cemagraphics

Shoppers’ high 12 holdings (listed 1-12), unfold throughout separate accounts, custodied at Schwab, as of 8.31.24 (YTD returns as of 8/31/24):

- JPMorgan Earnings Fund (JPMIX), YTD return +6.09%

- Microsoft (MSFT) +11.53% YTD return

- JPMorgan (JPM): +34.13% YTD return

- Nasdaq 100 (QQQ): +16.64% YTD return

- Amazon (AMZN): +17.48% YTD return

- Oakmark Worldwide (OAKIX): +1.15% YTD return

- Schwab (SCHW): -4.29% YTD return

- Netflix (NFLX): +44.05% YTD return

- S&P 500 ETF (SPY): +19.35% YTD return

- Alphabet (GOOGL): +17.10% YTD return

- Rising Markets ex-China ETF (EMXC): +10.41% YTD return

- Walmart (WMT): +48.15% YTD return

JPMorgan, Netflix and Walmart are the large outperformers YTD. Microsoft, Amazon and the Nasdaq 100 now underperforming the S&P 500 YTD.

(Discovered under in a distinct part of the weblog, taking a look at SPDR ETF returns by sector, XLK (know-how) is the one ETF that has a decrease whole return YTD right this moment, August 31 ’24, than on June 30 ’24.)

Oakmark’s weight has been minimize in half for the reason that final time the “high 10” was up to date, on July 4, 2024 (right here). David Herro – the Worldwide portfolio supervisor of the last decade between 2000 and 2009 – is the Oakmark Int’l PM that’s high canine on the Oakmark Worldwide group. It’s been powerful to endure by means of the efficiency differential between Oakmark and the S&P 500. Any worldwide fund or ETF that doesn’t have a US element (ex-US) is seeing single-digit returns, however the final 30 to 60 days, maybe as a result of weaker greenback, the asset class is beginning to stir. Shoppers’ different two Non-US ETFs held are the EMXC (listed above, and +10.41% YTD), and the Vanguard Developed Market ETF (VEA), +11.04% YTD, are at the very least up greater than 10% YTD.

My greatest fear about worldwide, rising markets, and Non-US investing is that (I think) China’s development within the late Nineteen Nineties by means of the nice monetary disaster drove a lot of the European and rising market returns again 15-20 years in the past, when the BRICs have been red-hot (Brazil, Russia, India, and China).

China’s GDP development – whereas of low high quality – grew 10-15% per 12 months from 2000 by means of 2009 and a bit past. Right this moment, China’s annual GDP development is a far cry from that development price, with little proof that it’s going to return to wherever near that stage.

JPMorgan has a neat little worldwide fund – JPMorgan Developed Int’l Worth (JFEAX) – which is being acquired in small quantities at current. The fund is up 15.27% YTD as of August 31, with no US publicity (it’s onerous to search out a world fund up 15% YTD with no US large-cap shares) however a heavy obese in financials. Of the highest 10 holdings, 5 shares have euro or British pound forex. The ten-year annualized return on the JFEAX is 3.99%, whereas the 10-year annualized return on the S&P 500 (SPY) is 12.88%. (All return information sourced from Morningstar.)

Portfolio development is sort of a skilled sports activities group: you want your huge canine to indicate up on the large day and make the large performs (i.e., outperform), and the supporting forged has to not detract from group efficiency (i.e., don’t be too divergent when it comes to benchmark returns).

Sector efficiency beneath loosening financial coverage

Shifting on, the final comparatively regular interval when the Fed / FOMC / Jay Powell lowered the fed funds price was the 12 months 2019, after the fed funds price hikes began by Janet Yellen.

Right here’s how the varied sectors carried out in 2019 as Jay Powell lowered the fed funds price from shut to three%, to finish up between 1.5% and 1.75% in September 2019, the place it remained till March 2020.

Healthcare (XLV) and vitality (XLE) have been laggards in 2019. Power was downright terrible that 12 months.

Solely know-how beat the S&P 500, whereas shopper discretionary (XLY) (Amazon and Tesla) and communication companies (Google and Meta) have been shut. Financials too (XLF) returned 29% in 2019.

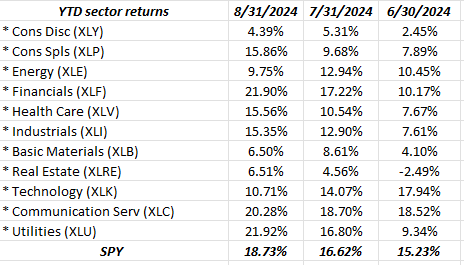

Right this moment, we’re beginning to see financials (XLF), actual property (XLRE) and utilities (XLU) – all lengthy thought-about curiosity rate-sensitive sectors – begin to outperform.

Right here’s the final 3 months returns for a similar sector ETFs used above. (Return supply is Bespoke Weekly Report.)

Financials have doubled within the final 60 days, know-how has misplaced 700 bps of return, falling from a +17% return on the XLK as of June 30 ’24, to +10.71% as of August 31. The truth is, know-how (XLK) is the one SPDR ETF that has misplaced floor since June 30 ’24 when it comes to YTD whole return. (See the desk simply above.)

Remaining remark: Excessive-yield credit score continues to commerce very nicely, at the same time as TLT fell 1% Friday, 8/30/24, on above-average quantity. Company excessive yield’s continued constructive returns – one of the best of the varied fixed-income lessons except for rising market credit score, which can be performing nicely – tells us that recession threat stays low.

A number of employment information this coming week, the August nonfarm payroll report anticipating +150,000, (138,000 for personal payrolls) “internet new jobs added” to the US economic system in August ’24. We additionally get JOLTS on Wednesday morning, ADP Thursday morning, September fifth, in addition to jobless claims (Supply: Briefing.com).

None of it is a suggestion or recommendation, however solely an opinion. Previous efficiency isn’t any assure of future outcomes. Investing can contain the lack of principal, even for brief intervals of time.

Thanks for studying.

Authentic Put up

Editor’s Word: The abstract bullets for this text have been chosen by Searching for Alpha editors.