LumerB

This text was revealed on Dividend Kings on Monday, June twenty sixth

—————————————————————————————

My loyalty isn’t to an organization, not even a dividend aristocrat.

My loyalty is to you, my readers, and meaning to the reality, as greatest as anybody can realize it.

When the information change, I modify my thoughts, what do you do sir?” – John Maynard Keynes

- 3M Is Struggling, So Purchase These 7+% Yielding Dividend Aristocrats As an alternative

Right here is my warning of 3M’s deteriorating fundamentals in December of 2022.

- 3M’s Dividend Danger Is Rising, So Purchase These 2 Greater-Yielding Options

3M’s Dividend Streak May Be About To Finish

And right here is my warning that 3M’s dividend security was persevering with to deteriorate.

3M (NYSE:MMM) Security And High quality Rating Down Grade Due To Regulation Go well with Prices

Dividend Security

| Score | Dividend Kings Security Rating (250 Level Security Mannequin) | Approximate Dividend Minimize Danger (Common Recession) | Approximate Dividend Minimize Danger In Pandemic Degree Recession |

| 1 – unsafe | 0% to twenty% | over 4% | 16+% |

| 2- under common | 21% to 40% | over 2% | 8% to 16% |

| 3 – common | 41% to 60% | 2% | 4% to eight% |

| 4 – protected | 61% to 80% | 1% | 2% to 4% |

| 5- very protected | 81% to 100% | 0.5% | 1% to 2% |

| MMM | 53% | 2.00% | 5.40% |

| Danger Score | Medium Danger 89th percentile threat administration $2 billion per yr lawsuit liabilities | A unfavourable outlook credit standing =0.66% 30-year chapter threat | 2.5% or much less max threat cap- speculative |

Total High quality

| MMM | Ultimate Rating | Score |

| Security | 53% | 3/5 common |

| Enterprise Mannequin | 90% | 3/3 wide-moat |

| Dependability | 53% | 3/5 common |

| Whole | 65% | 9/13 Above-average |

| Danger Score |

3/5 medium- Danger |

|

| 2.5% OR LESS Max Danger Cap Rec – speculative |

30% Margin of Security For A Probably Good Purchase |

3M’s security and high quality rating, primarily based on a 3,000-point high quality mannequin that comes with over 1,000 fundamentals and which is designed to be 95% correct at predicting dividend security in recessions, has continued to deteriorate.

Let me make clear that the chance of a dividend minimize stays small to gentle, for the traditionally common S&P firm with its present fundamentals, throughout a recession.

The chance is greater for any particular firm, reminiscent of 3M dealing with tens of billions in potential litigation prices and the $12.5 billion it simply settled for with 300 cities and states over PFAS.

In line with my Bloomberg Terminal, in a current convention name, 3M’s CFO is responding to an analyst about whether or not 3M’s dividend will probably be maintained. “So we’ll need to see as that performs itself out” – 3M CFO.

That is hardly a ringing endorsement of dividend security from the individual in control of operating 3M’s books.

Why 3M May Be The Subsequent Failed Dividend King

Let me be clear, a “failed dividend king” is a dividend king that cuts its dividend and loses its streak. It doesn’t suggest a bankrupt firm.

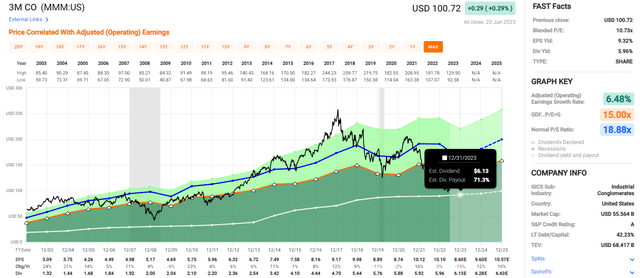

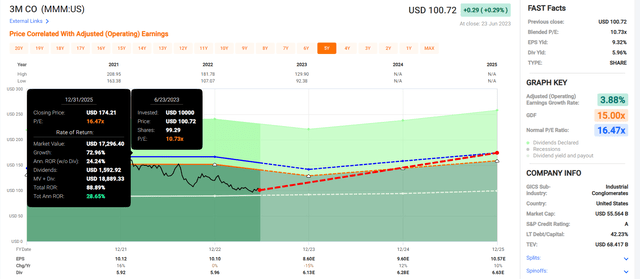

FAST Graphs, FactSet

For the time being, the consensus from 21 analysts is that 3M will NOT minimize its dividend.

