Revealed by Nathan Parsh on November twenty ninth, 2022

Utilities are sometimes a favourite of dividend progress traders as they’ll present glorious returns and high-income ranges.

Corporations on this sector can accomplish that as a result of they usually maintain regulatory-based aggressive benefits limiting competitors. Utilities can usually apply and obtain approval for charge base will increase as they make upgrades and investments of their infrastructure. This will result in reliable money flows that then be distributed to shareholders within the type of dividends.

As such, many utility shares usually have dividend yields which are a number of occasions that of the typical inventory within the S&P 500 Index.

Due to these favorable business traits, we’ve compiled an inventory of utility shares. The listing is derived from the main utility sector exchange-traded funds JXI, VPU, and XLU.

You’ll be able to obtain the listing of all utility shares (together with vital monetary ratios corresponding to dividend yields and payout ratios) by clicking on the hyperlink under:

Electrical utilities are one of the vital frequent varieties within the sector, as these corporations present power to customers which are wanted each day.

Most electrical energy consumption within the U.S. is because of lighting, home equipment, heating, air flow, and air-con. However moreover powering properties, companies, and industrial amenities, electrical energy can be wanted to satisfy the rising demand from the elevated adoption of electrical automobiles.

On the finish of 2021, it was estimated that there have been already 2.3 million electrical vehicles on the highway, representing about 1% of the entire within the U.S. This leaves a lot room for progress. Whereas the entire variety of electrical automobiles continues to be low, the expansion charges have been very excessive. Whole world electrical vehicles bought had been up 107% in 2021 and adopted a 98% improve in 2020. There may be a lot demand for electrical automobiles that’s rising.

This text will look at 10 of our favourite electrical utility names, ranked so as of potential returns over the subsequent 5 years (whole anticipated returns are primarily based on closing inventory costs for the November 25th, 2022, buying and selling session).

Prime Utility Inventory #10: Sempra Vitality (SRE)

- 5-year anticipated annual returns: 7.7%

Based over twenty years in the past, Sempra Vitality has blossomed into an almost $51 billion market cap firm. Sempra Vitality operates in Southern California, giving the corporate one of many largest utility buyer bases within the U.S. The corporate gives electrical energy and pure fuel to greater than 20 million clients.

Sempra Vitality additionally has a majority stake within the Texas-based Oncor. This transmission and distribution enterprise gives electrical energy to greater than 10 million clients. As well as, Sempra Vitality owns and operates different utilities and service provider renewable power tasks, liquefied pure fuel amenities, and fuel pipes and storage within the U.S. and Latin America.

Sempra Vitality reported third-quarter earnings outcomes on November 3rd, 2022.

Supply: Investor Presentation

The corporate’s earnings-per-share grew 16% to $1.97 and got here in $0.19 above analysts’ anticipated. Consequently, administration raised its annual earnings-per-share steering to $8.70 to $9.00 in comparison with $8.10 to $8.70.

Lengthy-term, Sempra Vitality expects to develop its earnings-per-share by 6% to eight% because of an intensive capital funding plan and buyer progress in its areas of operation. Erring on the facet of warning, we undertaking earnings-per-share progress of 5% over the subsequent 5 years.

Sempra Vitality has elevated its dividend for the previous 12 years and has a projected payout ratio of simply 52% for 2022, a really low determine for a utility firm. Shares yield 2.8%, which compares nicely to the 1.6% common yield for the S&P 500 Index.

Lastly, shares of the corporate are buying and selling close to our five-year goal price-to-earnings (P/E) ratio of 18.8, implying a 0.2% tailwind from a number of expansions over the subsequent 5 years.

Sempra Vitality is projected to return 7.7% yearly by 2027, ensuing from 5% earnings progress, the two.8% beginning yield, and the valuation contribution. Shares earn a maintain score because of anticipated whole returns.

