ryasick

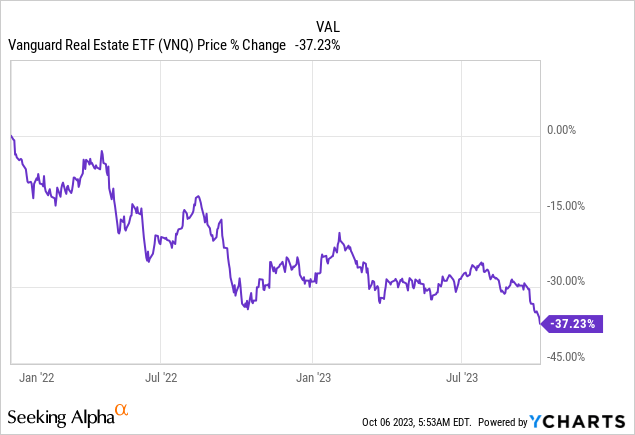

As we speak, actual property funding trusts, or REITs (VNQ), are priced at their lowest valuations because the nice monetary disaster. Their share costs have dropped by practically 40% because the starting of 2022 whilst their money flows have risen by 5-10% typically:

Because of this, valuations are actually roughly 2x decrease than in early 2022.

And that is simply the typical!

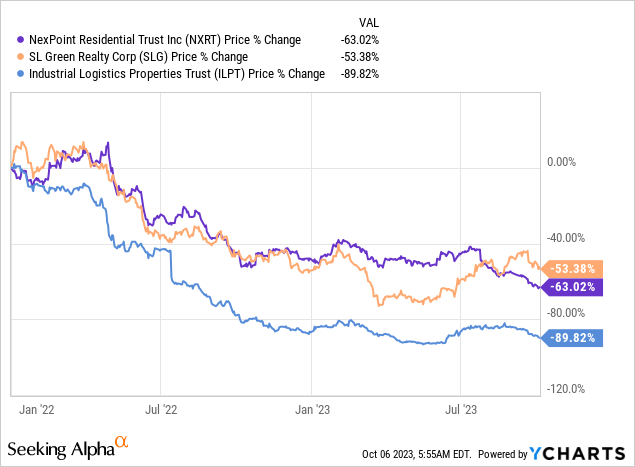

There are a selection of REITs which might be down nearer to 50, 60, and even 90% in essentially the most excessive circumstances:

That is how brutal this market has been on REITs…

We aren’t speaking a few correction anymore. It is a actual crash.

The worst one since 2008-2009!

It jogs my memory of the next quote of Warren Buffett

“The years forward will sometimes ship main market declines — even panics — that can have an effect on just about all shares. Nobody can let you know when these traumas will happen… The most effective likelihood to deploy capital is when issues are happening. When it rains gold, put out the bucket, not the thimble.” Warren Buffett.

Briefly, what he’s saying right here is that fortunes are made throughout bear markets when worry is excessive and alternatives are ample.

Costs usually drop too low attributable to extreme pessimism, after which on prime of that, it additionally results in indiscriminate promoting with each inventory in a given sector dropping, no matter their fundamentals.

That is exactly what has occurred with REITs, and it has led to some distinctive shopping for alternatives.

Certain, an overleveraged REIT with workplace properties might need to commerce at a decrease valuation, however these are literally the minority.

Most REITs right this moment have robust steadiness sheets with low debt and personal fascinating belongings that take pleasure in rising rents. And but, they’re now priced at big reductions relative to the honest worth of their belongings.

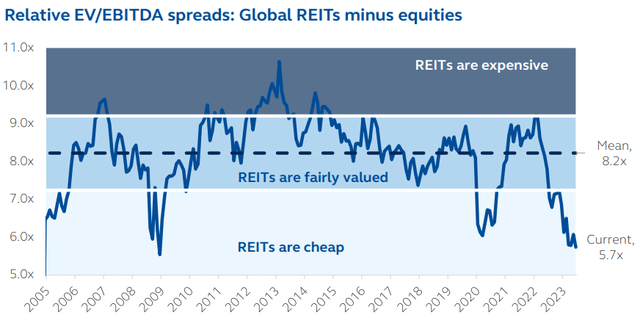

The final time valuations had been this low was following the nice monetary disaster, and REITs then tripled within the following two years:

Principal Asset Administration

As soon as extra, we expect that we’re introduced with a “once-in-a-decade” likelihood to win large within the REIT sector. In what follows, we current three of our Prime Picks to capitalize on this chance.