FactSet Analysis Terminal

FactSet additionally exhibits no dividend minimize, although elevated payout ratios by means of 2025.

For context, 60% or decrease payout ratios are thought of protected for industrials, in keeping with score companies.

However that is as we speak, and issues may hold getting worse for 3M. I’m warning buyers, for a third time, for one easy motive.

Large Moat Analysis

When the dividend is minimize, statistically talking, it is time to promote.

So let’s take a look at the newest information from 3M’s years-long authorized wrestle to see why about $2 billion in long-term authorized prices could possibly be about to show 3M into the following failed dividend king.

Upon additional evaluation, we transfer our 3M Uncertainty Score to Very Excessive. In keeping with our June 23 be aware, we predict estimating 3M’s authorized dangers is a extremely unsure train. We reiterate that we predict the settlement cost poses a threat to the dividend, notably after the upcoming healthcare spinoff and with extra lingering authorized dangers like per- or poly-fluoroalkyl substance-related private damage or extra environmental claims.” – Morningstar

Morningstar now estimates that the whole PFAS settlement prices, together with the $12.5 billion settlement reached with states and cities, will whole about $20 billion.

The settlement with cities and states doesn’t cowl a number of different pending circumstances.

The $12.5 billion will probably be paid out over 13 years, about $1 billion per yr that will probably be hanging round 3M’s neck till 2036.

FactSet Analysis

3M’s dividend prices $3.4 billion per yr, and in 2023, it is anticipated to generate $4.3 billion in free money stream.

So principally, the annual settlement value brings the payout ratio to 100% on a free money stream foundation.

Word that greater free money flows are anticipated to deliver this down sooner or later.

Nevertheless, dividend sustainability is extra than simply payout ratios.

SA

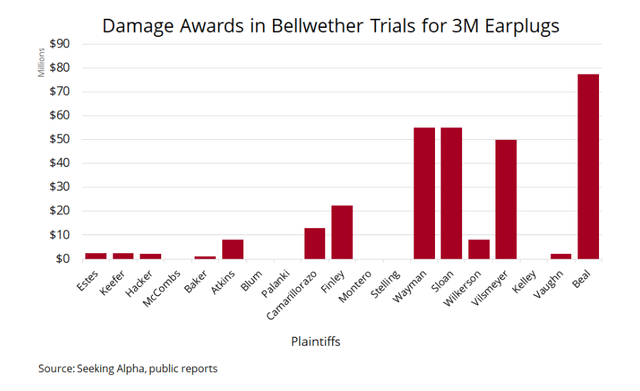

There are 260,000 pending circumstances over earplugs during which US army servicemen and ladies are claiming that 3M earplugs resulted in listening to loss.

The awards given by Juries to date vary from a couple of million to nearly $80 million.

Here is the excellent news for 3M about that.

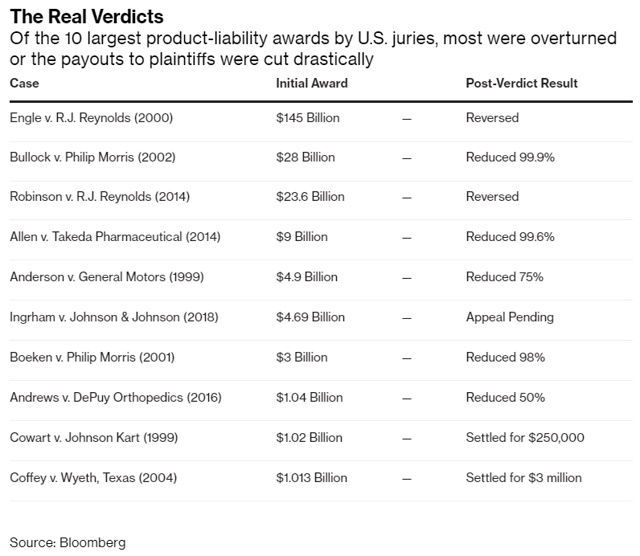

Bloomberg

Usually, very giant jury awards are overturned on enchantment.

