on TSCO (preview of page 1 of 3 shown below):

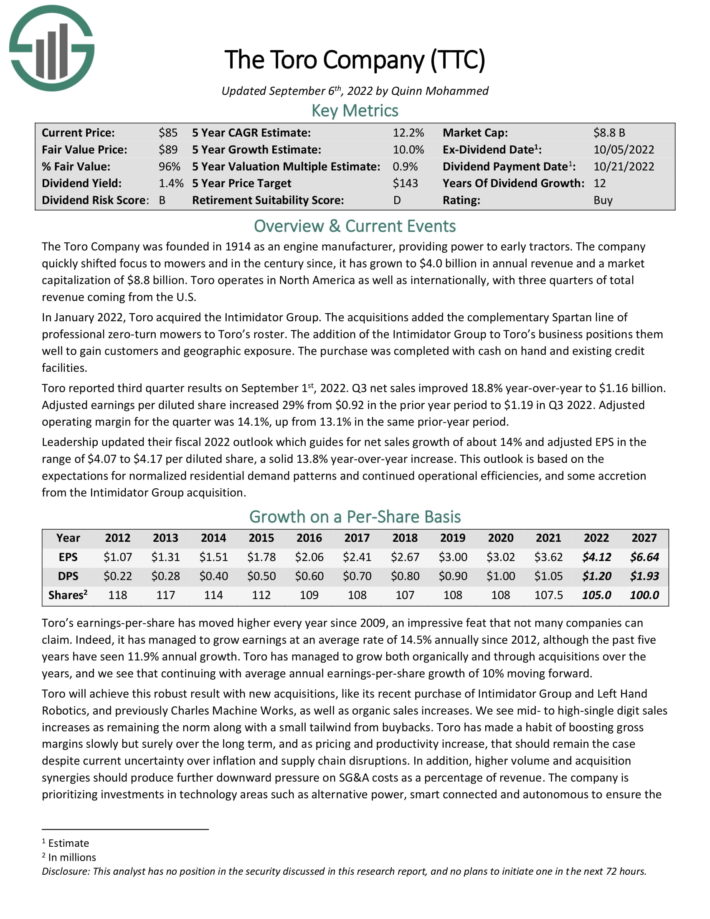

Agriculture Stock #6: The Toro Company (TTC)

- 5-year expected annual returns: 9.7%

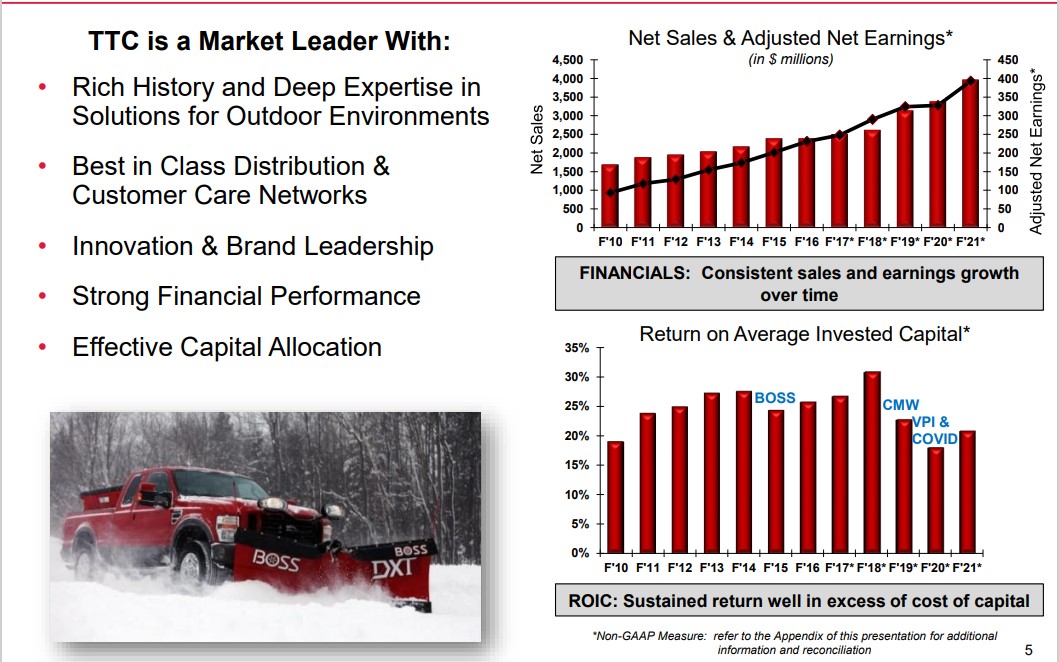

The Toro Company was founded in 1914 as an engine manufacturer, providing power to early tractors. The company quickly shifted focus to mowers and in the century since, it has grown to $3.4 billion in annual revenue. Toro operates in North America as well as internationally, with three quarters of total revenue coming from the United States.

