Revealed by Josh Arnold on November eleventh, 2022

There are numerous methods to worth shares. There are strategies primarily based on money movement, earnings, dividend yield, income, and the topic of this text, guide worth. The idea of guide worth is sort of easy. The corporate’s property must be valued a minimum of quarterly on the steadiness sheet for buyers to see, and primarily based upon that worth, buyers can then examine the market worth of the inventory to the asset worth on the steadiness sheet.

By doing this, one can see if a inventory trades under its theoretical liquidation worth, which is the web worth of the corporate’s property minus the web worth of its liabilities. For example, if an organization has $2 billion in property and $1 billion in complete liabilities, its guide worth can be $1 billion. That may be the theoretical worth of the corporate if it have been to shut down and liquidate its property. If the inventory had a market cap of $500 million, that might be 50% of the guide worth.

In doing this, we are able to display for shares which can be buying and selling fairly cheaply, as most shares by no means commerce under guide worth, and for people who do, they have a tendency to not keep there for lengthy.

Sectors that are likely to see shares under guide worth are financials, utilities, and sure client staples. It could possibly occur in any sector, however these are those which can be most vulnerable to it.

On this article, we’ll check out 10 shares which can be buying and selling under guide worth and that additionally pay sturdy dividends.

Now we have created a spreadsheet of shares (and carefully associated REITs and MLPs, and so on.) with dividend yields of 5% or extra…

You’ll be able to obtain your free full record of all securities with 5%+ yields (together with essential monetary metrics corresponding to dividend yield and payout ratio) by clicking on the hyperlink under:

Citigroup, Inc. (C)

Our first inventory is Citigroup, one of many main cash middle banks primarily based within the US. Citi had maybe the worst time of the cash middle banks recovering from the monetary disaster, and regardless that the corporate has made monumental progress, it continues to commerce with very low valuations in comparison with its friends. The financial institution provides a full suite of monetary services and products to people, companies, municipalities, and others all around the globe. It has a big bank card enterprise, conventional banking enterprise, in addition to wealth administration, funding banking, and extra.

The corporate was based in 1812, generates $75 billion in annual income, and trades with a market cap of $88 billion.