Here is the unhealthy information for 3M.

- 3M unit appeals the dismissal of chapter case associated to army earplug lawsuits

On Friday, U.S. Chapter Decide Jeffrey Graham in Indianapolis dismissed Aearo’s chapter declare, describing it as “fatally untimely.” – SA

MMM has angered judges by making an attempt the “Texas Two Step,” during which it transfers all lawsuits to a subsidiary known as Aearo Applied sciences, then that firm recordsdata for chapter, and 3M settles all excellent claims for about $3 billion.

3M has claimed it isn’t answerable for the listening to loss as a result of it was following DOD specs, and so the federal government must be liable.

The DOD claims 3M tousled manufacturing after which knowingly stored promoting the earplugs.

The worst-case state of affairs for 3M is estimated to be $140 billion in ear-plug liabilities by means of $4 to $20 billion, which is estimated to be the ultimate value after appeals.

Morningstar estimates $4 billion for a complete lawsuit legal responsibility value of $24 billion.

The consensus vary is about $10 to $15 billion for earplugs.

- $22.5 billion to $35 billion whole authorized value

That works out to about $2 billion to $3 billion per yr in authorized prices for the following 13 years or so to simply over $2 billion.

3M’s Spin-Off Provides Even Extra Uncertainty

3M is planning on spinning off its medical division, which is its best-performing unit, in early 2024.

This may create two corporations, and if the cumulative dividend of each is $6/share, then 3M’s streak stays intact.

Nevertheless, as 3M’s CFO is now saying, it’s too early to say whether or not 3M buyers will probably be made entire or if the brand new mixed dividend goes to be smaller.

It is extremely probably 3M’s dividend goes to be diminished as a result of the medical division generates about 30% of free money stream.

- post-spin 3M will probably be producing about $3 billion in free money stream

- and $2 billion in probably annual authorized bills

The spin-off itself is predicted to deliver 3M, about $10.5 billion, practically paying for the PFAS settlement.

- That solely settles most of, not all of, these claims

Why does Morningstar imagine that 3M goes to need to pay $7.5 to $10 billion extra to settle PFAS?

As a result of the case towards 3M may be very robust.

Minnesota sued 3M and settled for practically $1 billion as a result of its without end chemical compounds have been each poisonous and contaminating folks at a startling charge.

Biomonitoring research by the Federal Facilities for Illness Management and Prevention present that the blood of practically all People is contaminated with PFAS.” – Environmental Working Group

So 3M poisoned the nation (in addition to many of the world).

PFAS are in all places and in most animals surveyed,” mentioned Rainer Lohmann, a professor of oceanography on the College of Rhode Island who focuses on PFAS contamination and was not concerned within the Environmental Working Group’s evaluation. “However gathering that info and placing it collectively is a big effort. And I’m not certain most of the people is totally conscious how completely these chemical compounds have penetrated the surroundings.” – NYT

So it seems that 3M could have probably poisoned lots of of tens of millions of individuals, probably billions. It is a good factor (for 3M) that the majority international locations do not have class motion legal guidelines, or they could possibly be dealing with trillions in liabilities.

So between $8 billion and $1.6 trillion per yr to repair the PFAS downside globally. $330 million to $66 billion per yr within the US. Undecided how cost-effective that is, however one factor’s for certain, 3M in all probability cannot afford it.

- The worldwide financial system is roughly $100 trillion

- cleansing up PFAS simply in human water may value 1.6% of the worldwide GDP

- cleansing up the oceans is economically unfeasible

Bankrupting the corporate isn’t going to assist anybody, however now you hopefully get an thought of the scale of this downside.

S&P charges 3M 89th percentile on international threat administration. I will defer to their experience given their 1,000 metric threat mannequin, however this information makes me personally query that rating.

