anyaberkut

Co-produced with Treading Softly.

The older I get, the extra I notice simply how costly life might be.

Whenever you’re youthful, your first paycheck makes you’re feeling like a newly minted member of the higher class of society. But the truth is that your fast-food paycheck is nothing when it stacks up towards the realities of maturity bills.

The older we get, the costlier life can develop into as we purchase a home or pay lease, increase kids, and pay for our payments. When individuals are of their 20s and 30s, their revenue will rise quickly, however so too does the bills tied to their life as they get established and have a household.

Many do not begin considering of their retirement plans till they hit their 40s, and retirement is just 15 years away. Now they really feel like they’re within the 4th quarter, and the opposite workforce has been getting touchdowns whereas they have been altering diapers.

The basic components for retirement is to carry a portfolio of fifty% equities, just like the S&P 500 (SP500), and 50% bonds, just like the Vanguard Whole Bond Market ETF (BND). As soon as you have constructed that portfolio, you’d take 4% out yearly to reside off of, adjusting for inflation, and also you’d pray your portfolio makes it your entire size of your retirement.

This works nice as long as you rigidly observe it and time your retirement successfully. The built-in assumption is that the market would return 7% yearly, and inflation would solely quantity to three%. Thus, in case you take out 4%, you can repeat this course of indefinitely.

As you understand, inflation has not been a gradual 3%, and not too long ago it is spiked strongly whereas the market posted unfavorable returns. In these cases, you will be eroding the worth of your general portfolio to reside, leaving much less beginning cash to cowl your subsequent withdrawal the following 12 months.

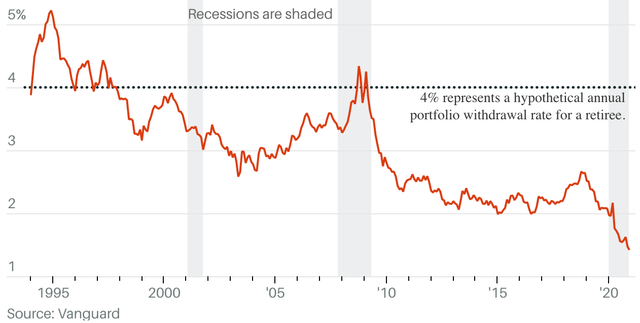

In latest occasions, the power of a 50/50 portfolio to satisfy your wants has declined quickly. As soon as yielding over 5%, a 50/50 fairness and bond portfolio now’s yielding lower than 2%. (Supply: irrelevantinvestor.com.)

irrelevantinvestor.com

So what can an individual do, if they need an awesome retirement with out having to emphasize and fear over their monetary stability?

Reside off of dividends. Sure, you heard that proper. It is completely attainable and believable to do this!

Dividends present a path to take pleasure in long-term revenue which covers your monetary wants with out having to resort to asset gross sales. There was a time frame when folks needed to go away property to their kids, which was one of many key ways in which generational wealth was created, by passing it downward. But, because the 4% rule turned common, increasingly folks have been pressured into an orderly dismantling of their property as a substitute of leaving an inheritance to folks they love or causes they assist.

Dividends Are Changing into Extra Obligatory For Lengthy-Time period Revenue

We have survived a very long time interval the place we lived in a zero-interest-rate surroundings. This led to rock-bottom CD rates of interest, low municipal bond charges, and low revenue from conventional secure haven investments.

We lived in a spending-benefitting surroundings. You would get cash from a financial institution very cheaply at low-interest charges, which meant your financial institution accounts and different debt merchandise provided a pittance of revenue. But, when the 4% rule was popularized, we lived in a saving-friendly surroundings. Rates of interest have been increased, and thus banks paid high greenback to your life financial savings to lend it out and reap main earnings from it.

Proper now, we discover ourselves someplace within the center:

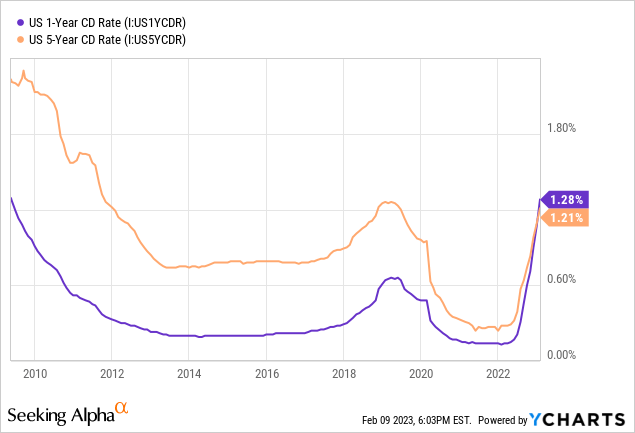

Are CD charges climbing? Sure. They moved from beneath half a % to round 1.28% nationally. It is very important observe that 1-year CD charges are increased than 5-year charges. This implies banks are considering charges will drop throughout the subsequent 5 years and are unwilling to pay you extra for holding your cash longer than a short-term CD.

