")

SimonSkafar/E+ through Getty Photographs

Buyers rely on the administration groups that run the businesses that they put money into to behave in ways in which create essentially the most worth on the finish of the day. Once in a while, there is usually a disconnect between what administration thinks is finest and with the market believes to be finest. When these opinions diverge, you’ll be able to see a big motion in share worth. The most recent instance of this was seen on October sixteenth when shares of Vista Outside (NYSE:VSTO) plunged, closing down almost 24%. This motion got here in response to Vista Outside asserting a change in its strategic plan. Beforehand, administration anticipated to separate up the corporate into two separate corporations by the use of a by-product, with the Sporting Merchandise operations serving as one enterprise and the Outside Merchandise serving as one other.

Sadly for shareholders, this all modified on October sixteenth. Administration introduced that the corporate could be promoting off its Sporting Merchandise enterprise in an all-cash transaction whereas the Outside Merchandise agency could be all that is left for shareholders to personal a chunk of. As you will notice, the precise transaction is a little more sophisticated than that. However with the prospect of a doubtlessly important tax invoice and considerations over the well being of the surviving firm, the market didn’t take too kindly to this maneuver.

It’s price noting that this is not my first rodeo with Vista Outside. I did write in regards to the firm beforehand, the final time in 2021. In that article, I rated the corporate a purchase as a result of it had began exhibiting good progress. Sadly, due largely to this latest plunge, shares at the moment are down 38.3% in comparison with the 6.8% decline seen by the S&P 500 over the identical window of time. Though gross sales continued to rise from 2021 to 2022, earnings dropped, falling to a lack of $9.7 million in comparison with the $433.2 million achieve seen the 12 months prior. Even when we take a look at working earnings with out the agency’s giant enchancment, margin contraction took its earnings down from $646.2 million in 2021 to $482.2 million final 12 months. In actual fact, it is this sort of weak spot that nearly definitely inspired administration to discover strategic alternate options.

An abrupt change

Again in Might of 2022, the administration workforce at Vista Outside introduced their plans to separate the 2 separate firms into separate publicly traded enterprises. Up till October sixteenth, there was no indication that this plan would change. However on that date, administration introduced that they had been promoting off the Sporting Merchandise operation for $1.91 billion in money. Though that is being positioned as a sale publicly, the transaction is a little more complicated than that. Technically, Vista Outside will break up off its Outside Merchandise enterprise from what’s presently the mother or father firm. They are going to then merge that with a subsidiary of the acquirer, Czechoslovak Group, with the money from that transaction being mixed with the shares of the Outside Merchandise operation, and being hand it over to the present shareholders of Vista Outside.

| Standalone Outside Merchandise Firm (Revelyst) | Monetary Information |

| Debt | $986.01 |

| Much less: Present Money | $63.16 |

| Much less: Buy Money | $1,910.00 |

| Internet Debt: | -$987.16 |

| Market Cap | $1,446.00 |

| Enterprise Worth | $458.84 |

In keeping with administration, this Outside Merchandise enterprise might be rebranded as Revelyst. The Sporting Merchandise operation could be unloaded on a money free and debt free foundation. That implies that the $986 million in debt that Vista Outside presently owns might be stored by the surviving enterprise. However once you add within the $1.91 billion in money and the $63.2 million in money that the enterprise presently has on its books, you see that debt, on a internet foundation, has been worn out. $750 million of this money might be allotted towards shareholders of Vista Outside (or, technically, the brand new Revelyst) with at the least a few of that going to pay taxes for the reason that transaction will represent A taxable sale of the stockholders in Vista Outside for the shares of the brand new firm they’re receiving and its money consideration.

I can’t opine on the tax state of affairs myself since that’s not my space of experience and since every particular person’s tax state of affairs differs. However it’s secure to imagine that it is this tax image that has shareholders indignant. If there’s a optimistic facet to this, it is that the tax therapy of this transaction will enhance the image for Revelyst, bringing its tax invoice all the way down to solely $50 million in comparison with the $380 million administration mentioned that an asset sale outright would end in. If this maneuver by itself is just not irritating sufficient for shareholders, there’s additionally the truth that administration additionally determined to let traders know of a moderately important revision in monetary efficiency for the 2024 fiscal 12 months.

