")

Anatoly Morozov/iStock through Getty Photos

Funding thesis

The shares in Toyo Gosei (OTCPK:TYGIF) have corrected 53% YTD, and we imagine key negatives over price inflation and FX dangers have been priced in. Regardless of the corporate’s place as a provider of key chemical substances to the semiconductor trade, we imagine it isn’t value investing in given the restricted upside from a money burn profile and falling profitability which might result in detrimental development YoY. We’re impartial on the shares.

Fast primer

Established in 1954, Toyo Gosei is a Japanese specialty chemical producer working two key enterprise segments. The primary is photosensitive supplies utilized in semiconductor manufacturing (for each logic and reminiscence chips) which made up over 60% of FY3/2022 gross sales. The second is chemical substances to be used in prescribed drugs, fragrances, paints, and solvents and their storage administration and warehousing. The present CEO Yujin Kimura is a member of the family of the founder and former Chairman Masateru Kimura.

The corporate’s largest buyer is Shin-Etsu Chemical (OTCPK:SHECY), Japan’s largest chemical firm and the worldwide main producer of PVC by quantity. Shin-Etsu Chemical made up 13.6% (web page 12) of complete gross sales in FY3/2022.

The corporate will announce Q2 FY3/2023 outcomes on November ninth, 2022.

Key financials together with consensus forecasts

Key financials together with consensus forecasts (Firm, Refinitiv)

Our targets

Toyo Gosei hit the headlines with Kamala Harris’s go to to Japan in September 2022, who hosted a roundtable assembly with semiconductor provide chain corporations. Though not at all a significant heavyweight within the sector, Toyo Gosei has a task in offering photosensitive materials to be used in semiconductor lithography.

On this piece, we wish to assess the outlook for earnings given the key modifications in FX charges, and inflationary pressures affecting uncooked materials and freight prices.

An uphill climb

While the corporate had anticipated the depreciation of the Japanese yen versus the US greenback in FY3/2023, no one might have anticipated its precise fast price of decline. Toyo Gosei had anticipated an FY common FX price of JPY125 to the US greenback for the present monetary 12 months, however it had already reached JPY136 in Q1 FY3/2023 and is presently buying and selling at round JPY147 – a depreciation of 31% YoY.

While this may end in pushing yen-denominated gross sales strongly YoY, it was already noticeable in Q1 FY3/2023 (web page 4) that prices have been rising. Uncooked supplies, gasoline, and freight prices rose YoY dampening margins, along with rising working prices as the corporate spent on Capex and R&D. While buying and selling appeared consistent with interim firm steering, we see the next challenges forward.

Firstly, the power of the greenback will imply higher-than-expected prices. There’s room for Toyo Gosei to lift costs, however we imagine there can be restricted promoting energy as end-user demand begins to dry up for flat panel show supplies, in addition to extra notably within the reminiscence market with stock changes presently underway lately highlighted by Micron (MU), Western Digital (WDC) and Samsung Electronics (OTCPK:SSNLF). The logic market appears to be like comparatively more healthy, however the general outlook for the corporate’s photosensitive chemical enterprise is detrimental.

Prices may even play a component in pushing down profitability within the chemical phase, which is reliant on demand from autos, cosmetics, and high-purity solvents for electronics, that are all experiencing a downturn in client sentiment.

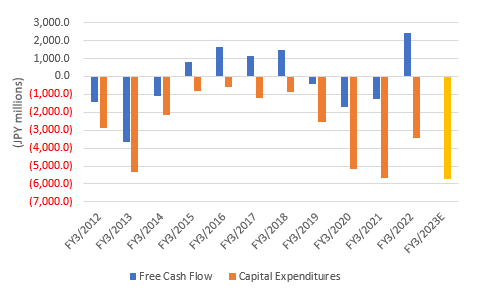

Secondly, the corporate introduced a medium-term plan in FY3/2022, which highlighted a dedication to funding to boost its infrastructure and lift manufacturing capability. Though these ought to have longer-term advantages, within the quick to medium time period it seems to be an ideal storm whereby profitability is pushed down with rising depreciation, while free money move is punished as Capex ranges are anticipated to stay traditionally elevated with a view to increase capability. The corporate’s monitor document of producing free money move shouldn’t be precisely secure, and consequently, we anticipate the corporate to be burning money in FY3/2023 and FY3/2024 except plans are revised – a tall order given the long-term contract nature of those build-outs.

Free money move pattern (in blue), with deliberate Capex for FY3/2023 (in yellow)

Free money move pattern, with deliberate Capex for FY3/2023 (Firm)

Consensus forecasts look too bullish

Regardless of these main challenges that lay forward, consensus forecasts seem very optimistic with continued margin enlargement mixed with strengthening free money move technology (please see desk above in Key Financials). We can’t foresee such occasions occurring, given the price pressures and waning underlying demand. What seems comparatively plausible is the dividend forecast for FY3/2023 the place the corporate has already deliberate JPY40 per share. Nonetheless, given the present enterprise atmosphere, we imagine this can be at greatest a cap on dividends for the medium time period, at worst pointing to a dividend reduce YoY. The corporate shouldn’t be cash-rich with a web debt steadiness of JPY14.1 billion/USD97 million, equating to a web debt to fairness of 0.9x, which isn’t a significant concern however highlights limits over the corporate’s capacity to cater to rising shareholder returns.

Regardless of the corporate recording traditionally excessive working margins of 14.3% in FY3/2022, it could seem that this was a one-off and never a sustainable pattern. To conclude, consensus forecasts are deceptive in our view.

Valuations

On consensus forecasts, the shares are buying and selling on PER FY3/2024 12.6x. There’s a danger that the corporate’s EPS might attain this degree, however purely by paper positive aspects (beneath non-operating earnings) as US greenback deposits are translated again to the Japanese yen. The market usually doesn’t reward short-term FX translation positive aspects. Nonetheless, the forecast free money move yield of two.4% appears to be like too excessive given the potential for money burn, and consequently, we don’t imagine the shares look undervalued.

Dangers

The corporate could also be seen as a key participant within the semiconductor provide chain, and consequently could also be valued at a better valuation a number of than traditionally assessed. After a significant correction within the share worth, buyers might view that every one the negatives have been priced in, and the longer-term image is enticing given Toyo Gosei’s publicity to structural development in semiconductor manufacturing.

Detrimental dangers embody weaker than anticipated Q2 FY3/2023 outcomes, with FY firm steering being revised down as price pressures are quantified and the earnings outlook downgraded. Administration can also restrict proposals over future dividend hikes, given the dangers of rising financing prices.

Conclusion

We imagine latest buying and selling is weak at Toyo Gosei and this can be highlighted in Q2 FY3/2023 outcomes. The shares have corrected 53% YTD, and therefore we don’t see main draw back danger. Nonetheless, given the corporate’s comparatively sketchy monitor document of free money move technology, and its restricted capacity in boosting costs to mitigate price inflation, we don’t see the shares as being enticing. We’ve got a impartial ranking on the shares.