William_Potter

Launched by State Avenue International Advisors and managed by SSGA Funds Administration, Inc., SPDR Portfolio Mortgage Backed Bond ETF (NYSEARCA:SPMB) seeks to offer broad publicity to company mortgage backed securities in america. SPMB makes use of a market worth methodology in weighting and deciding on its holdings, and it seeks to trace the efficiency of the Bloomberg U.S. MBS Index utilizing a consultant sampling approach. The fund was launched in 2009 and has amassed an AUM of $4.34 billion. The fund is rebalanced on the final enterprise day of every month.

Holding Evaluation

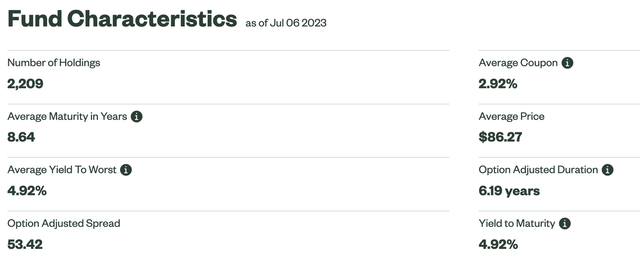

As talked about earlier, SPMB invests in company mortgage backed securities of the U.S. funding grade bond market. The fund invests in a complete of two,209 holdings and has a mean maturity of 8.64 years.

SSGA

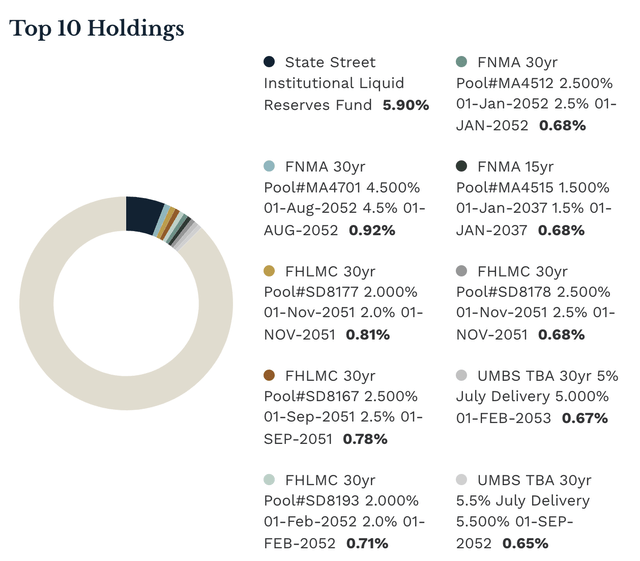

The fund is skewed in direction of the State Avenue Institutional Liquid Reserves Fund, with a weighting of practically 6%. Its high 10 holdings represent roughly 12% of its whole portfolio.

etf.com

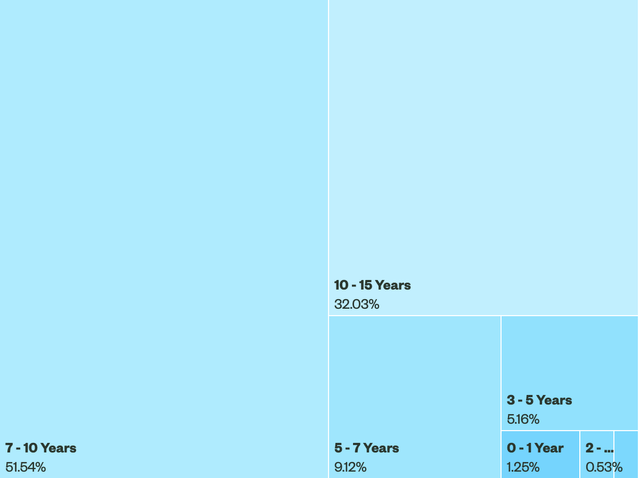

For the reason that fund invests in company mortgage-backed securities, the standard of its holdings is 100% of the best funding grade of AAA. These bonds usually have a decrease threat of default but in addition could have decrease yields than much less creditworthy bonds. Inside SPMB, bonds even have a variety of maturities, with a predominant give attention to 7-10 12 months maturities. A complete breakdown could be seen under.

SSGA

Why Make investments MBS: Low Bills, Low Threat, With Decrease Yield

Company mortgage backed safety funds are recognized to be very secure investments as they’ve restricted credit score threat due to their relationship with the U.S. authorities and the U.S. Treasury. These bonds are issued by considered one of two government-sponsored enterprises (Fannie Mae or Freddie Mac) and are all rated of the best funding grade high quality of AAA. These funds present stability, liquidity, and have favorable valuations throughout instances of uncertainty and volatility. Nevertheless, due to its restricted credit score threat because of backing by the U.S. authorities, these funds could produce decrease yields than different much less creditworthy bonds, resembling company bonds. These bonds additionally usually have decrease prices when lenders and debtors make giant transactions, as seen in SPMB’s low expense ratio of 0.04%. Lots of SPMB’s closest friends even have comparatively low expense ratios.

