Robinhood Banking is Robinhood’s largest push but past inventory buying and selling — a full checking-and-savings expertise that pays as much as 4% APY, delivers bodily money to your door, and wraps your deposits in as much as $2.5 million of FDIC protection. Introduced in early 2025 and rolling out by way of 2026, it’s designed to make your on a regular basis money work as laborious as your investments.

However there’s a catch that journeys up lots of people: Robinhood isn’t a financial institution, and Robinhood Banking is simply out there to paying Robinhood Gold members. The accounts are held at an FDIC-insured companion financial institution, one of the best perks require a month-to-month direct deposit, and entry continues to be rolling out by invitation. Whether or not it’s value switching relies on how a lot money you retain available and the way deep you already are within the Robinhood ecosystem.

On this information we’ll break down the whole lot: the actual APY, how the checking and financial savings accounts work, the headline-grabbing cash-delivery characteristic, the charges, who really qualifies, and — most significantly — whether or not Robinhood Banking is secure. Robinhood unveiled the product alongside its wealth-management and AI instruments in its official 2025 announcement, positioning it as a direct problem to conventional banks.

| Robinhood Banking — At a Look | Particulars |

|---|---|

| Account Varieties | Checking & high-yield financial savings (particular person, joint & youngsters’ accounts) |

| Financial savings APY | As much as 4.00% for Gold members (no cap, no minimal) |

| Month-to-month Price | $0 account charge — however requires Robinhood Gold ($5/mo or $50/yr) |

| FDIC Protection | As much as $2.5 million by way of partner-bank sweep community |

| Banking Companion | Coastal Neighborhood Financial institution, Member FDIC |

| Standout Function | On-demand money supply to your door (charge & space limits apply) |

| Availability | Robinhood Gold members solely — rolling out by invite |

What Is Robinhood Banking?

Robinhood Banking is a set of full-featured deposit accounts — a checking account and a high-yield financial savings account — constructed immediately into the Robinhood app. It’s supplied by way of Robinhood Cash, LLC, with the precise banking providers and FDIC insurance coverage offered by Coastal Neighborhood Financial institution, Member FDIC. In different phrases, Robinhood is the tech and interface; a chartered financial institution holds your cash.

Robinhood first revealed Robinhood Banking in early 2025 at its “Misplaced Metropolis of Gold” occasion, alongside a wealth-management service (Robinhood Methods) and an AI finance assistant (Robinhood Cortex). The banking product started rolling out to Gold members by way of late 2025 and into 2026. It’s aimed squarely on the “major checking account” relationship that conventional banks like Chase and Financial institution of America have lengthy owned — and it’s utilizing a excessive APY, beneficiant FDIC protection, and a few genuinely novel perks to pry prospects away.

In contrast to the older Excessive-Yield Money sweep program (which pays curiosity on uninvested brokerage money), Robinhood Banking is a standalone banking relationship with a debit card, routing and account numbers, direct deposit, joint accounts, and even accounts for teenagers. For those who’re new to the platform, our full Robinhood evaluation covers how the brokerage aspect works.

Robinhood Banking APY: How A lot You’ll Earn

The headline quantity is the APY, and it’s aggressive. Robinhood Banking financial savings pays as much as 4.00% APY for Gold members — a number of occasions the nationwide financial savings common of roughly 0.38%. There’s no cap and no minimal stability to earn the speed, which is uncommon; many “high-yield” accounts throttle the highest price above a sure stability.

A couple of essential nuances on the speed:

- The speed is variable. Like each high-yield account, the APY floats with the broader interest-rate setting and might change at any time.

- Gold membership is required to earn the highest price. Drop Gold and the speed drops too.

- Promotional boosts seem periodically. Robinhood has run limited-time APY-boost gives for brand spanking new financial savings accounts, which may carry the first-year composite yield even increased.