Click on right here to obtain our most up-to-date Positive Evaluation report on Sempra Vitality (preview of web page 1 of three proven under):

Prime Utility Inventory #9: FirstEnergy Corp. (FE)

- 5-year anticipated annual returns: 8.3%

By means of its subsidiaries, FirstEnergy generates, transmits, and distributes electrical energy to clients within the U.S. The corporate contains two segments, Regulated Distribution and Regulated Transmission. FirstEnergy owns and manages hydroelectric, coal-fired, nuclear, and pure fuel amenities and its renewable energy producing operations. The $23 billion firm serves shut to 6 million clients throughout Ohio, Pennsylvania, New Jersey, West Virginia, Maryland, and New York.

FirstEnergy reported third-quarter outcomes on October 25th, 2022. Income improved 12% to $3.5 billion whereas adjusted earnings-per-share of $0.79 in comparison with $0.82 within the prior yr. Greater deliberate bills and share dilution had been the first causes for the decline in earnings.

FirstEnergy has a extra uneven profitability monitor report than most utility names, primarily due to chapter in a former subsidiary and poor investments. That mentioned, the corporate has taken steps to enhance its enterprise and stability sheet, together with decreasing its debt by 30% for the reason that finish of 2021.

As an example how far the corporate has come, administration reaffirmed its earlier forecast of 6% to eight% earnings progress over the medium time period, which is nicely above the compound annual progress charge of two.7% that FirstEnergy had in the course of the earlier decade. We forecast earnings progress of 6.5%.

In tandem with earnings, the dividend has additionally struggled to develop. The truth is, the present annualized dividend of $1.56 continues to be nicely under the $2.20 shareholders obtained in 2012. Nonetheless, the dividend was raised in 2020 and has remained fixed. We imagine that the present dividend is nicely protected given the anticipated payout ratio of 65% for 2022, which might be the bottom determine in additional than a decade. Shares yield 3.9%.

The inventory is buying and selling barely above our goal P/E of 15.5, which might imply that valuation may very well be a 1.5% headwind to annual returns over the subsequent 5 years.

FirstEnergy is anticipated to offer a complete annual return of 8.3% by 2027 because of earnings progress of 6.5% and the beginning yield of three.9%, offset barely by a number of compression. The inventory earns a maintain advice.

Click on right here to obtain our most up-to-date Positive Evaluation report on FirstEnergy Corp. (preview of web page 1 of three proven under):

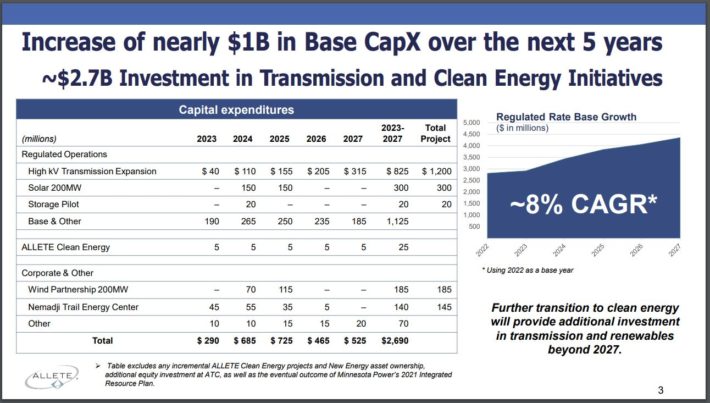

Prime Utility Inventory #8: ALLETE, Inc. (ALE)

- 5-year anticipated annual returns: 9.0%

Allete is an electrical providers firm working primarily within the higher Midwest that additionally invests in transmission infrastructure and different energy-related companies. ALLETE owns Minnesota Energy electrical utility, which gives electrical energy to 145,000 residents in 15 municipalities within the area together with particular giant industrial clients.

Whereas the regulated enterprise is vital to ALLETE, the corporate can be making stable inroads into renewable power. To additional that finish, the corporate acquired New Vitality Fairness, a high photo voltaic developer within the U.S., for $166 million on April 15th, 2022. Different companies embrace BNI Vitality, ALLETE Clear Vitality, Superior Water, and Mild and Energy. Wind tasks ought to have 200 MW in service by 2025, and photo voltaic is anticipated to have at the least 250 MW by the tip of 2026.