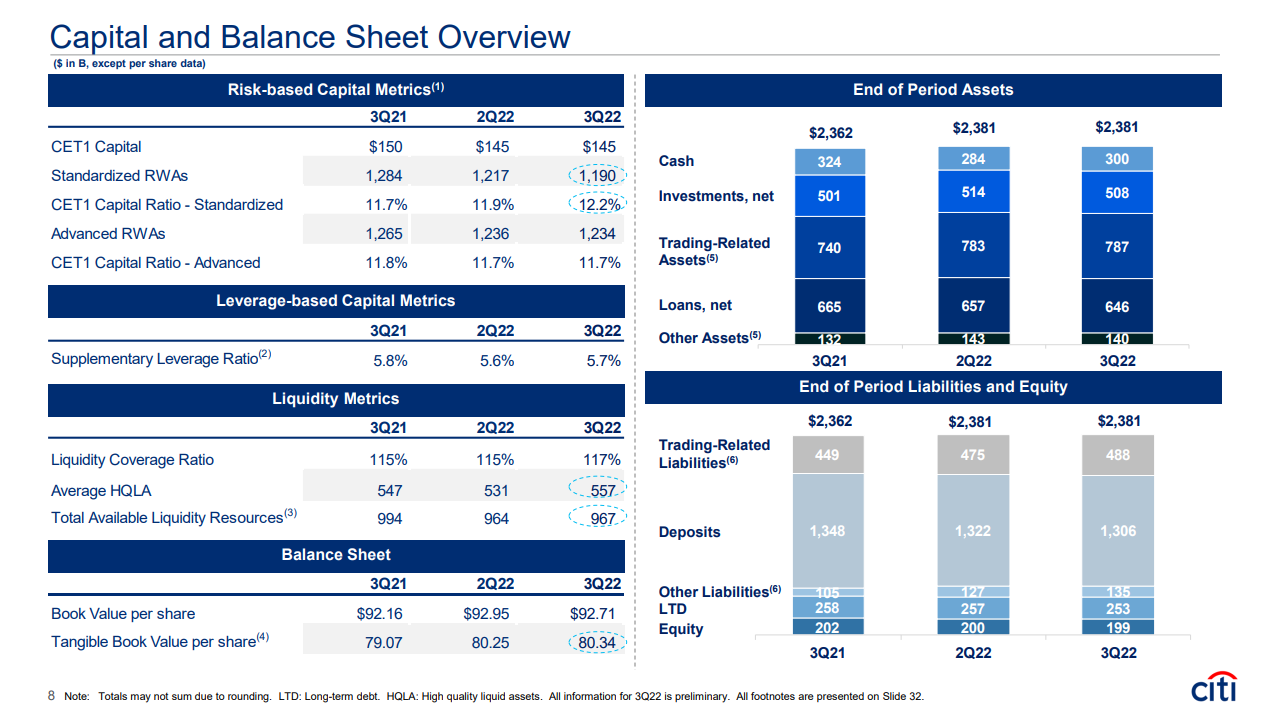

We are able to see Citi’s mixture of property under and the way its guide worth was derived.

Supply: Investor presentation

E-book worth has been fairly regular the previous few quarters at round $93, and it ended the newest quarter there as nicely.

Shares commerce for simply $48 right now, which implies the inventory is buying and selling at simply 52% of guide worth. That’s an especially low worth in opposition to books for any sector and any inventory, so Citi is sort of low-cost.

We see the inventory as buying and selling at simply 63% of honest worth and subsequently see an upside potential of about 10% yearly from the valuation alone.

The inventory additionally sports activities a yield of 4.2%, which is excellent in opposition to the S&P 500 but in addition in opposition to different banks. Since recovering from the monetary disaster, Citi has grow to be a really sturdy dividend inventory.

We’re cautious in regards to the financial institution’s capability to develop from very excessive ranges of earnings within the years to return and assess earnings change at -1% yearly. Nonetheless, with an enormous yield and a ten% tailwind from the valuation, we predict Citi can present complete annual returns of higher than 12% within the years to return.

Click on right here to obtain our most up-to-date Positive Evaluation report on Citigroup, Inc. (preview of web page 1 of three proven under):

British American Tobacco p.l.c. (BTI)

Our subsequent inventory is British American Tobacco, which is a tobacco and nicotine merchandise firm that operates globally. It’s maybe finest recognized for its Fortunate Strike, Newport, and Camel cigarette manufacturers, but it surely additionally provides heated tobacco, nicotine, and vaping merchandise.

The corporate was based in 1902, generates $32 billion in annual income, and trades with a market cap of $87 billion.

The inventory’s guide worth has elevated in latest quarters to almost $40 per share, and given it trades for underneath $38, British American Tobacco’s guide worth sneaks in the appropriate underneath 100%.

We see the inventory priced at 94% of honest worth, which might drive a ~1% tailwind to complete returns within the coming years.

Nonetheless, the inventory pays a staggering 7.3% dividend yield, making it a uncommon firm. Progress is pegged at 3% yearly, so combining these elements offers us anticipated annual returns of simply over 10%.

Click on right here to obtain our most up-to-date Positive Evaluation report on British American Tobacco p.l.c. (preview of web page 1 of three proven under):

Mercedes-Benz Group (MBGAF)

Subsequent up is Mercedes-Benz, the well-known automaker primarily based in Germany. The corporate has undergone transformations over the many years, however right now, it provides Mercedes-branded vehicles, vans, and vans internationally.

The corporate was based in 1886, making it the world’s oldest automaker. It produces about $144 billion in annual income and trades with a market cap of $69 billion.

The inventory ended the newest quarter with a guide worth of about $75 per share, and it trades right now with a price of lower than $65. That places it at about 85% of guide worth and simply 65% of the place we see the honest worth. That would drive a 9%+ tailwind to complete returns within the coming years, considerably including to projected returns.

As well as, the inventory yields greater than 8%, so it’s low-cost and provides an unlimited dividend yield.

We see development at -4% yearly, given 2022’s earnings base is sort of excessive, besides, we imagine the inventory can provide ~11% complete returns within the years to return.

Click on right here to obtain our most up-to-date Positive Evaluation report on Mercedes-Benz Group (preview of web page 1 of three proven under):

The Kraft Heinz Firm (KHC)

Our subsequent inventory is Kraft Heinz, the maker of meals and beverage merchandise which can be on cabinets internationally. Kraft Heinz provides a wide selection of dairy merchandise, condiments and sauces, drinks, meats, dressings, and far more.

The corporate was based in 1869, generates $26 billion in annual income, and trades with a market cap of $46 billion.