However Wait, It Will get Worse

Whether or not or not you are mad sufficient at 3M for poisoning you and your loved ones, together with what seems to be the complete nation and far of the world and its meals chain, to not personal the inventory is a private problem.

Nevertheless, all this authorized legal responsibility, together with the spin-off of its greatest unit (largely to pay authorized payments), has badly damage 3M’s development outlook.

FactSet Analysis Terminal

Earlier than the settlement information, 3M’s long-term median development consensus was 7.2%.

It has been minimize in half on information of what’s going to probably be $2 billion to $3 billion in annual settlement prices.

- Assuming that the earplug settlements are “solely $4 to $15 billion.”

So even when 3M’s 6% yield was nonetheless protected, which is very unsure, it means the long-term whole return potential is now 9.5%.

FAST Graphs

3M rising on the new slower charge is traditionally value about 16.5X earnings, which suggests that it COULD probably ship round 100% returns by 2025.

That is enticing, however keep in mind that long-term 3M is now providing quite uninspiring return potential.

| Funding Technique | Yield | LT Consensus Progress | LT Consensus Whole Return Potential | Lengthy-Time period Danger-Adjusted Anticipated Return |

| Vanguard Dividend Appreciation ETF | 1.9% | 10.7% | 12.6% | 8.8% |

| Nasdaq | 0.8% | 11.2% | 12.0% | 8.4% |

| Schwab US Dividend Fairness ETF | 3.6% | 7.6% | 11.2% | 7.8% |

| REITs | 3.9% | 7.0% | 10.9% | 7.6% |

| Dividend Champions | 2.6% | 8.1% | 10.7% | 7.5% |

| Dividend Aristocrats | 1.9% | 8.5% | 10.4% | 7.3% |

| S&P 500 | 1.7% | 8.5% | 10.2% | 7.1% |

| 3M | 6.0% | 3.5% | 9.5% | 6.7% |

| 60/40 Retirement Portfolio | 2.1% | 5.1% | 7.2% | 5.0% |

(Supply: FactSet, Morningstar)

So, assuming you may forgive 3M for poisoning you and your loved ones, and also you’re OK with what could also be years of ongoing lawsuits, 3M is providing you worse return potential than hottest ETFs.

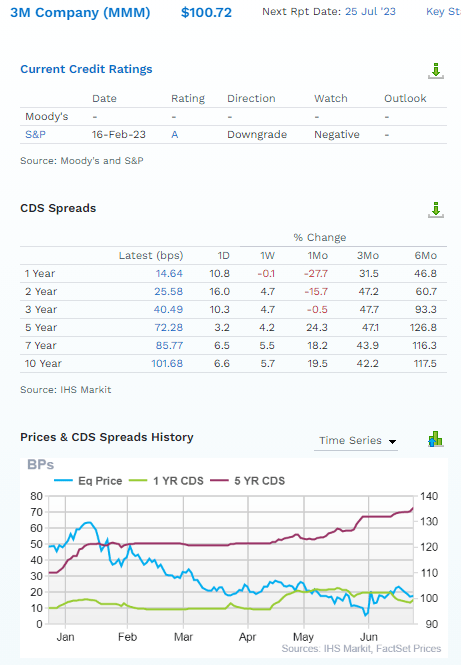

FactSet Analysis Terminal

The excellent news is that the bond market estimates the chance of 3M going bankrupt within the subsequent 30 years at about 3%, an A- rated firm.

However that threat is up 118% within the final six months.

A lot Safer Excessive-Yield Options To 3M

I did a fast display that took me 1 minute to discover a checklist of protected options to 3M.

- non-speculative (no turnarounds)

- credit standing: A- or higher

- 81+% security rating (very protected 1% to 2% threat of a minimize in extreme recession)

- 11+% long-term consensus whole return potential (vs. 10% S&P and 11% aristocrats)

Dividend Kings Zen Analysis Terminal

I’ll summarize U.S. Bancorp (USB) and Philip Morris (PM) PURELY as a result of EPD and OTCPK:ALIZY have tax implications that some buyers do not wish to cope with.