ALLETE reported quarterly outcomes on November 9th, 2022.

Supply: Investor Presentation

Earnings-per-share equaled $0.59, which was an 11% enchancment from the prior yr’s determine of $0.53. Administration forecasts that earnings-per-share will develop 16% in 2022.

ALLETE expects its charge base progress can be ~8% yearly over the subsequent half-decade, which ought to result in stable long-term progress. Whereas we share on this enthusiasm, particularly due to the renewable portfolio, we’ve earnings progress estimated at 4% per yr.

Lengthy-term, ALLETE’s dividend progress has been stable as the corporate has a dividend progress streak of 11 years and has maintained its funds to shareholders since 1948. The inventory gives a yield of three.9%.

Shares of ALLETE are buying and selling under our goal P/E/ of 19.5, with potential a number of enlargement including 1.8% to annual returns going ahead.

Subsequently, whole returns come to 9%, stemming from 4% earnings progress, the three.9% beginning yield, and a low single-digit contribution from a valuation. On a pullback, we’d view ALLETE as a purchase.

Click on right here to obtain our most up-to-date Positive Evaluation report on ALLETE, Inc. (preview of web page 1 of three proven under):

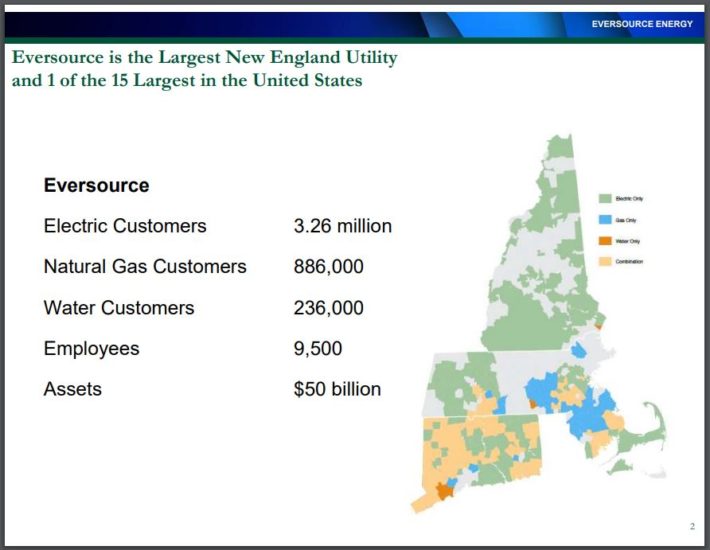

Prime Utility Inventory #7: Eversource Vitality (ES)

- 5-year anticipated annual returns: 9.6%

Subsequent up is Eversource, a diversified holding firm whose subsidiaries present regulated electrical, fuel, and water distribution service within the northeastern U.S. The truth is, the corporate is the most important utility in New England.

Supply: Investor Presentation

Following a number of acquisitions over the past decade, the corporate’s utilities now present providers to greater than 4 million clients. The $29 billion firm modified its title to Eversource from Northeast utilities in 2015.

Eversource reported third-quarter outcomes on November 2nd, 2022. Income surged greater than 32% to $3.22 billion whereas reported earnings of $349.4 million, or $1.00 per share, in comparison with earnings of $283.2 million, or $0.82 per share.

Electrical Transmission earnings had been up virtually 12% to $155.8 million, thanks primarily to larger ranges of funding in Eversource’s electrical transmission system. Electrical Distribution earnings grew 5.4% to $225.1 million because of larger revenues and decrease pensions-related prices.

Eversource has a extremely formidable plan to speculate $18.1 billion in its transmission and distribution tasks by 2026 to be carbon impartial by 2030. The corporate goals so as to add as a lot as 1,800 MW of offshore wind to its portfolio by 2025 by a three way partnership.

We undertaking earnings progress of 5% yearly by 2027, which is near the corporate’s forecast of 5% to 7% progress and the long-term common progress charge of 6%.

Eversource has elevated its dividend for twenty-four years, inserting the corporate on the cusp of accomplishing Dividend Champion standing. With an inexpensive payout ratio of 62%, it’s doubtless that the present yield of three.1% is secure.

