")

[ad_1]

SerrNovik

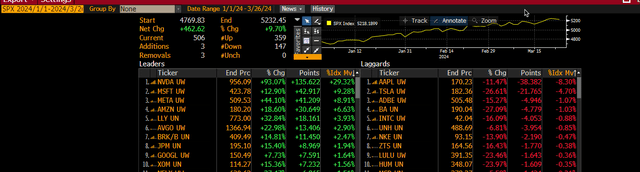

Market rotation appears lifeless as of late, with simply three shares accounting for about 50% of the beneficial properties within the S&P 500 and 5 shares accounting for nearly 60%. That signifies that of the 462.62 factors the S&P 500 (SPX) has gained in 2024, 268 factors of these beneficial properties have come from Nvidia (NVDA), Microsoft (MSFT), Meta (META), Amazon (AMZN), and Eli Lilly (LLY).

The highest-10 gainers account for 317 factors within the S&P 500, about 69% of all of the beneficial properties up to now in 2024. Apple (AAPL) has weighed down the S&P 500, accounting for 8.3% of its losses, whereas Tesla has accounted for 4.7%. In whole, the top-10 decliners in 2024 have subtracted a complete of simply 85 factors from the S&P 500 and characterize a mere fraction of what the top-5 shares have overwhelmingly contributed. Nvidia alone has added 135.6 factors to the S&P 500 this yr.

Bloomberg

Certainly, this isn’t an indication of a market rotation or a rally broadening out; it’s extra an indication of market focus. What’s extra troubling concerning the rally is that almost all of the names main the cost are linked to the AI mania that has been happening in 2024, which isn’t wholesome. If the AI mania ought to fade or implode on itself, which is feasible given the exuberance within the group, greater than 50% of the S&P 500 beneficial properties could be gone.

What this tells us is that the market rally just isn’t as safe as some would possibly make you suppose and should not even be all that deserved since most of it has come on the heels of a number of expansions, not as a result of the earnings outlook is enhancing.

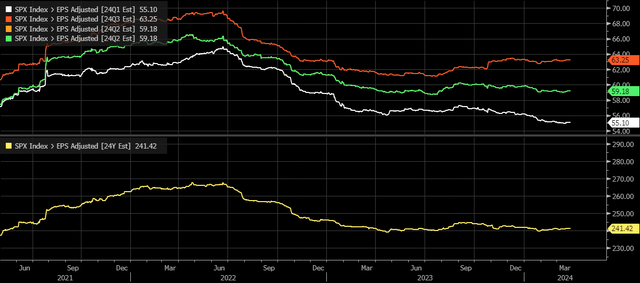

In actual fact, earnings estimates for the S&P 500 have been steadily declining for the primary quarter, whereas the precise earnings estimates for 2024 have been as flat as a thinly cooked pancake since February 2023 and are simply trending sideways.

Bloomberg

So, whereas earnings are anticipated to develop by roughly 9 to 10% in 2024, there was no enchancment to that development outlook over the previous yr. In actual fact, most of that development is not as a result of earnings for 2024 have improved; it’s as a result of earnings estimates for 2023 deteriorated materially beginning within the fall of 2022. Earnings estimates for 2024 are actually round $241 per share, in comparison with round $241 per share again within the fall of 2022. It sounds a bit like development by way of subtraction.

Bloomberg

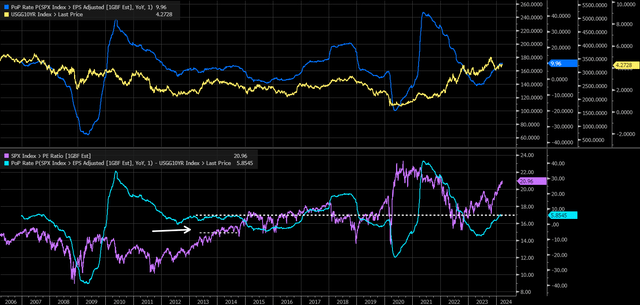

If you consider that development price a bit additional and take the anticipated development price over the following 12 months of 9.96%, the anticipated market return, and subtract the 10-year Treasury price of 4.27%, the premium for earnings development over the risk-free price is simply 5.85%, which is just about what the chance premium was in 2012, 2013, and 2014. The S&P 500 had a PE a number of of nearer to 16 than at present’s 21, which is a distinction of about 24%.

Bloomberg

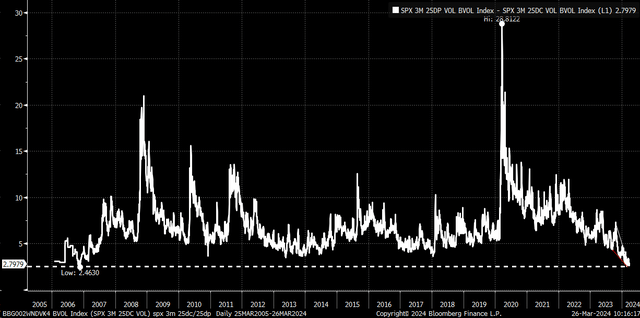

Issues like PE multiples are very emotionally pushed, although, and the present PE a number of, given the risk-free price, appears to recommend plenty of complacency and enthusiasm constructed up on this market. It’s not laborious to seek out that complacency or exuberance when utilizing a 3-month S&P 500 25 delta put implied volatility versus a 3-month S&P 500 25 delta name unfold, which is at present simply 2.8 proportion factors. The bottom worth going again to late 2006.

Bloomberg

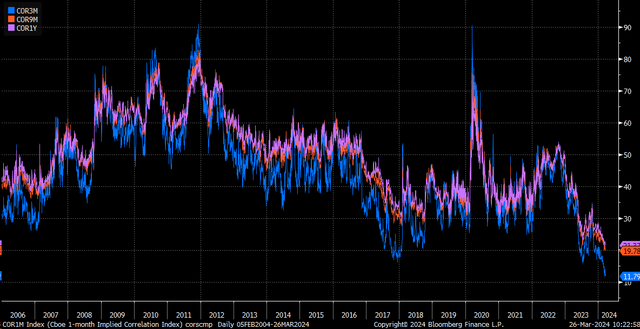

In the meantime, the 3-month implied correlation index measures the anticipated correlation of the highest 50 opponents inside the S&P 500 utilizing their implied volatility ranges. A low worth on this index means that shares will not be correlated. The present studying is at an all-time low, together with the 9-month and 12-month implied correlation indexes.

Bloomberg

This means that the market rally just isn’t as broad because it appears on the floor; the info reveals that almost all the beneficial properties are coming from only a handful of names, whereas the shares which might be declining have hardly made a dent.

If one scans the adjustments within the sector ETFs, it could seem that some sort of broader-based rotation is happening, however the information beneath the floor factors to skinny management. On prime of that, the earnings outlook has remained unchanged for practically a yr, with development coming from a weaker-than-expected 2023, not an enhancing 2024. Moreover, the S&P 500 is dear, contemplating one is paying a particularly excessive a number of for a fairly meager return versus the risk-free price.

Perhaps ignorance is bliss, or not seeing or understanding all the information makes one really feel heat and fuzzy, however most proof helps the alternative. This can be a time to be extraordinarily cautious with how one operates on this market and, extra importantly, extraordinarily conscious of the dangers.

[ad_2]

Source link