DNY59

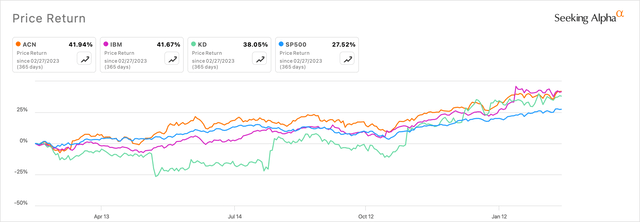

Accenture (NYSE:ACN) has seen modest development of their inventory’s efficiency, beating the broader market indices. Over the previous 12 months, the corporate’s market cap rose ~41%, increased than the S&P 500 at ~27% and beating a few of its friends akin to IBM (IBM) and Kyndryl (KD).

sa

Nonetheless the expertise consulting firm’s market efficiency is dwarfed by bigger expertise firms akin to Microsoft (MSFT) and Salesforce (CRM). Optimism within the firm’s outlook seems to have waned because the firm is seeing its development charges stall as companies cut back their discretionary spending whereas allocating their budgets in direction of bigger development areas akin to GenAI.

Accenture has made it mission-critical to additionally pivot on this space. Over the previous couple years, the corporate has taken benefit of its robust money place to accumulate firms. I imagine these acquisitions place Accenture in direction of a path of worthwhile development once more, and I see room for the inventory to run given these initiatives turning me bullish on the inventory.

About Accenture

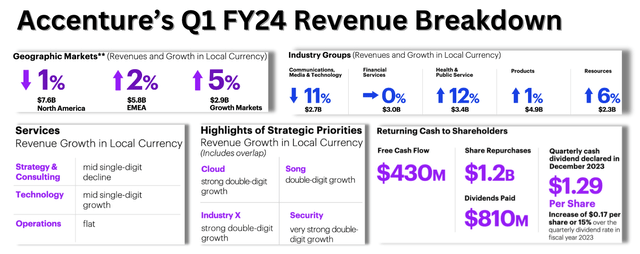

Accenture is knowledgeable and managed providers firm with the goal of offering consulting providers to purchasers and enterprises, serving to them digitize their companies and optimize their operations. This international consulting heavyweight presents consulting providers in addition to managed providers or outsourcing providers. As of its FY23 10K report, barely over 50% of its revenues come from Consulting, whereas the remainder come from its Managed Companies enterprise. I’ve compiled a snapshot beneath from its Q1 FY24 presentation.

Creator’s compilation from Accenture’s FY24 Q1 quarterly presentation

The corporate additionally has a historical past of working with firms throughout trade varieties. Shopper product purchasers account for round 30% of Accenture’s income share. Shoppers within the Monetary Companies, Healthcare, and Communications & Media domains every account for 18%–20% of Accenture’s revenues. Round 47% of its purchasers are North American firms, with 33% being in Europe and the remainder in rising market areas.

For the reason that firm operates inside the enterprise consulting and managed providers domains, it sometimes enters into multi-year contracts with its purchasers and information the quantity of those contracts as Bookings. I view Accenture’s new bookings metric as an approximate ahead indicator that alerts the expansion of its enterprise, since extra bookings imply extra contracts signed, with the potential for extra revenues per contract signed.

Acquisitions might reverse the slowing tendencies in Accenture’s enterprise.

Typically, the consulting house has been hit by slowdowns in venture budgets. These tendencies had been particularly seen in Accenture’s outcomes, which had been extra pronounced in a few of their stronger income segments, which I’ll focus on later. However the important thing takeaway from Accenture’s Q1 FY24 earnings name final month was that companies are persevering with to lower their discretionary budgets for initiatives, as famous by Accenture’s administration on the decision.

As anticipated, we proceed to see decrease discretionary spend, which notably impacts our consulting sort of labor in addition to slower resolution making and our CMT (Communications, Media, & Expertise) trade group continues to be challenged. We stay on monitor with the enterprise optimization actions we introduced in March to scale back structural prices to create higher resilience.