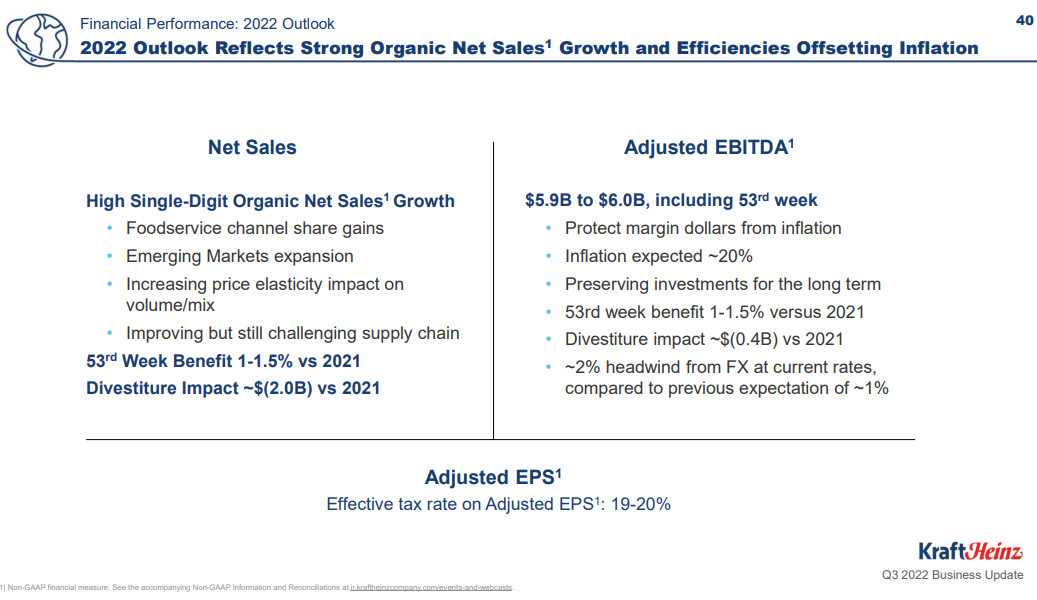

Supply: Investor presentation

Kraft Heinz will not be a high-growth firm, however we are able to see it expects excessive single-digit natural gross sales development this yr, which is excellent for a client staples firm. A lot of that’s pushed by pricing will increase to fight inflation, but it surely additionally stands that its place within the market is such that it may possibly command larger costs.

The inventory ended the newest quarter with a guide worth of simply over $39 per share, and it trades right now at about 97% of that worth. We see the inventory as barely overvalued regardless of it buying and selling slightly below guide worth however anticipate a modest headwind from the valuation.

Shares yield a really good 4.2% right now, so Kraft Heinz is a robust earnings inventory. We challenge development at 2% yearly, so combining all of those elements nets simply over 4% of complete annual returns within the years to return.

Click on right here to obtain our most up-to-date Positive Evaluation report on The Kraft Heinz Firm (preview of web page 1 of three proven under):

Invesco Ltd. (IVZ)

Our subsequent inventory is Invesco, a publicly-owned funding supervisor. The corporate offers funding services and products to establishments, people, funds, and pension funds. Invesco provides all kinds of shares, bonds, and associated funds for patrons to select from.

Invesco was based in 1935, ought to produce about $4.6 billion in income this yr, and has a market cap of $7.2 billion.

The inventory has a present guide worth of about $24 per share, so its price-to-book worth is 78%. We see shares buying and selling at 72% of honest worth right now, which implies we might see a nearly-7% tailwind to complete returns within the years to return from the increasing valuation.

Invesco additionally has a really sturdy yield of 4% right now. We see development at a modest 2%, besides, the mixture of the low valuation and powerful yield has us estimating practically 12% complete annual returns within the years to return.

Click on right here to obtain our most up-to-date Positive Evaluation report on Invesco Ltd. (preview of web page 1 of three proven under):

Manulife Monetary Company (MFC)

Our subsequent inventory is Manulife Monetary, an organization that gives monetary services and products to prospects all around the world. It provides wealth and asset administration providers and insurance coverage and annuities as its major traces of enterprise.

Manulife traces its roots to 1887, produces about $55 billion in annual income, and has a market cap of $31 billion right now.

