Urupong/iStock by way of Getty Photographs

Absolute Software program Company (NASDAQ:ABST) competes in a fast-growing cybersecurity sector that’s going to proceed to develop for a few years. It had some first rate numbers in its newest earnings report, however there have been some cracks within the armor beginning to seem, which in the event that they widen, might develop into problematic all through 2023.

Among the many considerations are some modifications in size of contracts, conversion of perpetual licenses to time period, and a rise in non-renewals of end-of-life product.

At the moment, these headwinds are modest in nature. They may simply speed up in 2023, which might push the expansion trajectory of ABST down.

Whereas the corporate has supplied steering for fiscal 2023, I am involved there due to the dearth of visibility on the macroeconomic aspect of issues. Regardless that the corporate does have contracted ARR, there are a variety of headwinds that would shortly change the expansion trajectory there, together with prime administration delaying and/or reprioritizing spend.

On this article we’ll have a look at among the latest numbers, some headwinds the corporate faces, and why I believe it is untimely to supply steering within the present financial setting.

Among the numbers

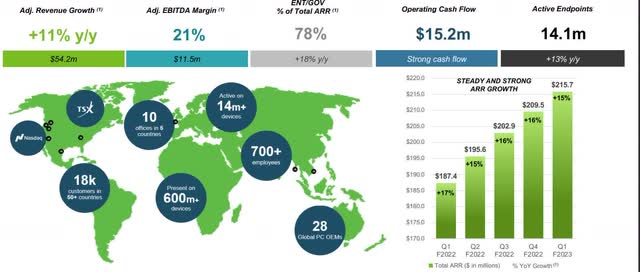

Adjusted income within the first fiscal quarter of 2023 was $54.2 million, up 10.6 p.c year-over-year.

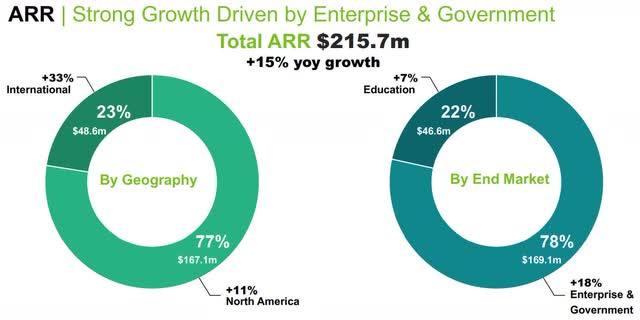

Whole ARR within the reporting interval was $215.7 million, up 15 p.c from the primary fiscal 12 months of 2022.

ARR in Enterprise & Authorities income of $169.1 million accounted for 78 p.c of whole ARR and was up 18 p.c in comparison with the primary fiscal quarter of 2022. Training ARR income of $46.6 million was 22 p.c of whole AAR and was up 7 p.c year-over-year.

Investor Presentation

Adjusted EBITDA was $11.5 million, in comparison with $12.8 million in adjusted EBITDA in the identical reporting interval final 12 months. Adjusted EBITDA margin was 21 p.c, down 5.1 p.c from the 26.1 p.c margin within the first fiscal quarter of 2022.

Adjusted gross margin within the quarter was 88 p.c. With the corporate’s ongoing transition to the general public cloud, it’s leading to larger prices which the corporate believes over time will decrease adjusted gross margin by 100 foundation factors to 200 foundation factors.

Working money move within the fiscal first quarter of 2023 was $15.2 million.

Money and short-term investments elevated from $67.6 million from $64 million within the prior quarter after servicing its debt and paying out its dividend. After its coupon elevated by 125 p.c sequentially, the corporate needed to pay out roughly $900,000 extra in curiosity bills within the reporting interval.

Regardless that there have been some financial headwinds that had an impression on the efficiency of the corporate within the reporting interval, particularly in schooling, the corporate sees development within the enterprise house and rising exercise in its Safe Entry product line offsetting that and conserving its adjusted income and adjusted EBITDA steering for full fiscal 2023 in place.

Whereas it is doable it’s going to have the ability to offset the headwinds, I am not satisfied within the present financial local weather that there is sufficient visibility over the subsequent a number of quarters to confidently present that king of steering, even with Training accounting for less than 22 p.c of whole ARR. Not solely that, however in Enterprise & Authorities there are numerous issues that would downwardly regulate, equivalent to contract size and slowing within the conversion of perpetual licenses, that are already occurring.