Source: Investor Presentation

In January 2022, Toro acquired the Intimidator Group. The acquisitions added the complementary Spartan line of professional zero-turn mowers to Toro’s roster. The addition of the Intimidator Group to Toro’s business positions them well to gain customers and geographic exposure. The purchase was completed with cash on hand and existing credit facilities.

Toro reported third quarter results on September 1st, 2022. Q3 net sales improved 18.8% year-over-year to $1.16 billion. Adjusted earnings per diluted share increased 29% from $0.92 in the prior year period to $1.19 in Q3 2022. Adjusted operating margin for the quarter was 14.1%, up from 13.1% in the same prior-year period.

Leadership updated their fiscal 2022 outlook which guides for net sales growth of about 14% and adjusted EPS in the range of $4.07 to $4.17 per diluted share, a solid 13.8% year-over-year increase. This outlook is based on the expectations for normalized residential demand patterns and continued operational efficiencies, and some accretion from the Intimidator Group acquisition.

We expect annual returns of 9.7% per year over the next five years, driven by 10% EPS growth, the 1.2% dividend yield, and a small reduction due to a declining P/E multiple.

Click here to download our most recent Sure Analysis report on The Toro Company (preview of page 1 of 3 shown below):

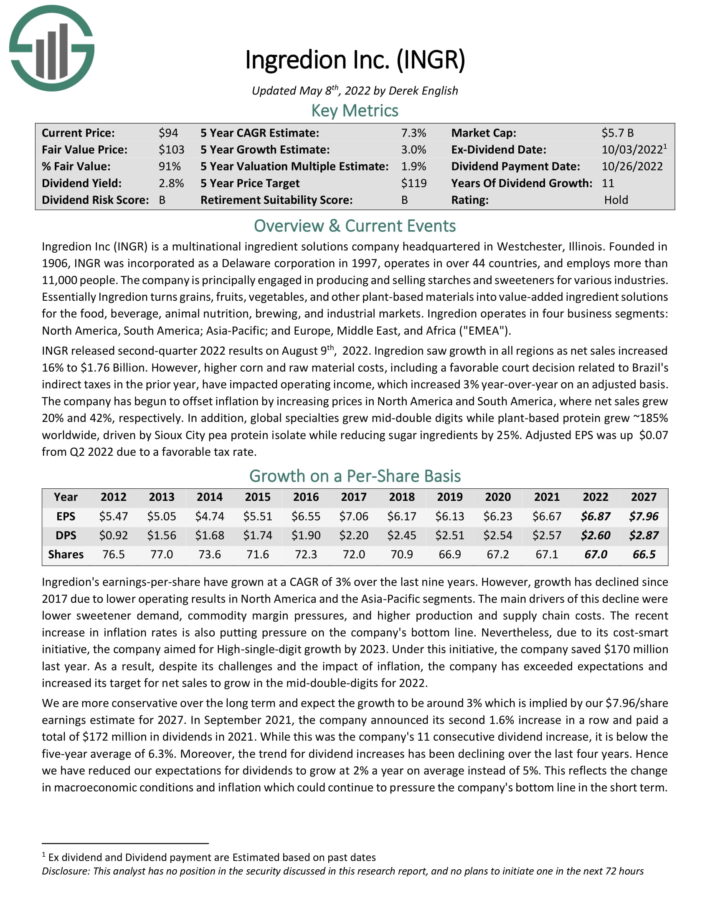

Agriculture Stock #5: Ingredion Inc. (INGR)

- 5-year expected annual returns: 9.9%

Ingredion is a multinational ingredient solutions company. It operates in over 44 countries, and employs more than 11,000 people. The company is principally engaged in producing and selling starches and sweeteners for various industries.