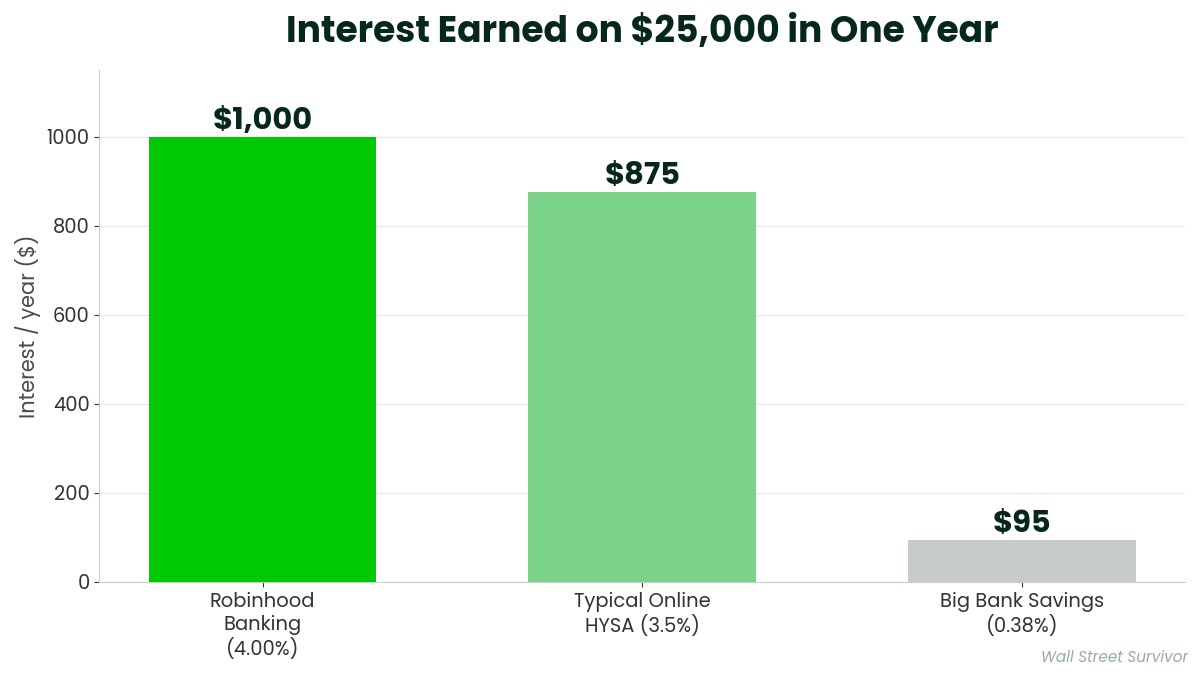

To place the speed in perspective, right here’s what $25,000 in financial savings earns in a 12 months at a number of frequent APYs:

| Account | APY | Curiosity on $25,000/yr |

|---|---|---|

| Robinhood Banking (Gold) | 4.00% | ~$1,000 |

| Typical on-line HYSA | ~3.5% | ~$875 |

| Large-bank financial savings (nationwide avg.) | 0.38% | ~$95 |

Even after subtracting the $50/12 months Gold membership, a saver with a wholesome stability comes out effectively forward of a standard big-bank account. The mathematics solely breaks down should you hold little or no money available — through which case the Gold charge eats up many of the curiosity benefit.

Robinhood Banking Options & Perks

Past the APY, Robinhood Banking is loaded with options you don’t usually see bundled collectively — some sensible, some virtually theatrical.

