abadonian

It’s definitely no secret that the utility sector has been crushed down by the market for the reason that starting of 2023. In accordance with Morningstar, the “median 16.0 P/E (for utilities) is at its lowest since exiting the 2008-09 recession,” and the sector is now down 16.0% for the reason that starting of 2023. This has made many high-quality utilities look extra enticing to traders and Spire Inc. (NYSE:SR) is definitely one among them. I imagine the shares are undervalued by 10.0% presently and the 5.3% yield is now aggressive with what cash markets are paying. At at this time’s discounted costs the shares are at a lovely entry level.

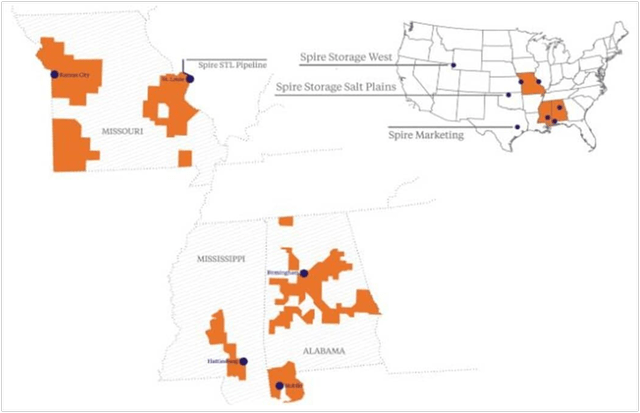

Spire Integrated is a holding firm with 5 subsidiaries. This can be a pure gasoline utility serving 1.7 million prospects with 61,200 miles of pipe. It operates in 4 markets, that are Alabama, Mississippi, the Gulf, and Missouri. The State of Missouri represents about 70.0% of the shopper base. Immediately, about 90.0% of Spire’s enterprise is regulated gasoline utilities whereas one other 10.0% is advertising and marketing and midstream operations. The corporate has a present market cap of $2.88 billion with a beta of 0.51, that means that shares are much less unstable than the market as an entire. Customary & Poor’s presently charges its unsecured debt as A-, or medium funding grade. The latest peak for the share worth was in Could of 2022 at $75.08. The present worth of $54.80 is a 27.0% low cost from that prime.

Spire Service Space (2022 Annual Report)

An Enticing Dividend Yield

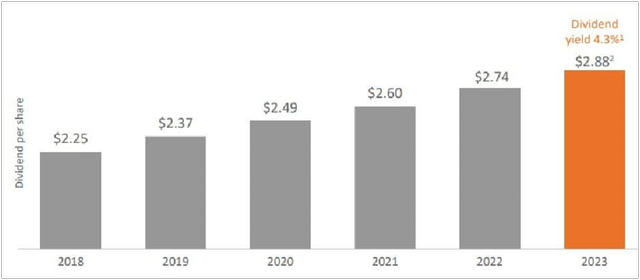

The present yield is a lovely 5.3%. The present payout is $0.72 per quarter and the dividend is paid in March, June, September, and December. The corporate has paid a dividend for the final 78 years, and it has been elevated commonly for the final twenty consecutive years. For the final 5 years, the compound annual improve has been about 5.0%, in step with administration targets. The annual improve is usually introduced subsequent month, possible on the November 16 earnings name and I estimate that the quarterly dividend will likely be raised to $0.76 at the moment, making the yield 5.5% on the present share worth of $54.80. Compared yields at different gasoline utilities are 2.79% at Atmos Vitality (ATO), 7.25% at UGI (UGI), 4.35% at Southwest Gasoline Holdings (SWX), and 5.26% at Northwest Pure (NWN). Offered beneath is a chart of the dividend during the last 5 years and the payout ratios.

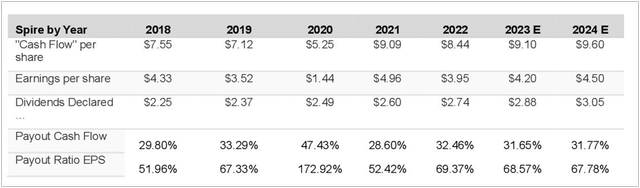

Earnings per Share Development (2023 Investor Presentation) Spire Payout Ratios (Writer Calculated)

The present payout primarily based on earnings per share over time may be very affordable and usually ranges from 51.0% to 69.0% except for one 12 months, 2020. On this 12 months, there was a one-time impairment cost for the Spire Storage West pure gasoline facility in Wyoming. The corporate decided that the brand new challenge beneath growth would take extra time and a part of its worth was not recoverable due to a plan revision. This led to a write-off of $148.6 million or $2.83 per share primarily based on the 52.6 million shares excellent. Earnings per share in 2020 would have been $4.27 in any other case, so the payout ratio would have been 58.4%. Trying on the payout ratio primarily based on money circulate, the numbers are considerably decrease and fluctuate from 29.0% to 47.4%.

Sequence A Most popular Shares are Paying 6.9%

Spire presently has a single sequence of most popular shares, the “A” Sequence 5.9% (SR.PR.A). These have been issued in Could 2019. The popular shares have a present credit standing of BBB from Customary & Poor’s, or decrease funding grade. They’ve a par worth of $25.00 per share and are presently buying and selling at a reduction of $21.42. The dividend is $1.475 per 12 months and the payout is quarterly. On the present share worth, the yield is a really enticing 6.9%. The shares are cumulative and certified. They’re “perpetual” and wouldn’t have a name date, however based on the prospectus, the inventory may be redeemed after August 15, 2024 at $25.00 per share. Tax therapy is “preferential” so the shares are certified. The beta on these is about 0.29 and the common quantity is about 11,000 shares per day.