- EPD K1 tax type

- ALIZY 26% dividend tax withholding (personal in taxable accounts to get a tax credit score)

All these different options are nice. I haven’t got time to speak about all of them.

U.S. Bancorp: The King Of Tremendous Regional Banks

Additional Studying

- U.S. Bancorp: A 5.5% Yielding Buffett Model Desk-Pounding Purchase

Why USB Is A Nice Purchase Right now

Based in 1929 in Minneapolis, Minnesota, US is a 94-year-old financial institution that has survived and thrived by means of:

-

15 recessions

-

the Nice Despair

-

inflation as excessive as 22%

-

rates of interest as excessive as 20%

-

23 bear markets

-

the Nice Monetary Disaster (throughout which it remained worthwhile)

U.S. Financial institution is Morningstar’s “lowest threat” regional financial institution suggestion with the bottom threat of a financial institution run.

Why?

“U.S. Bancorp is the most important non-GSIB within the U.S. and has been one of the vital worthwhile regional banks we cowl. Few home rivals can match its working effectivity and returns on fairness over the previous 15 years.” – Morningstar

USB is the brand new gold commonplace of excellent banking, a title as soon as held by Wells Fargo earlier than it sank below an ocean of scandal.

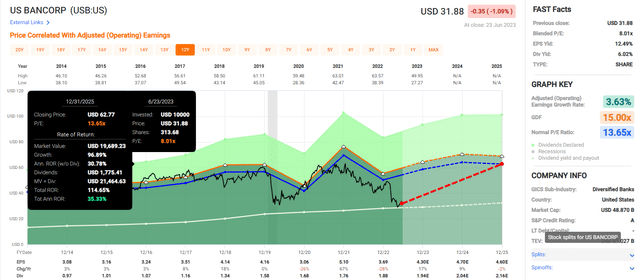

Basic Abstract

- DK high quality rating: 79% medium threat 12/13 Tremendous SWAN

- DK security rating: 88% very protected dividend (1.6% dividend minimize threat in extreme recession)

- Historic honest worth: $60.43

- Present worth: $31.88

- Low cost to honest worth: 47%

- DK score: potential Extremely Worth (Buffett-style fats pitch) purchase

- Yield: 6.0%

- Lengthy-term development consensus: 9.0%

- Consensus long-term return potential: 15.0%

FAST Graphs, FactSet

USB affords 115% return potential over the following 2.5 years, about 30% greater than 3M.

Philip Morris: Dividend King Which Is the Trade Progress King

Additional Studying

- Altria Vs. British American Vs. Philip Morris: Battle Of The Excessive-Yield Aristocrats

Why PM Is A Good Purchase Right now

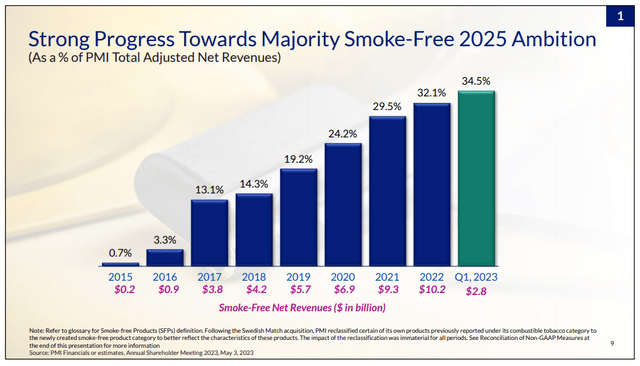

investor presentation

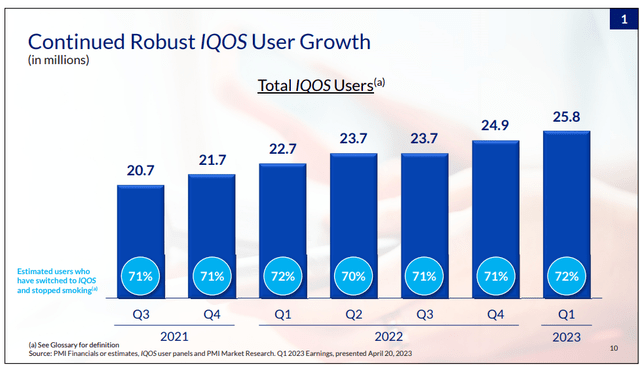

PM is the trade chief in reduced-risk merchandise, producing 35% from RRPs.

investor presentation

iQos is PM’s heat-stick model, and 72% of people who smoke who attempt it change completely and quit smoking.

iQos can also be now producing gross margins 0.1% above PM’s conventional cigarettes.