The inventory ended the newest quarter with a guide worth of about $21 per share, and it trades at simply 82% of that worth right now. We see the inventory as about 14% decrease than honest worth and a commensurate 3% tailwind to complete annual returns consequently.

The present yield is excellent at 6%, which is about 4 instances that of the S&P 500. As well as, we see 5% development within the years forward as Manulife is poised for sturdy income and margin enlargement.

Total, we imagine the inventory might provide 13% complete annual returns within the coming years.

Click on right here to obtain our most up-to-date Positive Evaluation report on Manulife Monetary Company (preview of web page 1 of three proven under):

Hewlett Packard Enterprise Firm (HPE)

Our subsequent inventory is Hewlett Packard Enterprise Firm, a agency that helps corporations seize, analyze, and act upon their knowledge. HPE has prospects all around the world and was spun out of the previous Hewlett-Packard conglomerate in 2016.

The corporate traces its roots to 1939, generates about $28 billion in annual income, and trades with a market cap of simply over $18 billion.

Shares ended the final quarter with a guide worth of about $16, and shares commerce about 7% under that right now. We imagine the inventory is pretty valued on the present worth, so we see basically no affect on returns from the valuation.

HPE pays a dividend price 3.2% right now, about double the S&P 500. Additional, we see 3% annual development, serving to to drive complete annual returns of simply over 6%.

Click on right here to obtain our most up-to-date Positive Evaluation report on Hewlett Packard Enterprise Firm (preview of web page 1 of three proven under):

Molson Coors Beverage Firm (TAP)

Subsequent up is Molson Coors, a beverage firm that manufactures, sells, and distributes beer and different malt drinks all through the world. The corporate’s portfolio focuses on beer, together with its namesake Molson and Coors manufacturers, however has lately diversified some.

Molson Coors traces its roots to 1774, generates virtually $11 billion in annual income, and has a market cap of the identical.