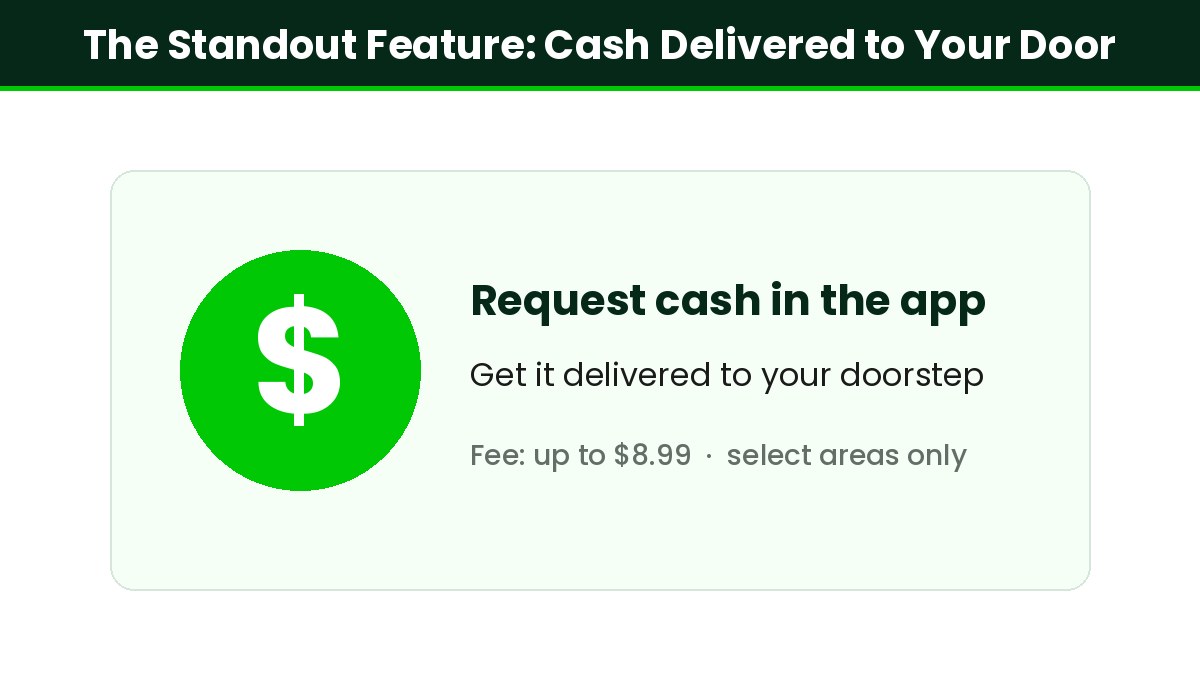

1. Money Delivered to Your Door

Probably the most talked-about characteristic: on-demand bodily money supply. As a substitute of trying to find an ATM, you possibly can request money within the app and have it delivered to your door. Availability relies on your location, and the service carries a charge (as much as about $8.99 per supply). It’s a gimmick for some and a real comfort for others — nevertheless it’s precisely the sort of headline characteristic that will get folks speaking a few new financial institution.