Creator – Vista Outside

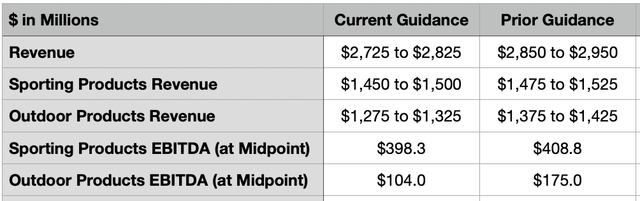

Beforehand, administration had forecasted income for the 12 months of between $2.85 billion and $2.95 billion. That has now been diminished to between $2.725 billion and $2.825 billion. Weak market situations can actually be blamed for this. However it’s additionally necessary to level out that this weak spot is generally affecting the a part of the corporate that shareholders might be left with. Prior steerage for the Sporting Merchandise a part of the corporate had been for income of between $1.475 billion and $1.525 billion. That has been diminished solely modestly by $25 million on each ends of the vary. By comparability, the Outside Merchandise enterprise was beforehand anticipated to generate income of between $1.375 billion and $1.425 billion. That has now been diminished by $100 million on the highest and backside traces.

Comparable weak spot is now forecasted on the underside line as properly. As an illustration, utilizing the midpoint of steerage for the EBITDA margin, the Sporting Merchandise enterprise ought to now generate round $398.3 million of EBITDA for its 2024 fiscal 12 months. That is down solely barely from the $408.8 million beforehand forecasted. By comparability, the Outside Merchandise firm ought to go from producing EBITDA of $175 million to solely $104 million. Administration nonetheless maintains, at the least, that the long-term outlook for the Outside Merchandise enterprise is vastly superior to the outlook for the Sporting Merchandise enterprise. The latter of those was estimated to have a market alternative for traders of $10 billion or extra. However the former has been forecasted to have a market alternative exceeding $130 billion, with $30 billion of this being for the core market within the US alone.

Creator

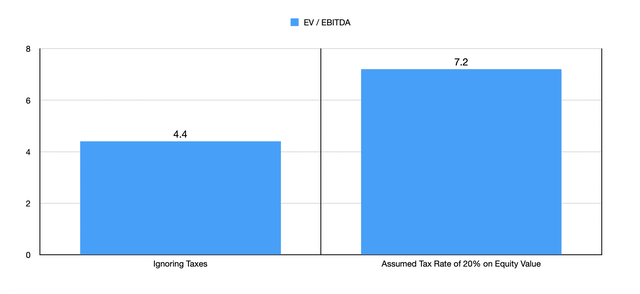

Though this drop is undeniably painful, it does now create what could possibly be a moderately fascinating alternative for traders. Even when we assume that monetary efficiency is not going to enhance past what the Outside Merchandise operation ought to generate for 2024, the corporate is now buying and selling at a ahead EV to EBITDA a number of of 4.4. After all, we do must issue within the tax facet to this. If, as an illustration, we assume a 20% tax charge on the present market capitalization of Vista Outside, this could end result within the EV to EBITDA a number of of the corporate being fairly a bit larger at 7.2. However within the desk under, you’ll be able to see how 5 related corporations are priced. With out this tax state of affairs factored in, the Outside Merchandise enterprise is the most affordable of the group. And with it factored in, three of the 5 firms are nonetheless costlier than it.

| Firm | EV / EBITDA |

| Vista Outside | 4.4 to 7.2 |

| Topgolf Callaway Manufacturers (MODG) | 8.4 |

| Sturm Ruger & Co. (RGR) | 7.7 |

| Smith & Wesson Manufacturers (SWBI) | 7.6 |

| Malibu Boats (MBUU) | 5.4 |

| Dick’s Sporting Items (DKS) | 5.1 |

Takeaway

If I had been a shareholder of Vista Outside proper now, I might be very indignant. This maneuver doesn’t appear optimum to me and it’s clear that market contributors had been each stunned and annoyed by it. It leaves shareholders in uncharted territory and may need been, on the finish of the day, an inferior technique to different strategic transactions and even maintaining the corporate collectively. Now that the inventory has fallen, nevertheless, I might make the case that shares are positively low-cost sufficient to warrant consideration. However I may perceive why traders would have a difficulty trusting administration after such a disastrous downturn.