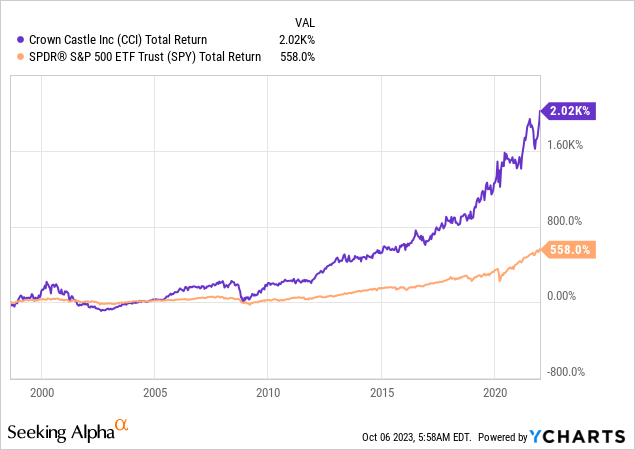

Crown Fort Inc. (CCI)

Crown Fort is slowly changing into one in every of my largest holdings.

It is a blue-chip REIT that usually trades at a excessive valuation and low dividend yield as a result of:

- It owns a cell tower portfolio that generates recession-resistant money move with regular and predictable development prospects.

- It has a robust funding grade-rated steadiness sheet that limits the impression of rising rates of interest.

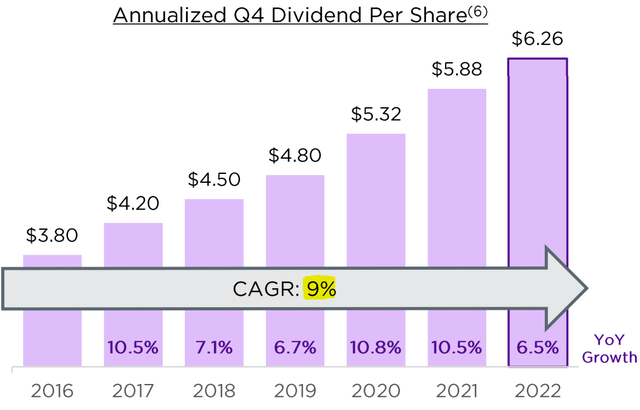

- It has traditionally been capable of develop its dividend by 9% per 12 months on common and massively outperformed the remainder of the inventory market:

Crown Fort

Because of this, the market usually costs it at 20-25x FFO and a low 3-4% dividend yield. That is warranted given the resilience of its fundamentals and its compelling development prospects.

Even a low 3% yield can get you to double-digit whole returns once you pair that with an 8% annual development charge.

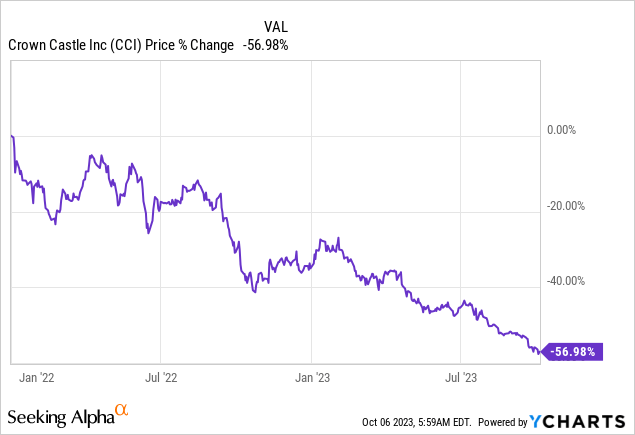

However right this moment is your likelihood to purchase CCI off the low cost rack. Its share worth has been minimize in half because the starting of 2022 whilst its money move and dividend saved on rising:

And this has resulted within the lowest valuation in over a decade for this blue-chip REIT:

| Sometimes | As we speak | |

| FFO A number of | 20-25x | 11.6x |

| Dividend Yield | 3-4% | 7% |

This exceptionally low valuation is the results of two issues:

Firstly, your entire REIT market has crashed, and this brought on all REITs, together with even blue chips like CCI, to endure from indiscriminate promoting.

After which secondly, CCI is dealing with a short lived slowdown in its development attributable to T-Cell’s latest acquisition of Dash. It is going to result in some lease cancellations by means of 2025 and stop CCI from rising till then.

This warrants a considerably decrease valuation, however I imagine that the market has overreacted to this and repriced CCI as if its development story was over endlessly. In actuality, our latest interview with CCI’s administration clearly revealed that they anticipate a return to their focused 7-8% dividend development charge by 2026. They’re very assured within the reacceleration of their development charge as a result of they’ve already contractually secured a lot of that development, giving them nice visibility.

The headwind from the Dash lease cancellations is just short-term, however the market is simply too centered on short-term outcomes to acknowledge this.

As such, you right this moment have the once-in-a-decade alternative to purchase shares of this blue-chip cell tower REIT at its lowest valuation because the nice monetary disaster.