Essentially, Ingredion turns grains, fruits, vegetables, and other plant-based materials into value-added ingredient solutions for the food, beverage, animal nutrition, brewing, and industrial markets. Ingredion operates in four business segments: North America, South America; Asia-Pacific; and Europe, Middle East, and Africa (“EMEA”).

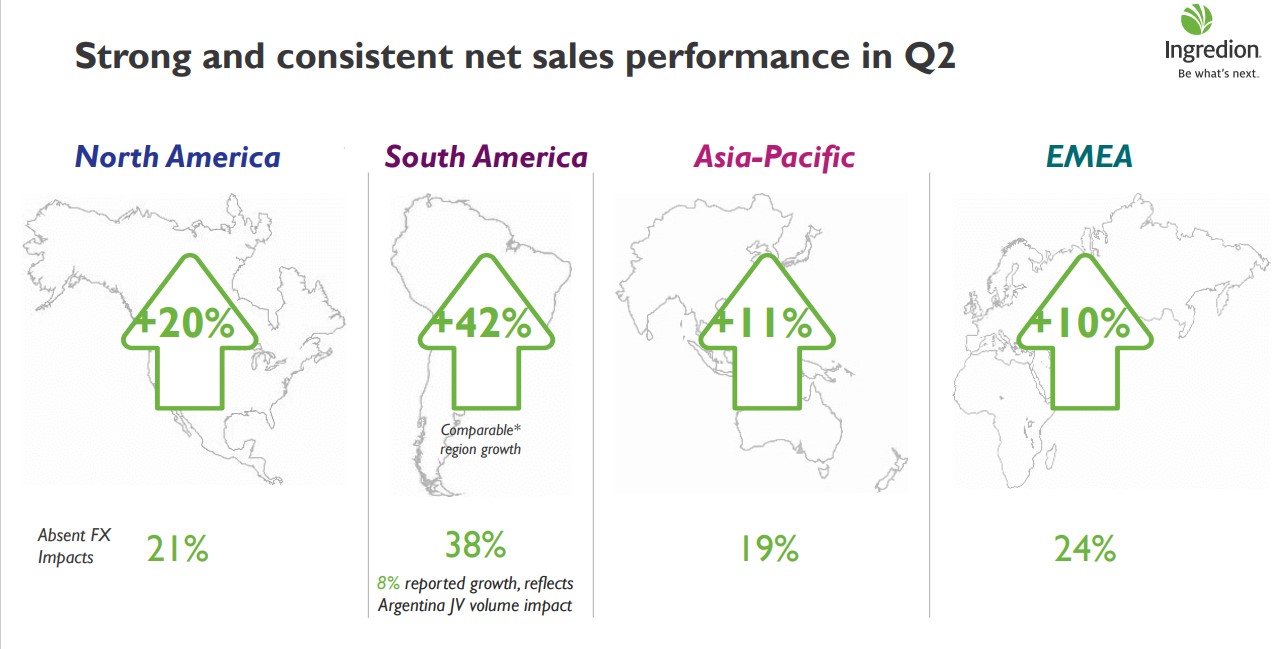

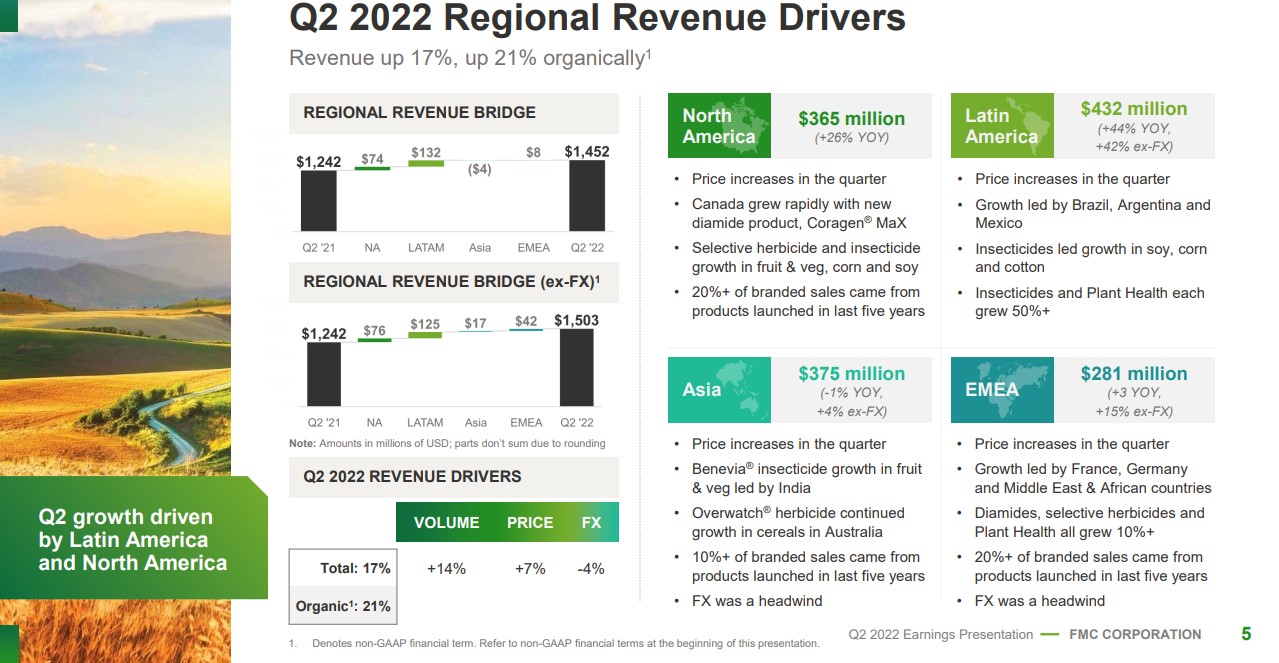

INGR released second-quarter 2022 results on August 9th, 2022. Ingredion saw growth in all regions as net sales increased 16% to $1.76 billion.

Source: Investor Presentation

However, higher corn and raw material costs, including a favorable court decision related to Brazil’s indirect taxes in the prior year, have impacted operating income, which increased 3% year-over-year on an adjusted basis.