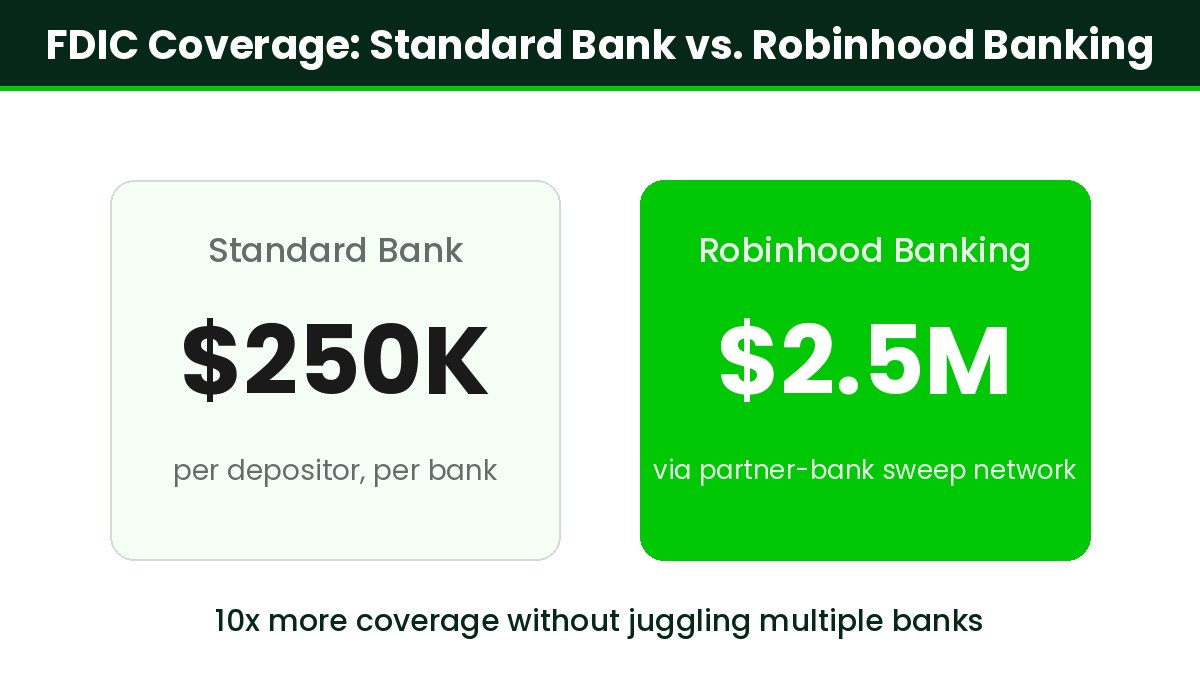

2. As much as $2.5 Million in FDIC Protection

Normal FDIC insurance coverage covers $250,000 per depositor, per financial institution. Robinhood Banking makes use of a sweep community of companion banks to unfold your deposits throughout a number of establishments, extending protection as much as $2.5 million. That’s a critical promoting level for anybody holding giant money balances who would in any other case need to open accounts at ten totally different banks to remain insured.

3. Checking, Joint & Children’ Accounts

Robinhood Banking helps particular person, joint, and youngsters’s accounts, plus a debit card, direct deposit, and commonplace bill-pay and switch features. The flexibility to open household and children’ accounts strikes Robinhood from a solo-investor app towards a family banking hub.

4. Non-public Banking & Luxurious Perks

For higher-balance prospects, Robinhood has teased a personal banking tier with property planning, tax recommendation, and eyebrow-raising luxurious perks — assume entry to personal jet journey, world chauffeurs, and helicopter rides. These are aimed on the wealth-management finish of the market and gained’t apply to most customers, however they sign Robinhood’s ambition to compete with personal banks, not simply on-line financial savings apps.

5. Bonus Perks for Gold Members

As a result of Robinhood Banking is bundled into Gold, members additionally get the broader Gold profit stack: a lift on IRA contributions, increased curiosity on brokerage money, and entry to the Robinhood Gold Card with 3% money again. The banking accounts are actually one piece of a bigger membership.