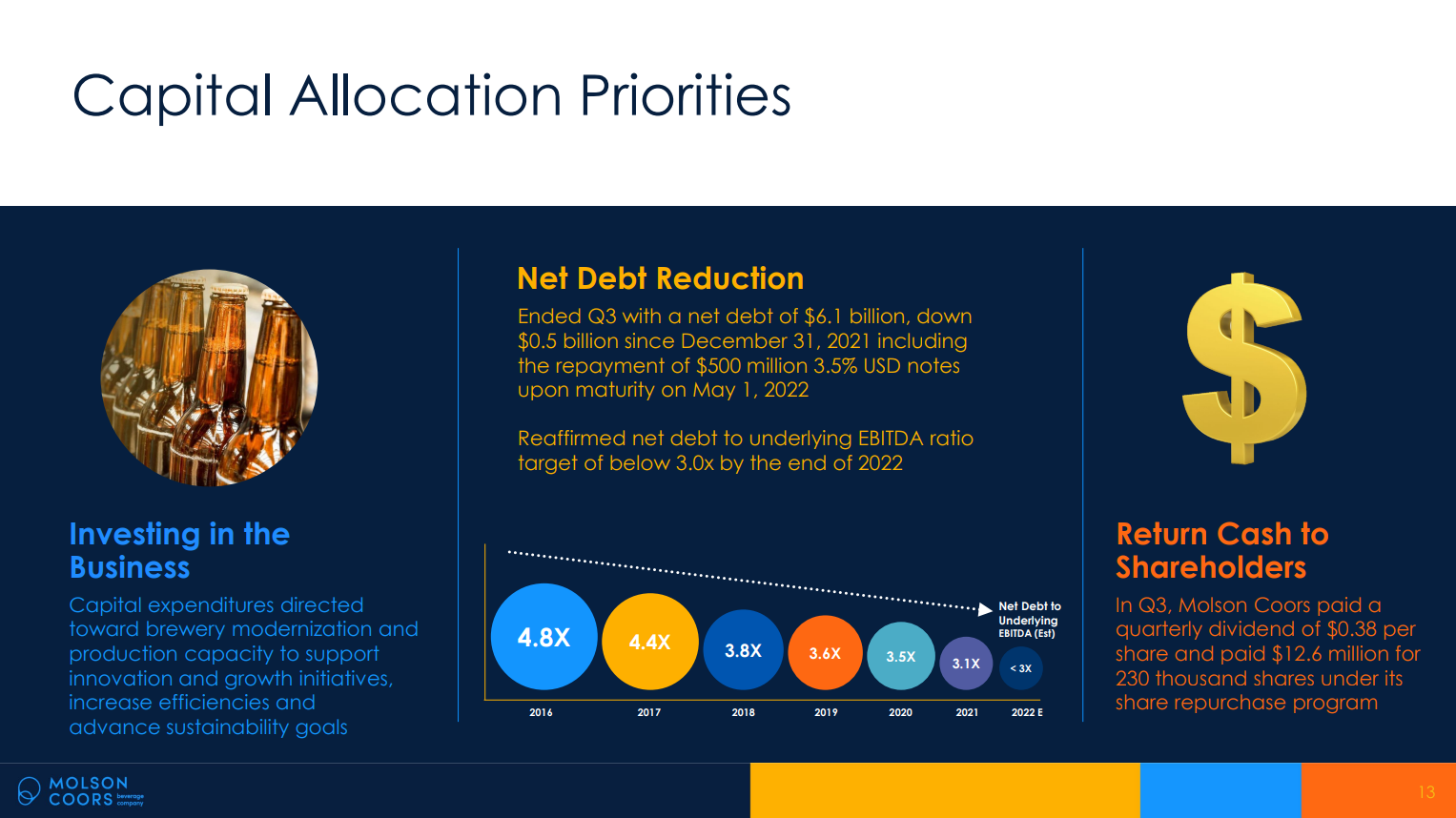

Supply: Investor presentation

This slide highlights the corporate’s dedication to shareholders in that it has three capital allocation priorities. First, it invests within the enterprise. Second, it seeks to scale back debt, because it has carried out for years. And third, it returns money to shareholders through dividends and buybacks. All are related to the guide worth dialogue in a method or one other.

The inventory’s guide worth ended the newest quarter at $61, and it trades for a reduction of about 15% to that worth right now. We see the inventory as about 7% undervalued, driving a possible tailwind of simply over 1%.

The dividend yield is 3% right now as nicely, which means that the inventory is robust from an earnings perspective regardless of the dividend not being the highest capital allocation precedence. Progress might are available in at 4% yearly, and we see 8% anticipated annual returns to shareholders.

Click on right here to obtain our most up-to-date Positive Evaluation report on Molson Coors Beverage Firm (preview of web page 1 of three proven under):

Fresenius Medical Care (FMS)

Fresenius is up subsequent, an organization that gives dialysis care, primarily in Germany and the US. It provides a community of virtually 4,200 clinics internationally, making it one of many largest corporations of its sort.

Fresenius was based in 1996, generates about $19.5 billion in annual income, and trades with a market cap of slightly below $11 billion.

The inventory ended the newest quarter with a guide worth close to $41, however the inventory trades for lower than $15 right now. That places it at lower than 40% of guide worth, and we see it as about 30% undervalued. That would drive a 7%+ tailwind to complete returns within the years to return.

The yield can be wonderful at practically 5%, and we see a 3% annual development for the inventory. Combining these elements means we challenge ~14% of complete annual returns to shareholders within the coming years.

Click on right here to obtain our most up-to-date Positive Evaluation report on Fresenius Medical Care (preview of web page 1 of three proven under):

WestRock Firm (WRK)

Our closing inventory is WestRock, a packaging options firm that operates globally. The corporate makes all kinds of packing containers, linerboards, tubing, and different kinds of packaging for an enormous array of consumers.

The corporate produces about $22 billion in annual income and has a market cap of $8.8 billion.

Shares ended the final quarter at a guide worth of $45 per share, about 25% larger than the present share worth. We see the inventory as greater than 30% undervalued at current, with that serving to to drive a possible ~8% tailwind to complete returns.

The dividend yield is good at 3%, however we see development as modest at a possible 2% per yr. All instructed, largely as a result of valuation, we challenge higher than 12% complete annual returns within the coming years.

Click on right here to obtain our most up-to-date Positive Evaluation report on WestRock Firm (preview of web page 1 of three proven under):

Ultimate Ideas

Whereas there’s all kinds of how to worth shares, a method we like is to contemplate the corporate’s market worth in opposition to its guide worth. This helps guard in opposition to overpaying for costly shares, and above, we famous ten shares we like underneath guide worth right now that additionally pay sturdy dividends.

Every has its distinctive mixture of worth, dividend yield, and development; most are buy-rated primarily based on complete return potential.

The next articles include shares with very lengthy dividend or company histories, ripe for choice for dividend development buyers:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}