The company has begun to offset inflation by increasing prices in North America and South America, where net sales grew 20% and 42%, respectively. In addition, global specialties grew mid-double digits while plant-based protein grew ~185% worldwide, driven by Sioux City pea protein isolate while reducing sugar ingredients by 25%. Adjusted EPS was up $0.07 from Q2 2022 due to a favorable tax rate.

We expect annual returns of 9.9% per year, due to 3% expected EPS growth, the 3.4% dividend yield, and a 3.5% annual return from an expanding P/E multiple.

Click here to download our most recent Sure Analysis report on INGR (preview of page 1 of 3 shown below):

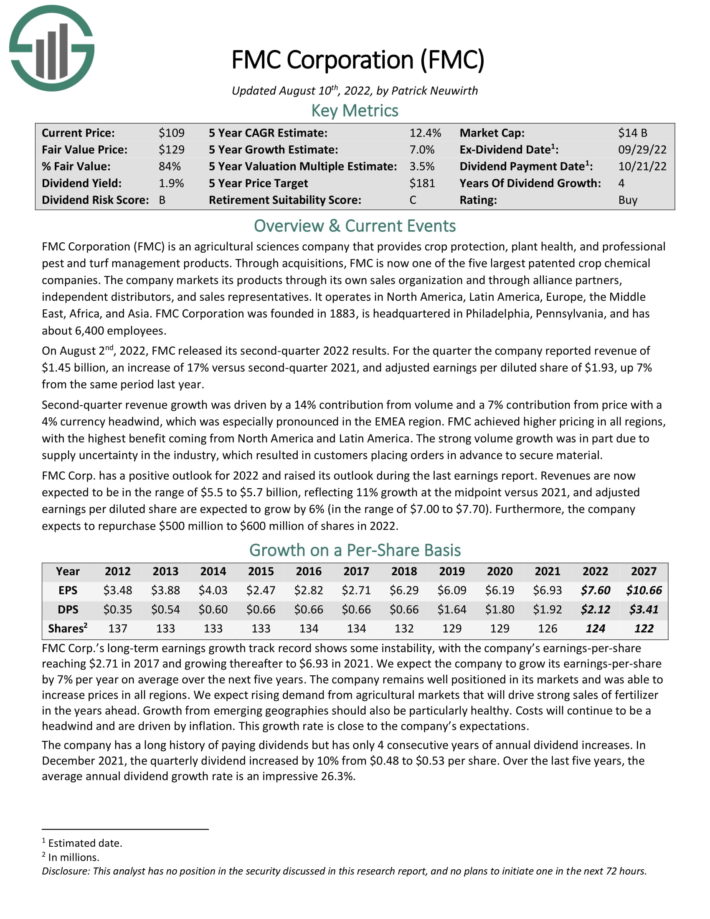

Agriculture Stock #4: FMC Corporation (FMC)

