Revealed on December twenty eighth, 2022 by Nate Parsh

Healthcare hasn’t been spared within the sell-off in markets during the last yr. The markets have confronted a number of headwinds throughout this era, together with aggressive tightening of fiscal coverage by the Federal Reserve, the Russian invasion of Ukraine, and extreme Covid-19 restrictions in China, amongst others.

That stated, the healthcare sector is often one of many most secure locations to take a position. The merchandise, medicines, and medical gadgets supplied by the businesses on this sector usually stay in excessive demand throughout recessionary intervals.

This means to thrive in a tough financial surroundings is proof of a really robust enterprise mannequin and is a significant purpose why quite a lot of healthcare corporations have attained Dividend Aristocrat standing.

The Dividend Aristocrats are a choose group of 65 shares within the S&P 500 Index, with 25+ consecutive years of dividend will increase.

You’ll be able to obtain an Excel spreadsheet of all 65 Dividend Aristocrats (with metrics that matter corresponding to dividend yields and price-to-earnings ratios) by clicking the hyperlink under:

This text will look at three names within the healthcare sector which have a trailing one-year complete return of a minimum of -10% or worse, however supply a minimum of 10% complete returns over the following 5 years. Every inventory additionally pays a market-beating dividend that seems to be very protected.

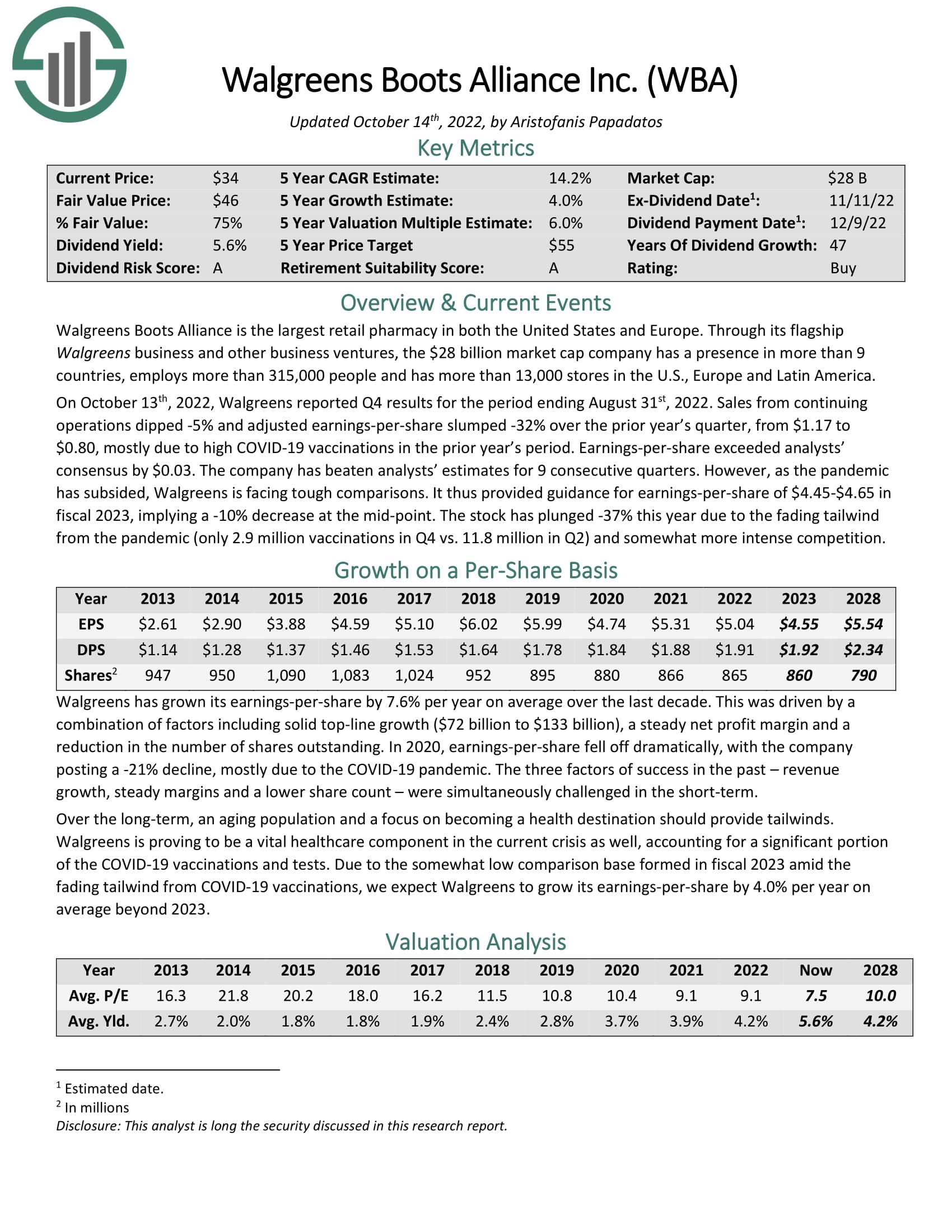

Prime Overwhelmed Up Healthcare Inventory #1: Walgreens Boots Alliance Inc. (WBA)