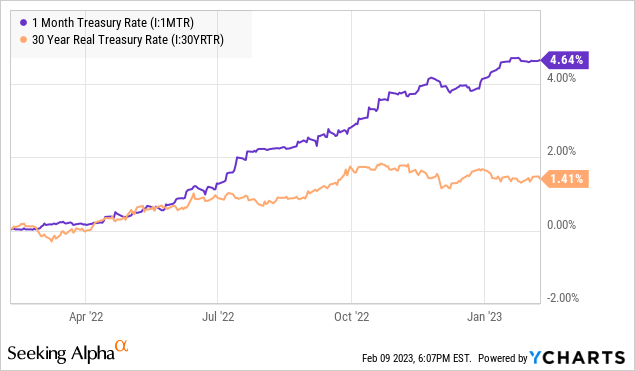

Likewise, Treasury yields present an identical dichotomy, though it’s bigger as a result of time distinction – 1 month vs. 30 years:

What does this imply? Nicely, similar to beforehand, counting on yields from bonds, CDs, and Treasury Notes means you’ll probably see declining revenue and yields as we glance additional into the long run. Banks and institutional buyers count on cheaper {dollars} sooner or later, so they’re unwilling to pony up huge bucks to your cash now.

To create a livable yield for the long run, that you must transfer deeper into the market and now not stay on the sidelines hiding in these different choices. In any other case, your revenue generated on property will likely be subsequent to nil as we glance into the long run. A excessive yield on a 1-year CD solely kicks the can down the street a 12 months, that is not a long-term sustainable selection.

As increasingly retirees notice their financial savings aren’t assembly their wants, and the need to go away an inheritance behind means they do not need to wind down their property to outlive, they’re pushed towards discovering revenue elsewhere.

Dwelling on Dividends Means Extra Revenue From Much less Capital

Whenever you examine a portfolio withdrawing 4% or a dividend revenue portfolio, you’ll be able to readily make the equal revenue on fewer preliminary property, or generate way more revenue from the equal asset base.

The Excessive Dividend Alternatives Mannequin Portfolio goals to generate a 9% yield from its array of holdings. Meaning a $1 million portfolio would pay out $90,000 or over double what a $1 million portfolio would offer utilizing the 4% withdrawal rule.

Or, alternatively, you would generate $40,000 from $445,000 – lower than half of your millionaire buddy.

This enables your retirement dream to be way more readily achievable.

The potential for extra revenue from safer locations abounds, you simply have to know the place to search for these alternatives.

There are expert people that go catfishing with simply their naked arms. They will stroll right into a river or stream and pull out a monster catfish from a gap. That does not imply you’ll be able to stroll to any river and shove your hand in a gap and yank out success. It takes ability, information, and endurance to develop these abilities.

Likewise, discovering dependable revenue available in the market means understanding the place the holes are and reaching in to drag out glorious alternatives to carry for many years to come back.

Buyers, when considering of dividends, will usually flock to the previous trustworthy like Coca-Cola (KO) or PepsiCo (PEP). But I’ve discovered, in case you actually need to generate excessive ranges of revenue from the inventory market, that you must transfer previous the overpopularized names and go into the place cash is actually being made within the financial system.

I purchase these corporations concerned in preserving the financial system transferring, preserving fuel at your native fuel station, or preserving your lights on. These alternatives present increased ranges of revenue and are much less identified.

Dreamstime

Your Distinctive Targets Met by a Uniform Resolution

Every of us is exclusive. No two folks share an identical backgrounds, life tales, or private pursuits. You may meet your doppelganger, however even whilst you look comparable, you will not be copy/paste people.

The fixed between all of our lives and selections is that cash is required. Each one among us has payments to pay and issues we should afford. If you wish to journey, you will want cash. If you wish to sit back at residence and watch the sundown, you will be paying bills associated to that residence and property.

That is the fantastic thing about revenue investing. When you and I are completely distinctive and completely different from each other, the strategy is uniform. Members of my funding neighborhood and different revenue buyers all search the identical dependable revenue from regular and powerful sources. We use debt devices, dividend-paying corporations, and most well-liked securities to attain our targets.

Dividends are the lifeblood of tens of millions of retirees’ revenue money movement. When you may withdraw 4% yearly and slowly dismantle your property, one other technique is to speculate for dividends and revel in increased revenue from dependable sources.

When is the perfect time to get began? Yesterday was the perfect time, and now’s the second-best time. Get your portfolio into income-producing investments, and you will come to see why so many retirees cease stressing about market actions and as a substitute unlock extra time to discover their favourite hobbies.

We’re all on our personal distinctive life journeys, however you needn’t reinvent the wheel earlier than you drive your automobile. Likewise, you needn’t reinvent investing to unlock success available in the market. Let dividends pay your means. I am unable to wait to see your accomplishments!