FactSet Analysis Terminal

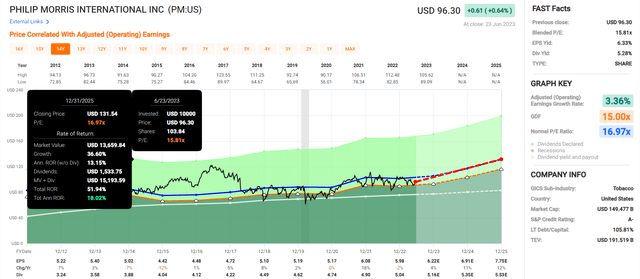

PM’s development consensus is nearly as excessive as 3M’s total whole return potential.

Basic Abstract

- DK high quality rating: 98% very low threat 13/13 Extremely SWAN dividend king

- DK security rating: 100% very protected dividend (1.0% dividend minimize threat in extreme recession)

- Historic honest worth: $109.25

- Present worth: $96.30

- Low cost to honest worth: 12%

- DK score: potential good purchase

- Yield: 5.3%

- Lengthy-term development consensus: 8.7%

- Consensus long-term return potential: 14.0%

FAST Graphs, FactSet

PM’s short-term return potential is much like the long-term return potential, which is very enticing and sustainable.

Backside Line: 3M’s Dividend May Be Doomed, So Purchase Safer Options

It now seems that 3M could have recognized that its earplugs have been faulty and stored promoting them anyway, harming the listening to of practically 300,000 US troopers.

It’ll probably take years for the reality of that to come back out.

However what’s not unsure is that 3M spent a long time producing poisonous chemical compounds which have contaminated basically all People. Globally PFAS is current in nearly all marine animals, having contaminated a lot of the world’s oceans. Billions of people have been poisoned, although not solely by 3M.

Bloomberg estimates that 3M could need to tackle $15 billion in new debt, doubling its curiosity prices throughout a interval of excessive charges, which may ship its debt/EBITDA to 5X and add $1 billion in annual curiosity prices.

If that occurs, this dividend can be recklessly unsustainable as a result of it will lose 3M’s A-credit score.

Must you promote 3M? That is a private selection, however I might, if solely as a result of poisoning all People with poisonous chemical compounds and masking it up for many years is an moral line I can not cross.

Word that 3M continues to be owned in standard ETFs like VIG and SCHD, and so long as the dividend stays uncut, it’ll stay in these ETFs, so I’ll personal a small quantity.

S&P says that even with the diabolically unethical PFAS contamination, it is nonetheless a really well-run firm, so I might be superb proudly owning 3M by way of ETFs…if it avoids a dividend minimize.

If it cuts its dividend, then I might promote and by no means look again.

SCHD and VIG’s high quality screens will eradicate 3M, and I will probably be glad to be rid of it.

3M is a dividend development legend and a hometown hero in my group, or it was.

However to be an excellent investor, it’s essential have loyalty solely to the reality, and the reality is that 3M has carried out unsuitable, very unsuitable.

Its turnaround, which started in 2018, is now in yr 5, and its authorized payments are forcing it to spin off its greatest enterprise unit.

Its development outlook has been minimize in half.

Whether or not or not you care about 3M’s ethics, USB and PM are much better options proper now.

And sure, I perceive the irony of claiming that “if you happen to’re bothered by 3M for poisoning the world, purchase a tobacco firm as a result of it is much less unethical. LOL.

- S&P nonetheless considers 3M to have superior threat administration than PM

- 3M 89th international percentile vs. PM’s 83%

However the level is that PM and USB supply superior dividend security and long-term return potential.

And dozens of very protected high-yield blue-chips at present appear to be higher investments than 3M.

{kind=link}