Shares are buying and selling at a reduction to our five-year goal P/E of twenty-two, which might result in a valuation tailwind of 1.8% yearly.

In whole, we discover that the return potential for Eversource is 9.6% yearly by 2027 because of earnings progress of 5%, the beginning yield of three.1%, and a small contribution from an increasing a number of. On a pullback, the inventory can be a sexy funding choice.

Click on right here to obtain our most up-to-date Positive Evaluation report on Eversource Vitality (preview of web page 1 of three proven under):

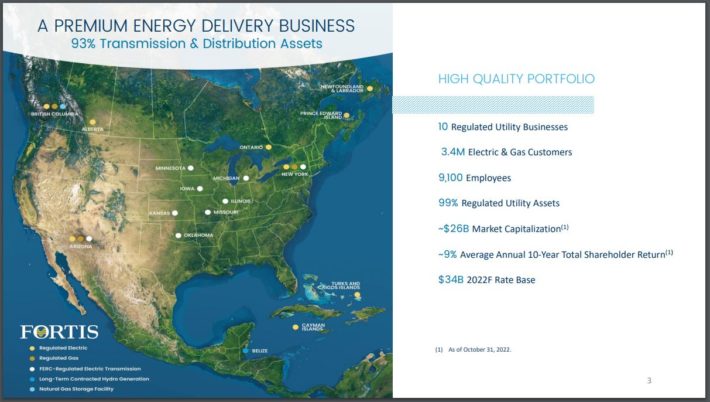

Prime Utility Inventory #6: Fortis Inc. (FTS)

- 5-year anticipated annual returns: 10.7%

The next utility title is Fortis, Canada’s largest publicly traded utility firm. The corporate has a sizeable footprint all through North America.

Supply: Investor Presentation

Whereas Fortis is predicated in Canada, virtually two-thirds of the corporate’s C$58 billion property are positioned within the U.S. A 3rd of property are in Canada, with the remaining positioned within the Caribbean. Of those, 82% of all property are regulated electrical utilities, 17% are regulated fuel, and 1% are nonregulated.

The corporate launched quarterly outcomes on October 28th, 2022. Web earnings of C$341 million had been a 14% improve year-over-year, whereas adjusted earnings-per-share elevated 11%. The corporate invested about C$3 billion, with a said goal of C$4 billion for the yr. We imagine that Fortis is able to 6% earnings progress yearly over the subsequent 5 years.

Fortis’ dividend is topic to forex fluctuations between the U.S. and Canadian greenback, however the firm has a really lengthy dividend progress streak of 49 consecutive years. The inventory gives a beneficiant yield of 4.2%. Fortis has a projected payout ratio of 76% for this yr.

Shares of the corporate are buying and selling just under our goal of 19.8 occasions earnings estimates, which might add 1.2% to annual returns.

Subsequently, Fortis is projected to supply whole annual returns of 10.7% by 2027 because of a mix of 6% earnings progress, a beginning yield of 4.1%, and a small tailwind from a number of expansions. Shares earn a purchase score because of projected returns.

Click on right here to obtain our most up-to-date Positive Evaluation report on Fortis Inc. (preview of web page 1 of three proven under):

Prime Utility Inventory #5: Portland Normal Electrical Firm (POR)

- 5-year anticipated annual returns: 11.2%

Portland Normal Electrical is an electrical utility primarily based in Portland, Oregon. The corporate is on the smaller facet, offering electrical energy to almost 900,000 clients and two million residents in 51 cities.

Supply: Investor Presentation

The client base could be very diversified, with 30% of retail deliveries going to residential clients, 35% to business purchasers, and 26% to industrial purchasers.

Portland Normal Electrical owns or contracts 3.3 gigawatts of power era by fuel (49% of whole), hydro (21%), wind and photo voltaic (19%), and coal (11%). From this breakdown, it’s clear that the corporate is investing closely in renewable power sources. To that finish, Portland Normal Electrical expects to be carbon-free by 2040.