- 5-year expected annual returns: 10.9%

FMC Corporation is an agricultural sciences company that provides crop protection, plant health, and professional pest and turf management products. Through acquisitions, FMC is now one of the five largest patented crop chemical companies.

The company markets its products through its own sales organization and through alliance partners, independent distributors, and sales representatives. It operates in North America, Latin America, Europe, the Middle East, Africa, and Asia.

On August 2nd, 2022, FMC released its second-quarter 2022 results. For the quarter the company reported revenue of $1.45 billion, an increase of 17% versus second-quarter 2021, and adjusted earnings per diluted share of $1.93, up 7% from the same period last year.

Source: Investor Presentation

Second-quarter revenue growth was driven by a 14% contribution from volume and a 7% contribution from price with a 4% currency headwind, which was especially pronounced in the EMEA region. FMC achieved higher pricing in all regions, with the highest benefit coming from North America and Latin America. The strong volume growth was in part due to supply uncertainty in the industry, which resulted in customers placing orders in advance to secure material.

FMC Corp. has a positive outlook for 2022 and raised its outlook during the last earnings report. Revenues are now expected to be in the range of $5.5 to $5.7 billion, reflecting 11% growth at the midpoint versus 2021, and adjusted earnings per diluted share are expected to grow by 6% (in the range of $7.00 to $7.70). Furthermore, the company expects to repurchase $500 million to $600 million of shares in 2022.

We expect annual returns of 10.9% per year, driven by 7% expected EPS growth and the 1.8% dividend yield, as well as a ~2.1% annual boost from an expanding P/E multiple.

Click here to download our most recent Sure Analysis report on FMC (preview of page 1 of 3 shown below):

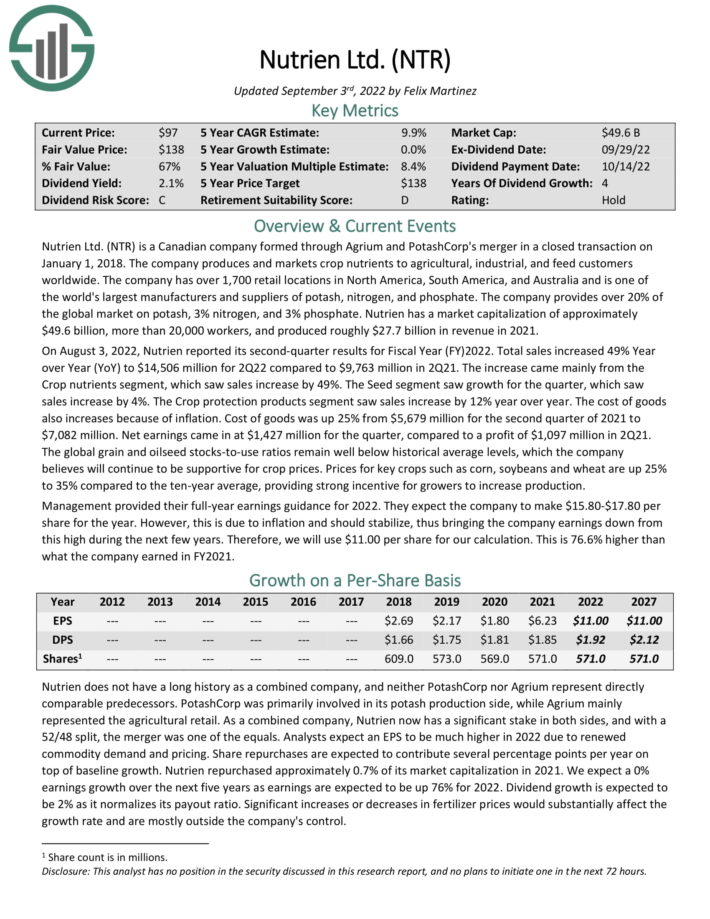

Agriculture Stock #3: Nutrien Ltd. (NTR)