- 5-year anticipated complete return: 11.6%

- 1-year complete return: -19.9%

Walgreens is a prime title in retail pharmacy, having the most important footprint of any such firm in each the U.S. and Europe. The corporate has operations in additional than 9 nations, employs greater than 315,000 folks, and has greater than 13,000 shops throughout the U.S., Europe, and Latin America.

This massive-scale operation permits Walgreens to deal with a sizeable buyer pool that almost all rivals can not match. Such an operation is enticing to companions. For instance, the corporate and AmerisourceBergen Company (ABC) have an settlement in place for Walgreens to be the first distributor for branded and generic medicine for the corporate till a minimum of 2029.

This unmatched dimension and scale can be helpful to the corporate because the world’s inhabitants continues to age. In response to the World Well being Group, the variety of folks over the age of 60 outnumbered the youngsters beneath the age of 5 in 2020. By 2050, the proportion of the world’s inhabitants over the age of 60 years will nearly double to 22% from 2015 ranges.

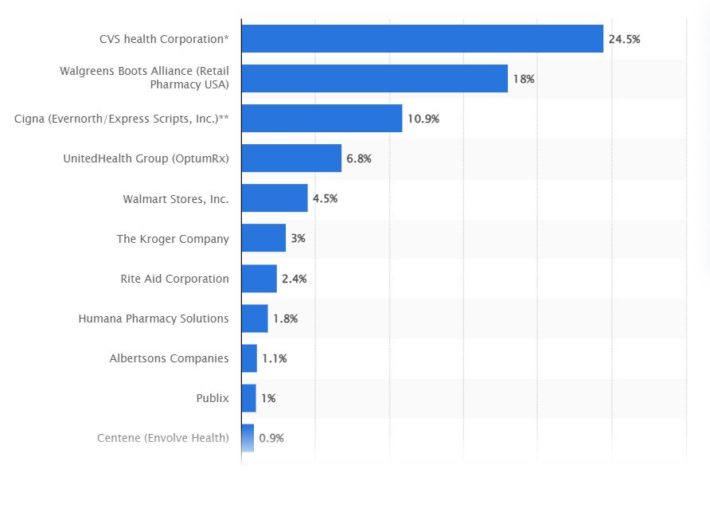

As folks age, they have a tendency to require extra well being care options. It will profit the sector on the whole, however Walgreens specifically as a result of off the variety of prescriptions and immunizations the corporate fills yearly. For instance, Walgreens stuffed 820 million prescriptions and immunizations within the U.S. alone throughout fiscal yr 2022. Because of this, Walgreens trails simply CVS Well being Company (CVS) when it comes to prescription drug market share.

Supply: Statista

These catalysts ought to permit for Walgreens to develop a minimum of 4% yearly via fiscal yr 2028.

Walgreens has raised its dividend for 47 years in a row, making the corporate a Dividend Aristocrat and simply three years away from turning into a Dividend King. Walgreens gives a yield of 5.0% that simply tops the typical yield of 1.7% for the S&P 500 Index. The projected payout ratio is simply 42% for this yr.

Walgreens has a price-to-earnings ratio of 8.5, under our goal of 10 instances earnings. Reaching our valuation goal by fiscal yr 2028 may add 3.6% to annual returns.

Subsequently, we anticipate that Walgreens will return 11.6% yearly over the following 5 years resulting from 4% earnings development, the 5.0% dividend yield, and a 3.6% tailwind from a number of growth.