As for yields, MBS usually carry larger yields than U.S. Treasuries, however proper now, company MBS yields have been unfavorable because of the inverted yield curve persisting for the previous 12 months. Brief maturity bonds have reported the best yields, with long-term bonds reporting decrease yields. Historically, the yield curve is upward-sloping, the place longer-term securities yield extra shorter-term securities. SPMB invests a considerable portion, 52%, in 7-10 12 months bonds and a barely decrease 32% in 10-15 12 months bonds, making the yield barely decrease than common at the moment. SPMB has a 30-day SEC yield of two.97%, which is significantly decrease than lots of its friends. Beneath is a desk of SPMB’s closest peer ETFs and their respective 30-day SEC yield.

| iShares GNMA Bond ETF (GNMA) | 3.52% |

| Janus Henderson Mortgage-Backed Securities ETF (JMBS) | 4.73% |

| iShares MBS ETF (MBB) | 3.00% |

| Vanguard Mortgage-Backed Secs Idx Fund ETF (VMBS) | 3.32 |

Droop within the MBS Market

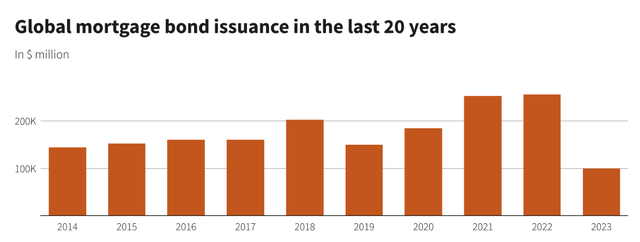

The U.S. Company MBS market has skilled a stoop in 2022 and into 2023 because of headwinds within the U.S. housing market. The stoop was exacerbated by the failure of a number of regional banks within the US, together with Silicon Valley Financial institution, Signature Financial institution, and First Republic Financial institution. The truth is, the issuance of world MBS reached a 23-year low within the first quarter of 2023 as mortgage charges elevated and property gross sales and refinancing decreased. As seen within the graph under, international MBS issuance decreased to a low of $100 billion, which is its lowest level since 2000. In the end, this decline in MBS issuances can result in a decreased availability of credit score, making it tougher for home-owners and property builders to safe financing. This vicious cycle can probably result in decrease MBS issuances within the close to future.

Reuters

Regardless of the report low MBS issuances and its projected contraction over the subsequent 2 years, the precise provide of MBS on sale is anticipated to extend dramatically over the interval. This rise in provide could be primarily attributed to the Federal Reserve’s financial tightening coverage supposed to fight inflation. In making an attempt to cut back inflation, the Fed’s aggressive rate of interest hikes previously few months together with its discount in its purchases of MBS have led to this enhance in provide. The unfold between MBS costs and the underlying mortgages is rising, which is one other headwind for the company MBS market.

As Recession Looms, Company MBS Outperform

Whereas it’s true that company MBS has been sluggish previously 12 months, I imagine that these securities could have favorable alternatives because the financial system looms nearer to a recession. U.S. company MBS have traditionally outperformed throughout recessions, they usually additionally could profit from the eventual pause of rate of interest hikes. The Fed has already slowed down hikes dramatically from months earlier, and this can be a sign of rates of interest nearing its peak earlier than dropping right down to regular ranges.

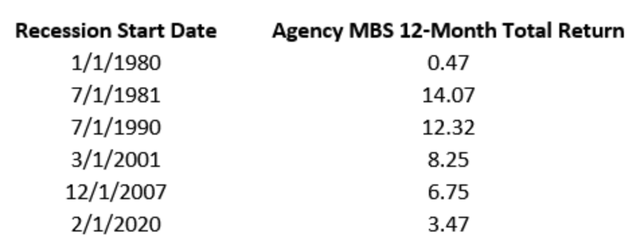

For the reason that inception of MBS within the late Seventies, there have been six recessions, and in each recession, the company MBS index reported optimistic complete return charges over the 12 months that adopted the onset of the recession. Furthermore, these bonds have additionally outperformed funding grade company bonds by a mean of 370 foundation factors throughout these instances.

Bloomberg

Funding Opinion

I’m sensing that government-guaranteed company MBS bonds ought to expertise an uptrend within the close to future, if not the approaching months. The MBS market has probably rebounded from its stoop previously 12 months and a half, and it ought to profit from a better chance of a recession. These bonds proceed to supply favorable yields whereas being among the most secure devices one should buy throughout instances like this. That is additionally to not point out the favorable valuations these securities provide. In the end, because the financial system slows down and enters a recession, high-quality debt devices like MBS will develop more and more favorable amongst buyers who’re in search of a secure, but high-yielding funding to journey out the recession. I fee SPMB a Purchase.