- 5-year expected annual returns: 11.3%

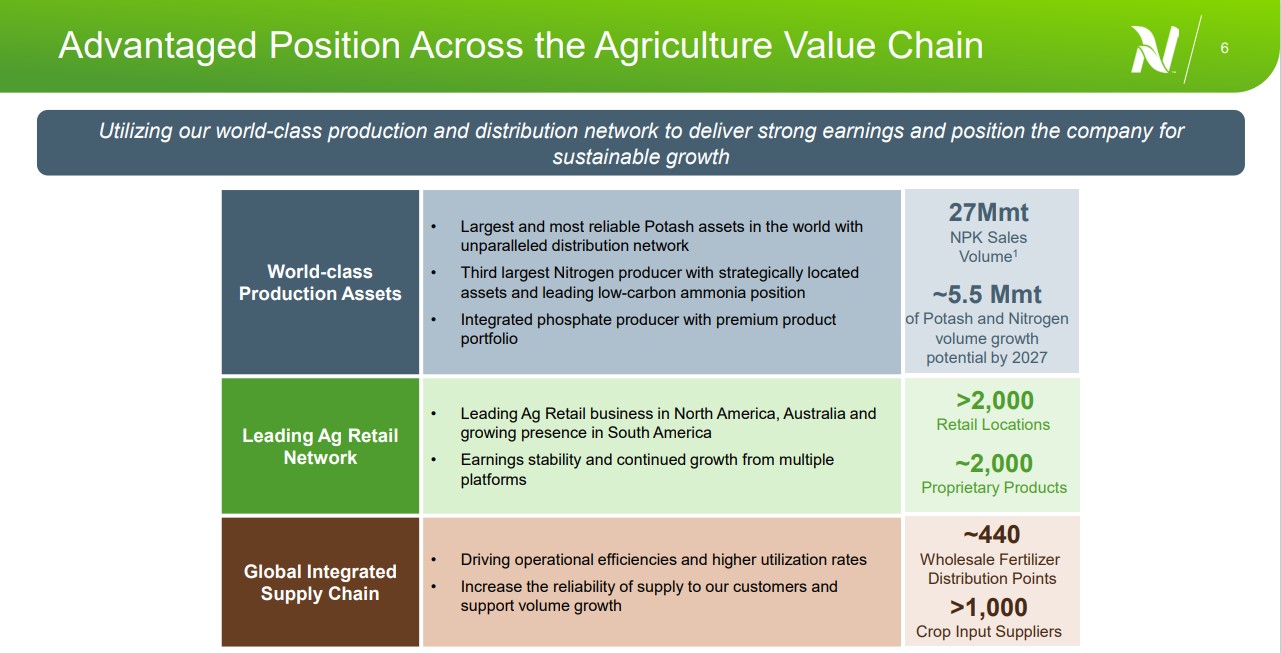

Nutrien Ltd. is a Canadian company formed through Agrium and PotashCorp’s merger in a closed transaction on January 1, 2018. The company produces and markets crop nutrients to agricultural, industrial, and feed customers worldwide.

The company has over 1,700 retail locations in North America, South America, and Australia and is one of the world’s largest manufacturers and suppliers of potash, nitrogen, and phosphate.

Source: Investor Presentation

The company provides over 20% of the global market on potash, 3% nitrogen, and 3% phosphate. Nutrien produced roughly $27.7 billion in revenue in 2021.

On August 3, 2022, Nutrien reported its second-quarter results for Fiscal Year (FY)2022. Total sales increased 49% year-over-year. The increase came mainly from the Crop nutrients segment, which saw sales increase by 49%. The Seed segment grew by 4%. The Crop protection products segment saw sales increase by 12% year over year. Net earnings came in at $1,427 million for the quarter, compared to a profit of $1,097 million in 2Q21.

The global grain and oilseed stocks-to-use ratios remain well below historical average levels, which the company believes will continue to be supportive for crop prices. Prices for key crops such as corn, soybeans and wheat are up 25% to 35% compared to the ten-year average, providing strong incentive for growers to increase production. Management expects the company to make $15.80-$17.80 per share for the year.