I predict that as its development accelerates, the market will reprice it at a materially greater valuation a number of, leading to substantial upside to those that purchase it right this moment.

Simply getting again midway to its earlier peak would unlock 50% upside and that might nonetheless worth it at a traditionally low a number of.

Whilst you wait, you earn a 7% dividend yield, and when the expansion reaccelerates to 7-8%, you can be incomes ~15% common annual whole returns on a continuing a number of foundation.

It’s onerous to search out higher risk-to-reward in right this moment’s market.

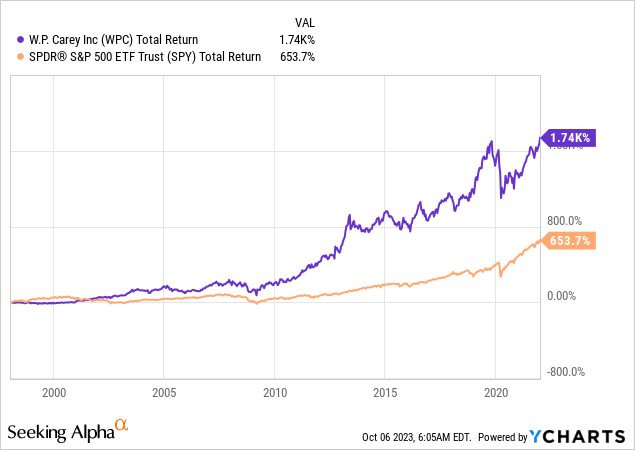

W. P. Carey Inc. (WPC)

W. P. Carey is one other blue-chip REIT that has offered off closely and now trades at a traditionally low valuation a number of:

- It owns primarily industrial internet lease properties that take pleasure in CPI-based hire changes, leading to speedy hire development in right this moment’s inflationary world.

- It has a robust funding grade-rated steadiness sheet that limits the impression of rising rates of interest.

- It has a multi-decade monitor report of great market outperformance, similar to CCI:

However it’s now priced at simply 10x AFFO, or put in a different way, a ten% money move yield.

This low valuation is very stunning when you think about that almost all industrial REITs generally commerce at >20x AFFO even following the latest crash. The most important, Prologis (PLD), presently trades at 22x AFFO.

They commerce at such excessive valuation multiples as a result of industrial properties are extremely sought-after as they straight profit from the rising tendencies of e-commerce and onshoring.

So why is WPC so closely discounted?

Properly, evidently the market is failing to see WPC as an industrial REIT as a result of traditionally, it has owned a diversified portfolio, together with some retail and workplace properties.

Nevertheless, that is now altering quickly.

Only in the near past, WPC introduced that it might spin off most of its workplace properties right into a separate REIT and unload the remainder. It is going to then reinvest the proceeds into principally industrial properties, which is able to enhance its allocation to ~2/3 of its portfolio:

W. P. Carey

The opposite 1/3 is right this moment invested in extremely resilient internet lease retail properties comparable to these owned by Realty Revenue (O). Take into consideration grocery shops and residential enchancment shops leased to a robust tenant below a ten+ 12 months lease with inflation-based hire escalators. That is very resilient.

W. P. Carey

I imagine that this spinoff is nice information for shareholders as a result of it’ll enable WPC to quickly get out of its worst belongings – all whereas growing its publicity to its finest belongings – decreasing dangers and enhancing its future development prospects.

However the market hates it due to one cause: it’ll result in a small dividend minimize.

WPC introduced that following the spinoff, it’ll barely cut back its dividend with a purpose to be in a greater place to self-fund its future development prospects.

That is completely comprehensible and the fitting factor to do for my part, contemplating that they’re shedding 10% of their belongings and their value of capital is right this moment too excessive to pursue accretive investments.

By organising the payout ratio at 70-75%, they are going to be much less reliant on capital markets and be capable to retain important earnings to purchase extra industrial properties, additional growing their allocation to this fascinating sector.

I predict that 5 years from now, their portfolio might be nearer to three/4 industrial and this can result in huge rerating of the inventory.

As I famous earlier, WPC is right this moment priced at simply 10x AFFO as a result of the market would not know to which peer group it belongs and dividend-oriented buyers are exiting the inventory.

However in 5 years, the market will understand WPC very in a different way and I anticipate it to commerce at a a number of that is nearer to these of business REITs.

This might unlock 50-100% upside from right here and whilst you wait, we anticipate to earn a 7% dividend yield even after the minimize.

Once more, it is a once-in-a-decade likelihood to purchase WPC at such a low valuation. It’s briefly hated, however I do not assume that this can final.