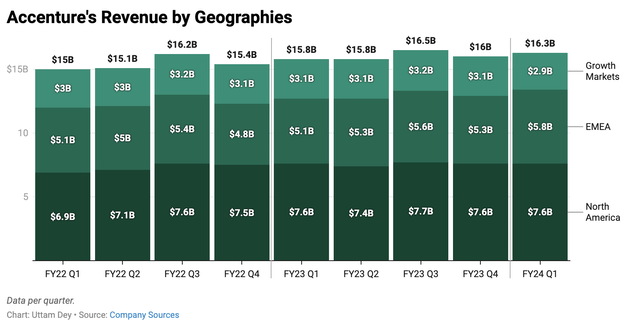

As may be seen within the chart beneath, income development charges have been stalling since mid-2022.

Accenture’s income by Geographies, Creator’s compilation from firm sources

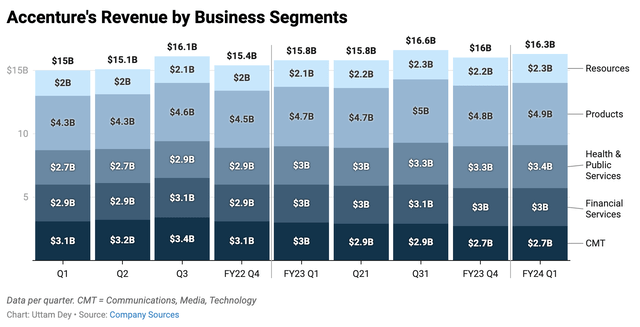

A lot of the slowdown was attributed to their enterprise in North America, which, as I famous earlier, often accounts for 47% of their income. By way of income segments, the slowdowns have been extra pronounced inside their purchasers which might be a part of the Merchandise enterprise group and the CMT group, as these companies had been notably hit laborious by the speedy rise in rates of interest. This was additionally identified by Accenture’s administration within the commentary I connected earlier. Within the chart beneath, I see how quarterly y/y tendencies in income inside enterprise segments and geographical segments present slowdowns.

Accenture’s income by Income Segments, Creator’s compilation from firm sources

Nevertheless, within the Q1 FY24 quarter, Accenture issued some upbeat numbers of their bookings, which can level to a trough of their earnings transferring ahead. Within the Q1 quarter, Accenture famous that its bookings had been up 14% y/y to $18.4 billion. Accenture famous that its consulting initiatives associated to digital transformations, akin to Cloud and Safety noticed robust double-digit development. Furthermore, Accenture has been very busy previously couple of years, buying near 14 firms since 2022. 4 of these acquisitions have been made within the final two months alone, and a lot of the latest acquisitions are tied to AI. On the Q1 name, administration famous that it had accomplished $450 million of gross sales in Q1 alone as a consequence of GenAI initiatives, which simply overshadowed the $300 million it achieved as a consequence of gross sales from GenAI initiatives by way of FY23.

With respect to the acquisition technique, I’ve connected an excerpt from administration’s Q1 FY24 name that I believe would appropriately add coloration to Accenture’s acquisition-led technique. I’ve additionally bolded one sentence particularly within the commentary beneath, which reveals how administration attracts from its historical past of leaning on its funding capability.

We’re nonetheless investing to both scale in sizzling areas or add new varieties of abilities. You see that we’re executing in capital initiatives like we described. I’d reiterate that it’s actually an enormous aggressive benefit for us that we will make investments throughout the cycles. You noticed that we did that within the first 12 months after the pandemic, the place we considerably elevated, and once more, all the time to drive natural development and place ourselves for these subsequent waves. So, you are going to see the AI acquisitions. You noticed well being within the UK, one other nice space of development, capital initiatives. So, take into consideration our strengths right here is how we speed up pivoting to development.