Total returns are estimated at 11.3% per year. While we expect no EPS growth, the 2.2% dividend yield and ~9.1% annual returns from an expanding P/E multiple will fuel future returns.

Click here to download our most recent Sure Analysis report on NTR (preview of page 1 of 3 shown below):

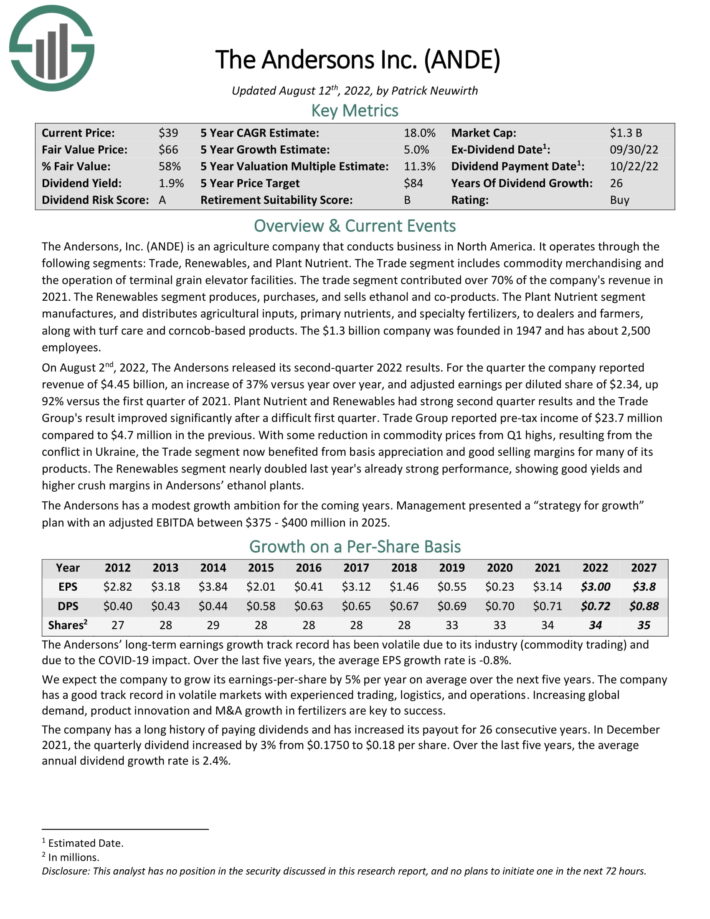

Agriculture Stock #2: The Andersons Inc. (ANDE)

- 5-year expected annual returns: 20.6%

The Andersons, Inc. operates through the following segments: Trade, Renewables, and Plant Nutrient. The Trade segment includes commodity merchandising and the operation of terminal grain elevator facilities. The trade segment contributed over 70% of the company’s revenue in 2021.

On August 2nd, 2022, The Andersons released its second-quarter 2022 results. For the quarter the company reported revenue of $4.45 billion, an increase of 37% versus year over year, and adjusted earnings per diluted share of $2.34, up 92% versus the first quarter of 2021. Plant Nutrient and Renewables had strong second quarter results and the Trade Group’s result improved significantly after a difficult first quarter. Trade Group reported pre-tax income of $23.7 million compared to $4.7 million in the previous.

With some reduction in commodity prices from Q1 highs, resulting from the conflict in Ukraine, the Trade segment now benefited from basis appreciation and good selling margins for many of its products. The Renewables segment nearly doubled last year’s already strong performance, showing good yields and higher crush margins in Andersons’ ethanol plants.

The Andersons has a modest growth ambition for the coming years. Management presented a “strategy for growth” plan with an adjusted EBITDA between $375 – $400 million in 2025.

The company has a long history of paying dividends and has increased its payout for 26 consecutive years. Shares currently yield 2.1%. We expect 5% annual EPS growth, while the stock also appears to be significantly undervalued. Total returns are estimated at 20.6% per year.