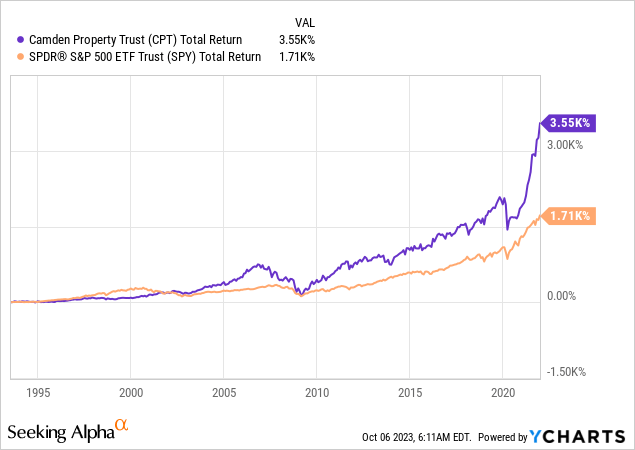

Camden Property Belief (CPT)

Lastly, I wish to focus on one in every of my favourite condo REITs.

If cell towers and industrial properties aren’t your factor, then maybe discounted condo communities will achieve your curiosity.

Camden Property Belief is without doubt one of the highest-quality condo REITs available in the market:

- It owns a high-quality portfolio of principally reasonably priced condo communities in robust sunbelt markets.

- It has one of many lowest leverages of all REITs with a low 30% LTV and simply 4.3x debt-to-EBITDA. This provides it a robust A-rated steadiness sheet.

- As soon as extra, it is a blue chip REIT with a protracted monitor report of great market outperformance and regular dividend development:

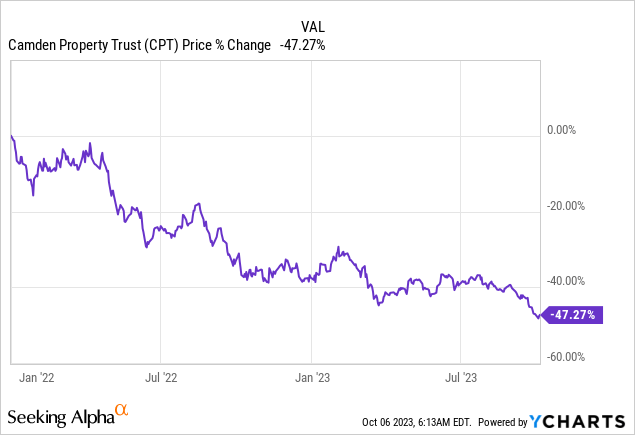

Nevertheless it wasn’t proof against the latest crash.

Nothing was.

And because of this, it’s now closely discounted:

This crash occurred whilst CPT saved rising its rents at a speedy tempo and so the low cost is even higher than it could appear.

To provide you a way of simply how low cost CPT has gotten, think about that it’s now priced at a close to 7% implied cap charge.

But, these belongings usually commerce at nearer to a 4.5-5% cap charge within the non-public market. Only in the near past, UDR, Inc. (UDR), one other condo REIT, introduced the acquisition of a Sunbelt condo portfolio at a 4.5% cap charge.

Because of this CPT is priced at a roughly 40% low cost to its internet asset worth in accordance with our personal estimates.

Camden Property Belief

That is moderately excessive! Sometimes, solely distressed REITs would commerce at such a big low cost, however CPT is an A-rated blue chip with a rising money move.

That is its lowest valuation in a decade.

In actual fact, its valuation has gotten so low that it lately received the eye of Starwood, which is a significant non-public fairness group that is run by legendary billionaire investor Barry Sternlicht.

Starwood’s newest 13F filling confirmed that they’d constructed CPT into their single largest place. I might add that Barry Sternlicht stated the next earlier this 12 months in a televised interview:

“By the best way, when credit score comes again, you’re gonna see REITs take off… There are some unbelievable bargains in REITs. We did the identical factor throughout the pandemic. We purchased a dozen shares everywhere in the world and we had a 70% IRR on that stuff. We’re already shopping for some stuff within the public market…” Barry Sternlicht, CEO/Chairman, Starwood Q3 2023 CNBC Interview.

That sums up the chance fairly properly.

Even in case you are conservative and assume that CPT’s NAV will come down fairly a bit because of the now greater rates of interest, we estimate that it might nonetheless have about 50% upside from right here and also you get a 4% dividend yield whilst you wait.

Backside Line

CCI, WPC, and CPT are three examples of once-in-a-decade shopping for alternatives within the REIT sector, however there are a lot of others.

I made a small fortune shopping for discounted REITs following the crash of 2020, and right this moment, these alternatives are much more compelling in lots of circumstances.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please concentrate on the dangers related to these shares.

{kind=link}