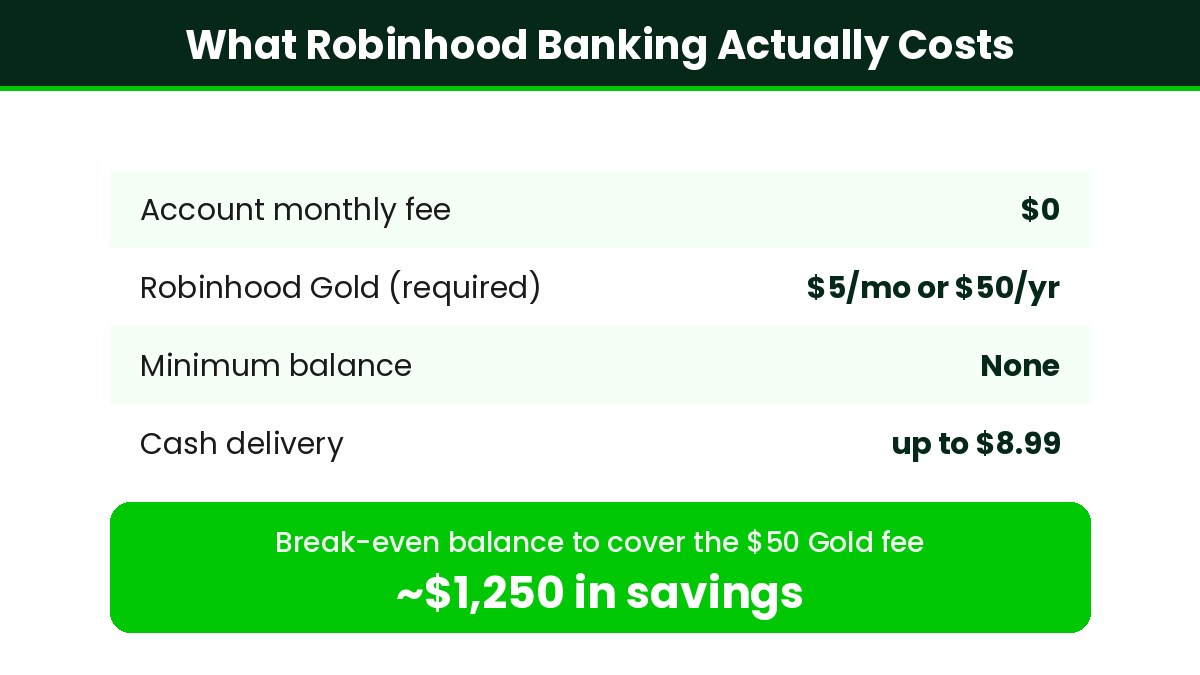

Robinhood Banking Value: What You’ll Truly Pay

The accounts themselves have no month-to-month upkeep charge, however you possibly can’t get Robinhood Banking with no Robinhood Gold subscription. Right here’s the actual value breakdown:

| Value Element | Quantity |

|---|---|

| Account month-to-month charge | $0 |

| Robinhood Gold (required) | $5/month or $50/12 months |

| Minimal stability | None |

| Money supply | As much as ~$8.99 per supply |

| Efficient annual value | $50–$60 (Gold) |

At 4% APY, you solely have to hold about $1,250 in financial savings to earn again the $50 annual Gold charge ($50 ÷ 4% = $1,250). Above that, the membership pays for itself and the remainder is upside. For those who’d already pay for Gold for the brokerage perks or the Gold Card, the banking accounts are successfully free. Wish to see if Gold is smart total? Learn Is Robinhood Gold Price It?

Is Robinhood Banking Secure?

That is the query that stops most individuals, and the trustworthy reply is: your deposits are protected, however perceive how.

Robinhood itself is not a financial institution. Robinhood Banking is obtainable by Robinhood Cash, LLC, a fintech firm. Your cash is definitely held at Coastal Neighborhood Financial institution, Member FDIC, and swept throughout a community of companion banks. FDIC insurance coverage applies as pass-through protection at these insured banks (as much as $2.5 million complete), offered this system’s circumstances are met. So the underlying {dollars} sit in FDIC-insured establishments — however the safety flows by way of the companion banks, not from Robinhood immediately.

Key distinction: FDIC insurance coverage protects you if the companion financial institution fails — it doesn’t defend towards funding losses or towards a fintech operational failure. This is similar pass-through mannequin utilized by most fashionable neobanks.

For a deeper have a look at how Robinhood’s insurance coverage and account protections work throughout its brokerage and money merchandise, see our overview of whether or not Robinhood is secure. Backside line: Robinhood Banking is as secure as different respected neobanks, so long as you retain balances throughout the insured limits and deal with it as a pass-through fintech account relatively than a chartered financial institution.

Robinhood Banking vs. Conventional & On-line Banks

| Function | Robinhood Banking | Typical On-line Financial institution | Large Conventional Financial institution |

|---|---|---|---|

| Financial savings APY | As much as 4.00% | ~3.5% | ~0.38% |

| FDIC protection | As much as $2.5M (sweep) | $250K | $250K |

| Month-to-month value | $5 Gold (or $50/yr) | $0 | $0–$25 |

| Money supply | Sure (charge) | No | Department/ATM solely |

| Bodily branches | No | No | Sure |

The trade-off is evident: Robinhood Banking wins on yield, insured limits, and novelty, however you pay for Gold and there are not any branches. For those who worth in-person service or desire a really free account, a standalone on-line HYSA or an enormous financial institution might match higher. For those who hold significant money and are already paying for Gold, Robinhood is tough to beat.

Easy methods to Get Robinhood Banking

- Open a Robinhood account. Free and takes about 10 minutes. For those who don’t have one but, enroll right here.

- Subscribe to Robinhood Gold ($5/month or $50/12 months). New customers sometimes get the primary 30 days free.