Click here to download our most recent Sure Analysis report on ANDE (preview of page 1 of 3 shown below):

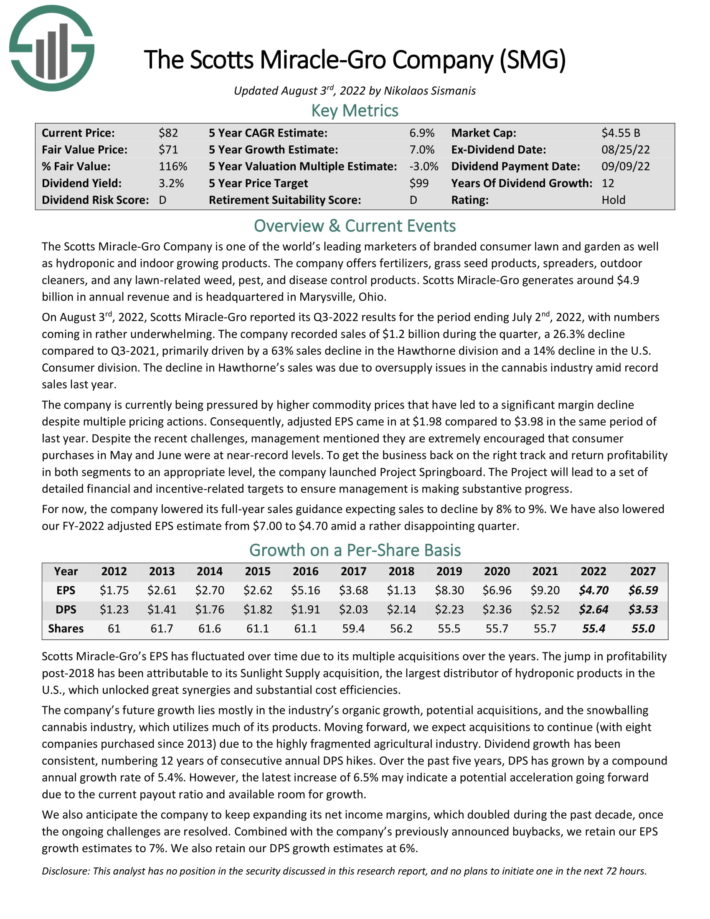

Agriculture Stock #1: Scotts Miracle-Gro (SMG)

- 5-year expected annual returns: 22.2%

The Scotts Miracle-Gro Company is one of the world’s leading marketers of branded consumer lawn and garden as well as hydroponic and indoor growing products. The company offers fertilizers, grass seed products, spreaders, outdoor cleaners, and any lawn-related weed, pest, and disease control products.

Source: Investor Presentation

On August 3rd, 2022, Scotts Miracle-Gro reported its Q3-2022 results for the period ending July 2nd, 2022, with numbers coming in rather underwhelming. The company recorded sales of $1.2 billion during the quarter, a 26.3% decline compared to Q3-2021, primarily driven by a 63% sales decline in the Hawthorne division and a 14% decline in the U.S. Consumer division.

The decline in Hawthorne’s sales was due to oversupply issues in the cannabis industry amid record sales last year. The company is currently being pressured by higher commodity prices that have led to a significant margin decline despite multiple pricing actions. Consequently, adjusted EPS came in at $1.98 compared to $3.98 in the same period of last year.

Despite the recent challenges, management mentioned they are extremely encouraged that consumer purchases in May and June were at near-record levels. To get the business back on the right track and return profitability in both segments to an appropriate level, the company launched Project Springboard.

The Project will lead to a set of detailed financial and incentive-related targets to ensure management is making substantive progress. The company lowered its full-year sales guidance expecting sales to decline by 8% to 9%.

We expect annual returns of 22.2% per year, driven by expected EPS growth of 7%, the 6.2% dividend yield and a ~9% annual boost from an expanding P/E multiple.

Click here to download our most recent Sure Analysis report on Scotts Miracle-Gro (preview of page 1 of 3 shown below):

Final Thoughts

Agriculture stocks are a compelling place to look for long-term stock investments. That’s because the demand drivers of the industry make it extremely likely to be around far into the future.

We believe the 7 agriculture stocks examined in this article are the best within the industry.

Of these, FMC, Scotts Miracle-Gro, and The Andersons stand above the rest from a quality perspective thanks to their strong business models, attractive dividend yields, and long-term dividend growth potential.

At Sure Dividend, we often advocate for investing in companies with a high probability of increasing their dividends each and every year.

If that strategy appeals to you, it may be useful to browse through the following databases of dividend growth stocks:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].