Click on right here to obtain our most up-to-date Positive Evaluation report on Walgreens Boots Alliance Inc. (preview of web page 1 of three proven under):

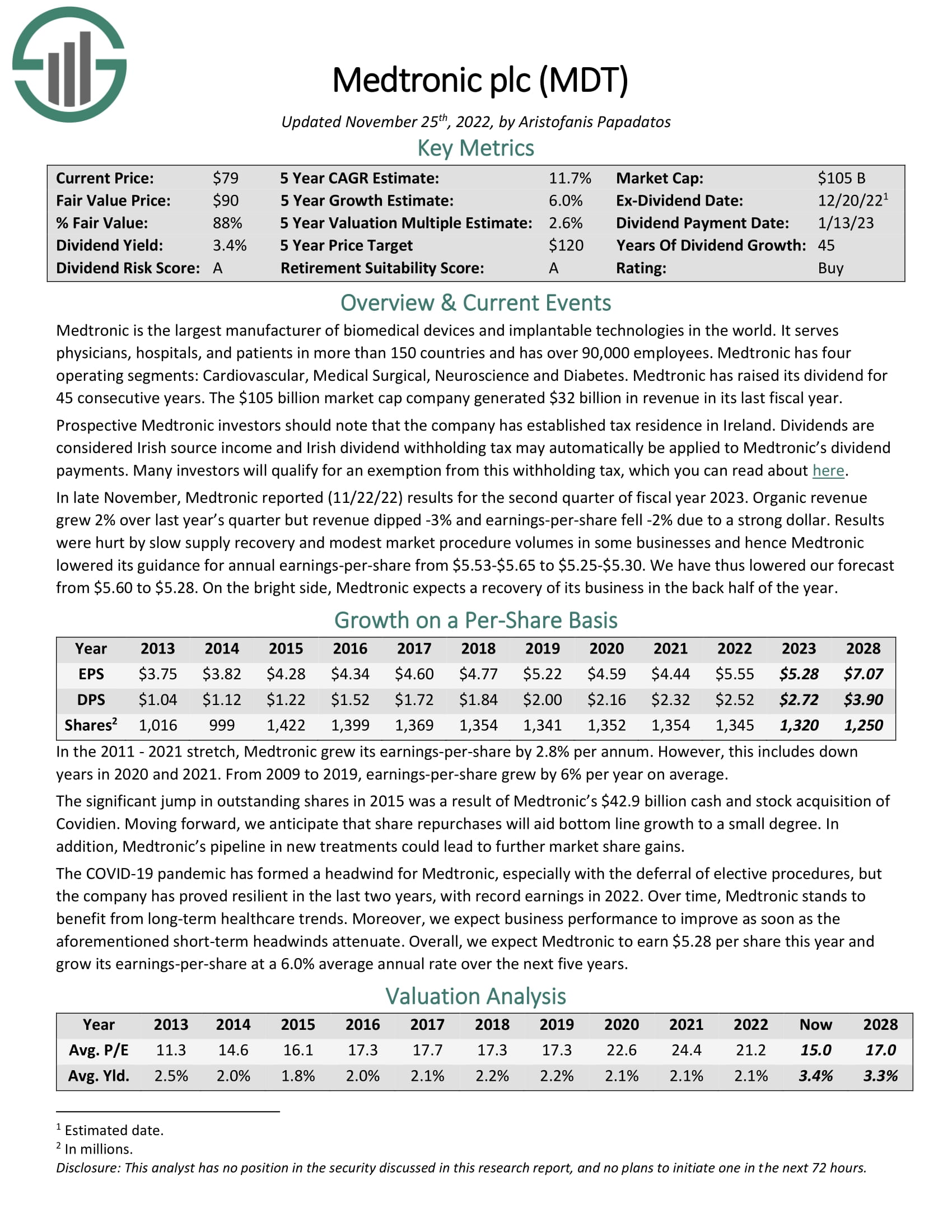

Prime Overwhelmed Up Healthcare Inventory #2: Medtronic plc (MDT)

- 5-year anticipated complete return: 12.1%

- 1-year complete return: -22.4%

Medtronic is the most important manufacture of biomedical gadgets and implantable applied sciences on the earth. This offers the corporate a scale unmatched by most friends as Medtronic’s merchandise are bought in additional than 150 nations.

The corporate consists of 4 segments, together with Cardiovascular, Medical Surgical, Neuroscience, and Diabetes. The corporate’s product contains implantable pacemakers, defibrillators, valves, stapling gadgets, sealing devices, robotic-assisted surgical procedure merchandise, insulin pumps, and glucose monitoring programs. This gives some diversification for Medtronic if a person section or product line faces headwinds whereas offering prospects with a protracted record of merchandise. This might make Medtronic a one-stop for main prospects trying to purchase the merchandise that they want.