Investor Presentation

Headwinds

In all probability the headwind that had essentially the most fast impression on the efficiency of ABST was in Training, the place provide chain points resulted in both numerous offers being pushed out or faculty districts altering from PCs to Chromebooks.

As for the offers being pushed out, administration says it expects to signal a few of these within the second fiscal quarter. Regarding Chromebooks, the combo has a a lot larger proportion of Chromebooks now due to their availability to high school districts.

The issue for ABST is Chromebooks has a decrease ARR per endpoint and represents a headwind for the corporate. Whereas administration sees endpoint inhabitants in Training to proceed to develop, it expects it to contribute to ARR development at a slower tempo.

As talked about above, Training income was up 7 p.c year-over-year, and as a proportion of whole income it’s declining. I believe that is going to proceed on sooner or later, and the impression on the efficiency of the corporate might be decided by whether or not or not the headwinds in Training from provide chain points are the catalyst, or development in Enterprises & Authorities is. If it is the previous, it might be a drag on Absolute Software program Company within the first half of calendar 2023.

Even with the headwinds, the corporate sees Training rising at a high-single-digit, low-double-digit tempo. If provide chain points proceed to have an effect on Training, I believe these numbers, at finest, are going to return in on the low aspect of expectations, and more than likely, decrease.

Among the areas macroeconomic elements got here into play within the quarter was in regard to size of contracts and conversion of perpetual licenses to time period. At the moment contract size did not have a unfavorable impact on ARR, however it did have a small unfavorable impression on income. If the financial system will get worse in calendar 2023, that is in all probability going to lead to a rise in shorter contracts in addition to conversion of perpetual licenses, which mixed, ought to have an effect on income and presumably to a modest diploma, on ARR.

For now, the visibility is not there to know which means it’s going to go, however the financial system and ongoing provide chain constraints are undoubtedly headwinds buyers want to look at regarding the impression on the efficiency of Absolute Software program going ahead. The query that has but to be answered is whether or not or not anticipated development within the enterprise house and growing exercise in its Safe Entry product line might be sufficient to offset the headwinds in Training, particularly if projected development in Enterprise and Safe Entry is decrease than anticipated based mostly upon unexpected responses to a weakening international financial system, if that is the way it performs out in 2023.

We might already be seeing a few of that coming from its Enterprise enterprise, which whereas enhancing sequentially, began to see some drag from non-renewal from legacy clients on the end-of-life product.

What’s occurring in these conditions is many administration groups are taking tighter management of spending on the prime, and the standard result’s spending contraction at some stage, which within the case of ABST might transition into a major headwind if non-renewals enhance.

Conclusion

Absolute Software program Company has had some constant development during the last 12 months, rising ARR from $187.4 million within the fiscal first quarter of 2021 to $215.7 million within the first fiscal 12 months 0f 2023, however it seems to be like macroeconomic weak point is beginning to affect the corporate.

And although the corporate provided steering, it considerations me that it did so in gentle of the dearth of visibility regarding the international financial system over the subsequent 12 months or so. Except for a only a few firms, administration groups have said they weren’t going to offer steering for 2023 due to the dearth of readability on how issues are going to play out over the subsequent 12 months. I believe that is the right method to view it.

As talked about above, there are already a number of issues rising available in the market which are having a slight impression on the corporate, equivalent to provide chain points, size of contracts, conversion of perpetual licenses to time period, and non-renewals of end-of-life product.

These aren’t issues that must be brushed apart just because they are not having a powerful impression on the efficiency of ABST now, other than provide chain. With all of these items occurring on the identical time, it suggests it might be within the early phases of a weaker market. In that case, these items are going to point out indicators of accelerating in impression on the corporate, and that may convey a couple of weaker efficiency in 2023.

Buying and selling View

Absolute Software program Company is buying and selling near the place it was in early June 2020, and I believe that displays uncertainty from the market within the sustainability of its long-term development trajectory. As the corporate stands at present and the unpredictability of the worldwide financial system in calendar 2023, I believe it should battle to achieve traction within the close to time period, by which I imply over the subsequent six months to a 12 months.

Over the long run, with Absolute Software program Company competing in a sector that’s in a development development that ought to final for a few years, the prospects for the corporate look good. Nevertheless, Absolute Software program Company goes to must work via this present interval of volatility and have a greater financial local weather to function in earlier than it has an opportunity to attain its potential.

{kind=link}