")

Bruce Bennett

There’s nothing to not like about Verizon (NYSE:VZ) proper now. The corporate reported first rate earnings outcomes for Q3, its enterprise seems to be recovering, and its inventory is an honest dividend and worth play with a modest upside. Whereas Verizon’s enterprise may very well be negatively affected by the worsening of the macroeconomic atmosphere subsequent 12 months if we enter a recession, there are nonetheless causes to imagine that its shares stay a horny funding on the present worth.

Restoration Is On The Manner

Just a few weeks in the past, Verizon reported its Q3 earnings outcomes which confirmed that it generated $33.33 billion in revenues, down 2.7% Y/Y however in keeping with the estimates, whereas its non-GAAP EPS was $1.22, above the expectations by $0.04. The decline in revenues is attributed principally to the decline of postpaid upgrades which resulted in a 12% Y/Y income decline within the wi-fi gear enterprise. Regardless of this, Verizon managed to generate $14.6 billion in FCF YTD, which is already above its 2022 ranges.

Going ahead, there are causes to imagine that Verizon will have the ability to enhance its total enterprise and develop its revenues within the foreseeable future. That is principally because of the truth that the corporate has an honest momentum going for it. Its broadband enterprise in Q3 had 434,000 internet additions and recorded a fourth quarter of over 400,000 internet provides in a row. On the similar time, regardless of the $10 improve for brand spanking new bundled clients, Verizon delivered 384,000 mounted wi-fi entry internet additions, whereas its bundled providing Fios managed to ship 72,000 web internet provides, up 20% Y/Y. The corporate now has 10.3 million broadband subscribers, up 21% Y/Y, and it seems that it will stay the case within the following quarters.

Let’s additionally not neglect about the truth that with the rising inflation, wi-fi costs have been going up and elevated by 5% over the past 12 months, and but it did not cease Verizon from bettering its person metrics in latest months. After launching myPlan earlier this 12 months and later the Final Limitless tier for it, the corporate was even in a position to improve its common income per account by 4.5% Y/Y in Q3 to $133.47, whereas its churn fee stood at solely 0.85%. Contemplating that we’re doubtless seeing the underside for pay as you go volumes, it might be secure to say that Verizon will have the ability to retain its momentum in This fall partly because of the providing of its flagship plans to the shoppers of the lately launched iPhone 15 which have already lifted the smartphone market.

What’s extra is that because the macroeconomic atmosphere improves, there is a risk that the corporate’s income progress will speed up within the foreseeable future. Contemplating that the inflation stalled M/M in October after the 2 months of M/M will increase, it is secure to say that we’re within the disinflation mode which bodes nicely for corporations like Verizon. The sooner rate-hiking cycle actually negatively affected Verizon’s potential to exceed expectations, particularly because it was in the course of growing its capital expenditures into 5G to stay aggressive. As capital expenditures lower, whereas the charges may very well be lower subsequent 12 months, Verizon has a chance to retain its momentum not solely in This fall however in 2024 as nicely.

The road already believes that that is precisely going to be the case because it expects a return to the Y/Y income progress beginning subsequent 12 months. Verizon’s administration itself sounded optimistic on the newest convention name and elevated its FCF steerage for FY23 to above $18 billion, up from the earlier estimates of $17 billion.

Is The Inventory A Purchase?

With such a constructive outlook for the 12 months, it is secure to say that Verizon’s present debt scenario is greater than manageable whereas its dividends are comparatively secure. Despite the fact that the corporate had solely $4.3 billion in money reserves and $137.2 billion in long-term debt on the finish of Q3, it has an curiosity protection ratio of over 5x, which makes it straightforward for it to proceed to cowl curiosity bills and pay dividends on the similar time. Contemplating the consistency at which Verizon has been rewarding its shareholders even through the troubled occasions, it is smart to say that the corporate’s inventory is a good dividend play in the mean time, particularly because it has a ahead yield of ~7%.