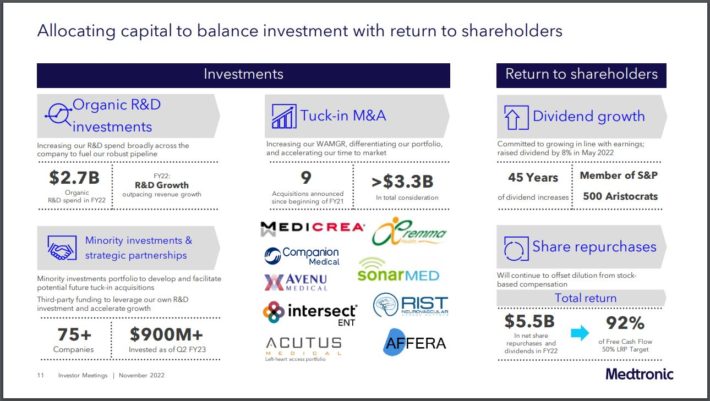

Medtronic has additionally been lively on the acquisition entrance so as to enhance its positioning in a bunch of classes.

Supply: Investor Presentation

The corporate has introduced 9 acquisitions during the last two fiscal years alone. Most of those have been of the bolt-on selection, serving to to enhance Medtronic’s management place. For instance, the corporate accomplished its buy of Affera, Inc. on August, thirtieth, 2022. The addition of Affera brings to Medtronic’s portfolio the first-ever cardiac mapping and navigation platform, which can assist present options for sufferers with irregular heartbeats and can be appropriate with the corporate’s current know-how.

Acquisitions have induced Medtronic to concern new shares during the last decade, which has saved a lid on earnings development over this era. Nonetheless, the fiscal years 2013 via 2022 noticed earnings develop by 4.5% yearly. We imagine a mixture of natural development and contributions from acquisitions will drive 6.0% yearly development over the following 5 fiscal years.

The decline within the share worth has pushed Medtronic’s yield to three.5%, a stage hardly ever seen in additional than a decade for the inventory. We forecast a payout ratio of 52%, which seemingly signifies that the corporate’s 45-year dividend development streak ought to stay intact.

Medtronic has a price-to-earnings ratio of 14.7, one of many lowest valuations the inventory has traded at since a minimum of 2013. Our goal price-to-earnings ratio is 17, which suggests a tailwind from a number of growth of three.0% per yr.

Because of this, we mission that shareholders of Medtronic may see annual returns totaling 12.1%, stemming from 6.0% earnings development, the three.5% dividend yield, and a 3.0% contribution from the increasing a number of.

Click on right here to obtain our most up-to-date Positive Evaluation report on Medtronic plc (preview of web page 1 of three proven under):