Portland Normal Electrical introduced third-quarter outcomes on October 25th, 2022. Web revenue and earnings-per-share improved by 16% for the interval because of larger power deliveries because of hotter climate and elevated industrial demand.

We undertaking that Portland Normal Electrical will develop earnings-per-share by 6%, which matches the long-term pattern.

Portland Normal Electrical has raised its dividend for 15 consecutive years. And with an anticipated payout ratio of 64% this yr, the inventory’s yield of three.7% appears secure.

Valuation might contribute to whole returns, and shares are buying and selling under our goal P/E of 19. If the inventory reached this stage by 2027, the valuation would add 2% to annual returns.

Annual returns are anticipated to be 11.2% by 2027, pushed by a 6% earnings progress charge, a 3.7% dividend yield, and a slight tailwind from a number of expansions. We charge shares as a purchase.

Click on right here to obtain our most up-to-date Positive Evaluation report on Portland Normal Electrical Firm (preview of web page 1 of three proven under):

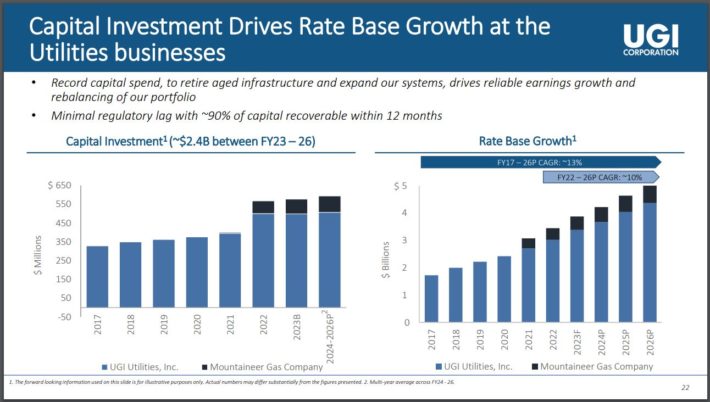

Prime Utility Inventory #4: UGI Company (UGI)

- 5-year anticipated annual returns: 12.6%

UGI is an electrical and fuel utility firm that operates in Pennsylvania, along with a big power distribution enterprise that serves all the U.S. and different elements of the world. The corporate has 4 segments: AmeriGas, UGI Worldwide, Midstream & Advertising and marketing, and UGI Utilities.

UGI reported fourth-quarter outcomes for the fiscal yr 2022 on November 17th, 2022. Adjusted internet revenue of $1.467 billion in contrast favorably to $629 million within the prior yr. Adjusted earnings-per-share fell barely to $2.90 from $2.96.

We discover that UGI can develop earnings-per-share by 7.2% per yr over the medium time period, pushed by funding in its enterprise that might result in a ten% charge base progress from 2022 by 2026.

Supply: Investor Presentation

UGI has paid a dividend yearly since 1885 and has raised its dividend for 35 consecutive years. The payout ratio was 50% for the fiscal yr 2022. The inventory is paying a 3.6% dividend yield in the intervening time.

Shares of the corporate are buying and selling at a reduction to our goal a number of of 15.5, which might add 2.5% to annual returns over the subsequent 5 years.

The mix of seven.2% earnings progress, the beginning yield of three.6%, and a low single-digit tailwind from a number of expansions might result in 12.6% annual returns for the inventory. Shares of UGI obtain a purchase score.

Click on right here to obtain our most up-to-date Positive Evaluation report on UGI Company (preview of web page 1 of three proven under):

Prime Utility Inventory #3: Evergy Inc. (EVRG)

- 5-year anticipated annual returns: 12.7%

Included in 2017, Evergy is an electrical utility holding firm that serves 1.4 million residential clients, 200,000 business clients, and 6,900 industrial clients and municipalities in Kansas and Missouri. The climate tremendously impacts this $13 billion firm as roughly one-third of annual revenues are recorded within the third quarter.