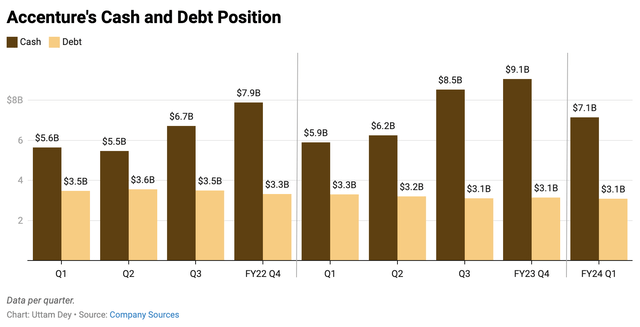

Though the corporate’s money ranges have declined, the corporate nonetheless seems wholesome and is ready to service its internet debt place. I think administration is utilizing the corporate’s robust money place to speculate it in rising areas of development and fund its subsequent chapter utilizing acquisitions that I discussed within the earlier paragraph.

Accenture’s money and debt positions, Creator’s compilation from firm sources

Moreover, administration additionally revealed within the Q1 FY24 name that they’re sticking to their long-term goal of returning money to shareholders, having executed 22% of their share buyback program within the final quarter and repurchased $1.2 billion value of shares at a median worth of $311.90 per share. Observing how administration is diligently managing the corporate’s debt ranges within the chart above whereas investing its money for future development, I sense that administration noticed worth on the ~$315 worth vary and acquired again shares. By doing so, I see that Accenture’s is constantly managing the dilution in its shares, as its excellent share quantity has fallen by slightly below a p.c on a compounded foundation over a five-year trailing interval.

Outlook for Accenture

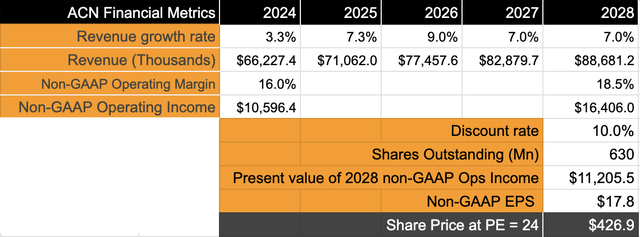

Accenture has demonstrated its acuity in transferring swiftly to realize market share within the consulting and managed providers house for GenAI. The acquisitions that I mirrored upon earlier manifest Accenture’s ambitions to learn from GenAI. I imagine these acquisitions previously few years will pivot the skilled providers firm in direction of increased mid-digit development any further, as the corporate has already seen a few of that profit in the previous few quarters. On the similar time, administration has additionally prioritized delivering reasonable margin enlargement per their Investor Day presentation. Taking these assumptions under consideration, I count on their adjusted working revenue to develop at ~12% CAGR, outpacing its ~7.5% compounded development over a five-year interval.

Creator

At this tempo of compounded development, I believe a ahead PE of 24 is justified, which suggests the inventory is at present undervalued with at the least 12% upside.

Dangers & Different Components to think about

If the enterprise spending slowdown continues as the corporate had beforehand seen in the previous few quarters, the outlook of Accenture will deteriorate, forcing me to rethink the optimistic outlook that I at present have for the corporate. As talked about earlier, I had famous how Accenture administration nonetheless sees enterprise discretionary spending decelerating, however they count on spend cycles to reverse increased, and the momentum in its GenAI bookings is anticipated to assist increased income development, in my view.

The greenback additionally performs an essential function in impacting Accenture’s development. With the surge within the U.S. greenback in FY22, Accenture was impacted as companies pushed out their initiatives as a consequence of increased change charges and rates of interest. Thus far, Accenture continues to see no impression from the greenback if it stays flat on a y/y foundation. However had been the greenback to maneuver increased once more, it could add headwinds to Accenture’s income development charges.

Takeaways

I imagine Accenture is setting itself as much as be a secular beneficiary of the shift in direction of GenAI by consolidating its place in Consulting and Managed providers. Administration has reinvested money in direction of buying firms that may assist it re-accelerate its development trajectory whereas prioritizing margin enlargement on the similar time, aiding the long-term bullish view I maintain for Accenture. I fee Accenture as a Purchase.

{kind=link}