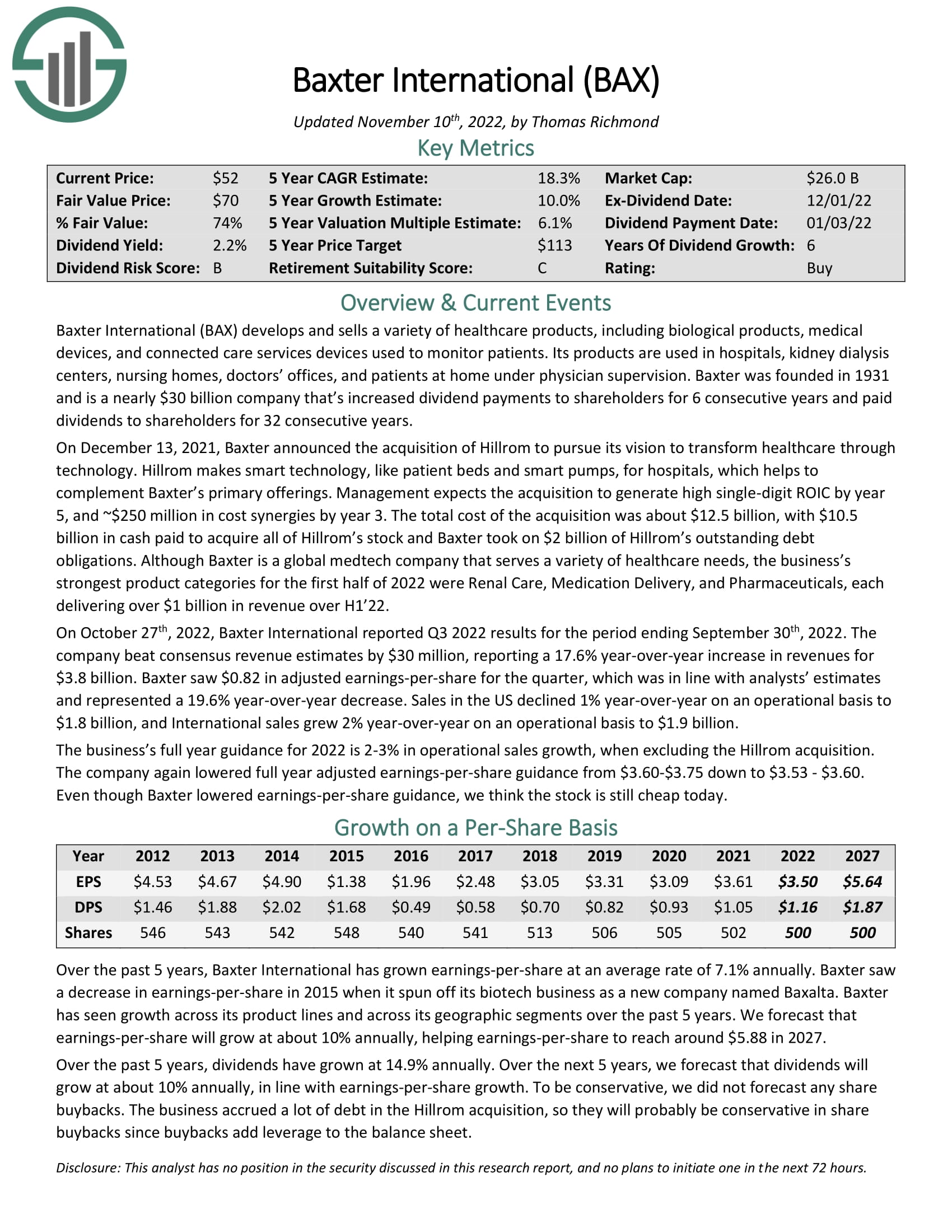

Prime Overwhelmed Up Healthcare Inventory #3: Baxter Worldwide (BAX)

- 5-year anticipated complete return: 19.2%

- 1-year complete return: -40.3%

Baxter develops and sells a wide range of healthcare merchandise, which incorporates organic merchandise, medical gadgets and linked care providers gadgets used to observe sufferers. This offers the corporate a reasonably broad buyer pool, which incorporates hospitals, medical doctors’ workplaces, and nursing houses. Baxter is also a number one title within the space of kidney well being, making dialysis facilities one of many firm’s prime prospects. The corporate’s prime performing companies to this point in the course of the yr have been Renal Care, Medicine Supply, and Prescription drugs.

The corporate has additionally used acquisitions to drive development. For instance, Baxter introduced on December thirteenth, 2022 that it had agreed to buy Hillrom, a maker of sensible know-how corresponding to affected person beds and sensible pumps. The acquisition price $12.5 billion, however ought to present excessive single-digit return on invested capital by the fifth yr after closing.

Hillrom is already factoring closely into outcomes as it’s anticipated to contribute meaningfully to development this yr.

Supply: Investor Presentation

Baxter spun off its biotech firm Baxalta in 2015, which led to a lower in earnings-per-share. Nonetheless, the corporate’s earnings-per-share have elevated at an annual fee of simply over 7% over the previous 5 years. This development has been pushed by beneficial properties throughout all merchandise strains and in most geographic areas, demonstrating the energy of Baxter’s product portfolio in addition to its attain. Subsequently, we forecast earnings development of 10% per yr for the following 5 years.

The corporate has raised its dividend yearly since spinning off Baxalta. Shareholders have additionally acquired a dividend for 32 consecutive years. The projected payout ratio for the present yr is simply 33%, making Baxter’s dividend seemingly very protected. Shares yield 2.2%.

Shares of Baxter are buying and selling at simply over 14 instances anticipated earnings-per-share for the yr. With a goal a number of of 20 instances earnings, this suggests a 6.9% annual tailwind to outcomes over the following half-decade.

In complete, we mission that Baxter will present a complete return of 19.2%, stemming from 10% earnings development, the beginning yield of two.2%, and a mid-single-digit contribution from a number of growth.

Click on right here to obtain our most up-to-date Positive Evaluation report on Baxter Worldwide (preview of web page 1 of three proven under):

Ultimate ideas

The healthcare sector has seen quite a lot of its main names undergo vital drawdowns within the share worth during the last yr.

The constructive aspect of this prevalence is that many shares are buying and selling with very enticing complete return profiles. Even higher, these shares supply market beating dividend yields that look like very protected.

Walgreens, Medtronic, and Baxter all have double-digit complete return potential whereas providing protected and safe dividend yields. Every business main firm can also be buying and selling under our valuation goal. For buyers in search of worth and earnings, these three shares may make enticing funding choices.

The next articles comprise shares with very lengthy dividend or company histories, ripe for choice for dividend development buyers:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}