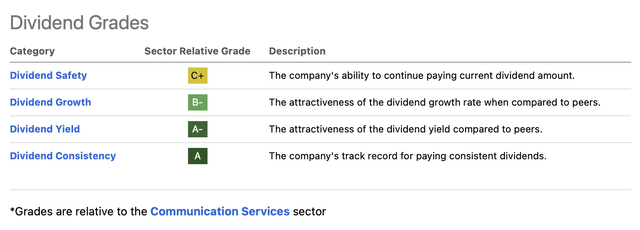

Verizon’s Dividend Grades (Searching for Alpha)

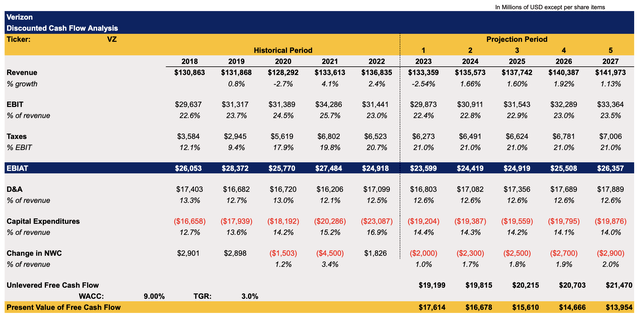

On prime of that, there are additionally causes to imagine that Verizon’s inventory is undervalued and provides an honest upside on the present ranges. My DCF mannequin beneath assumes that the top-line progress will return in FY24 and past, which aligns with the present sentiment on the road. The EBIT as a proportion of income is anticipated to be within the vary of twenty-two.4% to 23.5%, which intently mirrors charges from the earlier years. The tax fee stands at 21%, which is at present the usual company tax fee in the US. The capital expenditures assumptions for FY23 align with the administration’s forecast for the 12 months. On the similar time, the mannequin assumes a deceleration of capital expenditures as a proportion of income in FY24 and past for the reason that preliminary heavy funding into the 5G infrastructure has already taken place lately. The WACC within the mannequin stands at 9%, whereas the terminal progress fee is 3%.

Verizon’s DCF Mannequin (Historic Knowledge: Searching for Alpha, Assumptions: Writer)

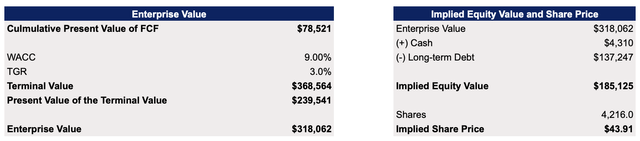

This mannequin reveals that Verizon’s enterprise worth is $318 billion, whereas its truthful worth is $43.91 per share, which represents an upside of ~20% from the present market worth. Contemplating this, it is secure to say that Verizon is an honest dividend and worth inventory on the present worth.

Verizon’s DCF Mannequin (Historic Knowledge: Searching for Alpha, Assumptions: Writer)

The Solely Threat That Actually Issues

It is secure to imagine that the one factor that would undermine Verizon’s restoration is the worsening of the macroeconomic atmosphere. The corporate operates a predictable enterprise that principally grows through the good occasions and principally declines in occasions of uncertainty.

That is why there is a danger that if the macro circumstances deteriorate and affect shoppers and companies, Verizon’s restoration may very well be in jeopardy, and the corporate might begin shedding its broadband subscribers. Despite the fact that the inflation information for October shocked many, there is a danger that the inflation itself will not fall to the two% stage, which the Federal Reserve targets, anytime quickly and will result in the extension of the present hawkish financial coverage by the regulators for an extended interval. There’s already a sign that shopper buying energy is perhaps declining because of inflation forward of the vacation season.

Contemplating that an organization like Verizon is anticipated to develop solely at 1% to 2% a 12 months, there’s at all times a danger that any small worsening of the macroeconomic circumstances might simply undermine its progress story. That is one thing that potential or present buyers have to continuously remember, because it’s the one main danger that really issues at this stage.

Aside from that, there’s nothing to not like about Verizon’s enterprise and if the macro dangers will not totally materialize – then it is unlikely that one thing would have the ability to undermine its restoration or the funding attractiveness of its shares.