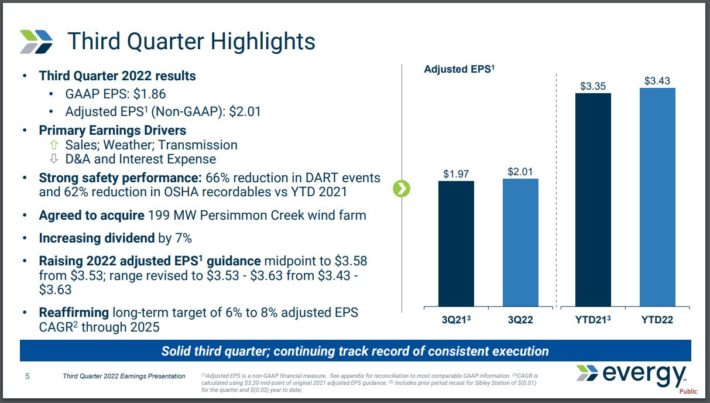

Evergy reported third-quarter outcomes on November 4th, 2022.

Supply: Investor Presentation

Favorable climate and better transmission margin had been solely partially offset by larger curiosity expense and depreciation and helped drive a 2% improve in earnings-per-share to $2.01. Administration narrowed its prior steering for adjusted earnings-per-share to $3.53 to $3.63 from $3.43 to $3.63.

The corporate additionally reiterated its steering for six% to eight% earnings-per-share progress from $3.30 till 2025. We imagine that the midpoint of this vary is feasible as Evergy has a capital allocation clan of just about $11 billion for the 2022 to 2026 interval. The corporate also needs to profit from a discount in bills. For instance, the corporate has already diminished bills by 18% since 2018 and expects one other 8% discount by the tip of 2024.

Evergy has elevated its dividend for 18 consecutive years and has a projected payout ratio of 69% for 2022. Shares yield 4.2%.

The inventory is buying and selling under our truthful worth estimate of 18.5. A number of expansions might add as a lot as 2.3% to annual returns over the subsequent 5 years.

Subsequently, we peg annual returns at 12.7%, stemming from a 7% earnings progress charge, a 4.2% beginning yield, and a small contribution from an increasing a number of.

Click on right here to obtain our most up-to-date Positive Evaluation report on Evergy Inc. (preview of web page 1 of three proven under):

Prime Utility Inventory #2: Dominion Vitality (D)

- 5-year anticipated annual returns: 13.8%

Dominion Vitality is without doubt one of the largest electrical utility corporations within the U.S.

Supply: Investor Presentation

The corporate gives providers to seven million clients in 15 U.S. states, together with Virginia, Ohio, and North and South Carolina. Energy era is fueled by varied sources, together with nuclear, pure fuel, coal, oil, water, wind, and solar.

Dominion Vitality reported third-quarter outcomes on November 4th, 2022. Working income grew 38% to $4.4 billion. Working earnings elevated 2.8% to $944 million, whereas earnings-per-share of $1.11 was flat from the prior yr. Will increase in bills, corresponding to the price of electrical gasoline going up 73%, stored a lid on earnings progress.

The corporate is forecasted to develop earnings-per-share by 6.5% per yr over the medium time period, almost twice the long-term progress charge. We bilevel that is potential because of an aggressive capital funding of $37 billion over the subsequent 4 years that ought to assist develop charge bases. Renewable power, corresponding to wind and photo voltaic tasks, also needs to help outcomes.

After promoting its fuel transmission and storage enterprise to Berkshire Hathaway (BRK.A)(BRK.B) for $9.7 billion, together with the idea of debt, in 2020, Dominion Vitality slashed its dividend by 33%. That mentioned, it seems that the dividend has now been rightsized as we forecast that the corporate may have a payout ratio of 65% in 2022, which might match the earlier yr for the bottom payout ratio in additional than a decade. Shares of Dominion Vitality yield a beneficiant 4.3% even after the dividend reduce.

Dominion Vitality is buying and selling under our five-year goal P/E ratio of 18, which might imply an annual contribution to whole returns of three.8%.

Subsequently, Dominion Vitality is projected to return 13.8% per yr for the subsequent half-decade, pushed by a 6.5% earnings progress charge, the 4.3% beginning yield, and a tailwind from a number of expansions.