- Be part of the Robinhood Banking waitlist from contained in the app. Entry is rolling out by invitation, so timing varies.

- Open your checking and/or financial savings account once you’re invited, then arrange direct deposit to unlock one of the best perks.

- Order your debit card and begin incomes as much as 4% APY in your financial savings.

Robinhood Banking: Professionals & Cons

| Professionals | Cons |

|---|---|

|

✅ As much as 4% APY with no cap or minimal ✅ As much as $2.5M FDIC protection by way of sweep ✅ Money delivered to your door ✅ Checking, joint & youngsters’ accounts ✅ Built-in with investing & the Gold Card ✅ No month-to-month account charge |

❌ Requires paid Robinhood Gold membership ❌ Robinhood just isn’t itself a financial institution (pass-through FDIC) ❌ No bodily branches ❌ Invite-only rollout ❌ Finest perks require month-to-month direct deposit ❌ APY is variable and might change |

Is Robinhood Banking Price It?

Robinhood Banking is value it if many of the following are true:

- You retain at the very least a number of thousand {dollars} in money (sufficient to clear the Gold charge after which some)

- You already pay for Robinhood Gold, or need its wider perks

- You need excessive FDIC protection with out juggling a number of banks

- You’re comfy with a branchless, app-first financial institution

It’s not value it should you hold little or no money (the Gold charge erodes your curiosity), you desire a utterly free account with no membership, otherwise you depend on in-person department service. In these instances, a standalone high-yield financial savings account will get you a comparable price with no subscription connected.

Continuously Requested Questions

No. Robinhood is a monetary expertise firm, not a financial institution. Robinhood Banking is obtainable by way of Robinhood Cash, LLC, and the precise banking providers and FDIC insurance coverage are offered by Coastal Neighborhood Financial institution, Member FDIC, together with a community of companion banks.

Robinhood Banking financial savings pays as much as 4.00% APY for Robinhood Gold members, with no cap and no minimal stability. The speed is variable and might change with market circumstances. Promotional boosts for brand spanking new accounts can quickly increase the efficient first-year yield.

Sure, by way of pass-through protection. Deposits are held at Coastal Neighborhood Financial institution and swept throughout companion banks, extending FDIC insurance coverage as much as $2.5 million complete. The protection comes from the insured companion banks, not from Robinhood itself, and applies when this system’s circumstances are met.

Sure. Robinhood Banking is out there solely to Robinhood Gold members, which prices $5/month or $50/12 months. For those who cancel Gold, you lose entry to the banking accounts and the highest APY.

Sure. Robinhood Banking gives on-demand money supply in supported areas. You request money within the app and it’s delivered to you, sometimes for a charge of as much as about $8.99 per supply. Availability relies on your location.

Open a Robinhood account, subscribe to Robinhood Gold, and be a part of the Robinhood Banking waitlist contained in the app. Entry is rolling out by invitation, so wait occasions fluctuate. As soon as invited, you possibly can open checking and financial savings accounts and arrange direct deposit.

It may be, should you hold sufficient money to justify the Gold charge and worth the additional FDIC protection and options. A standalone high-yield financial savings account gives an identical price with no membership required, so the only option relies on your stability and whether or not you need Robinhood’s different perks.

The Backside Line

Robinhood Banking is among the most aggressive makes an attempt but by a fintech to change into your major financial institution. As much as 4% APY, as much as $2.5 million in FDIC protection, money delivered to your door, and tight integration with investing and the Gold Card make it a genuinely compelling bundle — particularly should you’re already paying for Robinhood Gold.

The caveats are simply as essential. Robinhood isn’t a financial institution, one of the best price is locked behind a paid membership, and there are not any branches should you want in-person assist. For savers with actual money balances who reside within the app already, Robinhood Banking is a robust improve over a big-bank checking account. For everybody else, a free standalone high-yield financial savings account might ship many of the profit with out the subscription.

Both manner, Robinhood Banking raises the bar for what a contemporary account ought to provide — and it’s placing actual stress on the legacy banks which have coasted on 0.38% financial savings charges for years.

{kind=link}