Click on right here to obtain our most up-to-date Positive Evaluation report on Dominion Vitality (preview of web page 1 of three proven under):

Prime Utility Inventory #1: Algonquin Energy & Utilities Company (AGN)

- 5-year anticipated annual returns: 20.1%

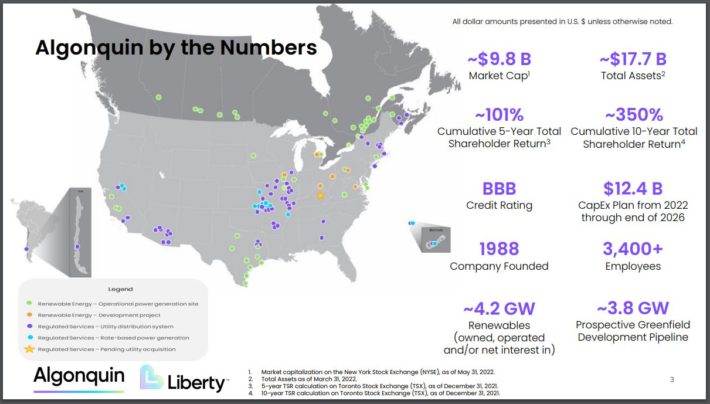

Our high choose amongst electrical utilities is Algonquin, which trades on each the Toronto Inventory Change and New York Inventory Change. The corporate gives providers to a couple of million connections, most of that are positioned within the U.S. and Canada.

Supply: Investor Presentation

The corporate contains two enterprise segments, regulated utilities, which embrace electrical, fuel, and water, and non-regulated renewable power, which incorporates wind, photo voltaic, hydro, and thermal. Algonquin has 4.3 GW of producing capability, 75% of which it goals to realize by renewable power era by 2023. Greater than 80% of the corporate’s renewable and clear power amenities are beneath long-term contracts of almost 12 years with inflation escalators.

Algonquin reported its third-quarter outcomes on November 11th, 2022. Income grew 26% to $666.7 million. Greater rates of interest and delays in development and completion of sure renewable tasks as a result of timing of tax incentives induced adjusted earnings-per-share to say no 27% to $0.11. Nevertheless, adjusted EBITDA, a money movement proxy, improved by 10% to $276.1 million.

As the corporate has used and can doubtless use sooner or later share issuance to develop its enterprise, we imagine that earnings progress of 6.5% may be achieved. This compares to the 11.6% annual progress the corporate noticed for the final 5 years.

The corporate’s dividend does have some fluidity because of forex change, however Algonquin’s dividend progress streak does stand at a decade. Shares are yielding a really excessive 9.7%. We imagine the payout ratio can be 107% for 2022. Normally, a excessive yield and an elevated payout ratio would trigger concern, however the latter has been above 100% for many of the final decade and is especially because of forex.

Algonquin is buying and selling at a big low cost to our truthful worth a number of of 17 occasions earnings. Buyers might see an annual contribution of seven.4% by 2027 if the a number of strategy this goal.

In whole, we forecast that Algonquin will present annual returns of 20.1% because of a mix of 6.5% earnings progress, the 9.7% dividend yield, and a excessive single-digit contribution from a number of expansions.

Click on right here to obtain our most up-to-date Positive Evaluation report on Algonquin Energy & Utilities Company (preview of web page 1 of three proven under):

Remaining Ideas

The necessity for electrical energy isn’t going away considerably as the recognition and progress of electrical automobiles speed up. Combining this want with the everyday makes use of of electrical energy and people utility corporations centered on this space of energy era ought to have additional progress forward because of rising demand.

Utility shares could make vital income-generating positions due to their typically secure enterprise fashions that permit for beneficiant dividend yields.

Whereas not all shares listed on this article have a purchase score, all of them have at the least a excessive single-digit whole return potential and really secure dividend yields. Buyers on the lookout for publicity to the utility sector and dependable revenue might do nicely including these names to their portfolios.

In the event you’re keen to enterprise outdoors of the utility business for funding alternatives, the next Positive Dividend databases are very helpful:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}