Latest Earnings Efficiency

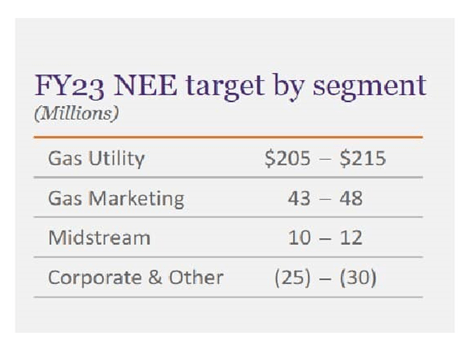

Spire Integrated has a goal of 5.0-7.0% for long-term annual revenue development. Whereas earnings fluctuate in the course of the 12 months and may be seasonal, in the long run they look like extra constant. The goal for earnings per share in 2023 was lowered to $4.15 to $4.25 per share, from $4.20-$4.30, after a $21.6 million loss within the third quarter. That is in comparison with a small loss in the identical interval the prior 12 months of $1.4 million. The corporate’s fiscal 12 months ends on September 30, so the third quarter is usually spring and early summer season. It may be the sluggish season for Spire, and spring 2023 was 22.0% hotter than the 12 months prior. This resulted in decrease residential utilization and better prices, thus the loss. Within the first quarter 2023, the corporate earned $91.0 million or $1.66 per share in comparison with $55.7 million or $1.01 per share within the first quarter 2022. Within the second quarter 2023, it earned $179.2 million or $3.33 per share. The second quarter is January-February-March, when there may be normally excessive demand for heating. As a gasoline utility, Spire has extra seasonality in its revenue than a diversified utility. Under are the forecasts for the 12 months by section in Internet Financial Earnings (NEE) or GAAP earnings which were “adjusted” for utility costs and one-time objects.

Spire Earnings Projections (2023 Investor Presentation)

In 2022, Spire’s revenues have been $2.19 billion down 1.8% from $2.23 billion in 2021, however up 17.7% from $1.86 billion in 2020. Earnings have been $205.7 million in 2022, or $3.95 per share, down from $256.5 million or $4.96 per share in 2021. Curiosity bills elevated and lowered EPS by $0.13 in 2022, because of greater charges for short-term borrowing; these almost tripled. For Spire, greater short-term borrowing normally takes place within the winter months when the utility is buying gasoline for distribution.

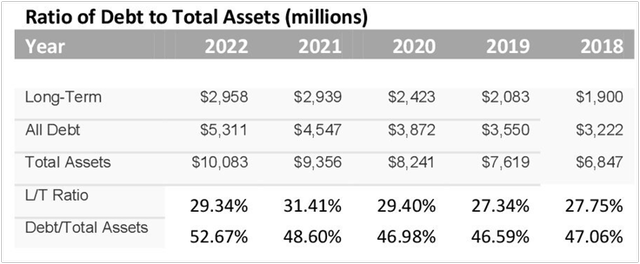

Lengthy-term debt, whereas usually at acceptable ranges, has been rising slowly during the last 5 years. The ratios of long-term debt, and all debt, to whole property are introduced beneath. Whereas the numbers are affordable for a utility, in a rising rate of interest setting, ideally the balances could be happening.

Spire Debt Ratios (Writer calculated)

Regulatory Atmosphere

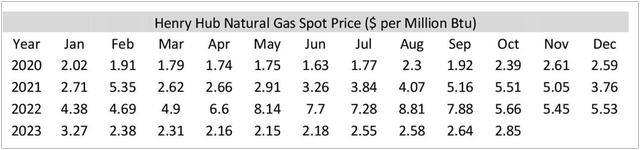

The speed construction is totally different for all three states the corporate operates in (Missouri, Alabama, and Mississippi) however usually appears favorable for the utility. Every state has a provision that enables Spire to go by means of prices because of variations from the norm in temperatures and gasoline provide prices. These can change significantly as proven within the desk beneath.

In Missouri, charges are filed each three years by means of the Missouri Public Service Fee. The state has what is named a Bought Gasoline Adjustment (PGA) clause, which permits the utility to go by means of will increase in prices to their prospects as a hedge. Missouri additionally has a climate normalization rider (as does Mississippi) to get well fastened prices regardless of variance in climate from regular patterns (normally this implies winter). Missouri additionally has an ISRS cost, or infrastructure system substitute surcharge, which may be handed by means of to prospects with no “formal charge case being filed.” Keep in mind, that is the state the place 70.0% of Spire’s enterprise is positioned.

Alabama and the Gulf set a charge yearly with Alabama Public Service Fee. Alabama has a GSA Rider (Gasoline Provide) which offers for a change in gasoline provide costs. The utility can go by means of adjustments in gasoline costs to shoppers. There may be additionally a temperature adjustment provision that offers with departures from climate norms. The allowed return on fairness (ROE) for the utility in Alabama ranges from 9.5% to 9.9%, whereas within the Gulf it’s 9.7-10.3%. Mississippi additionally has a climate normalization rider that adjusts for variations in winter local weather and an allowed ROE of 9.83%.

Henry Hub Spot Value (U Vitality Info)

Capital Expenditures

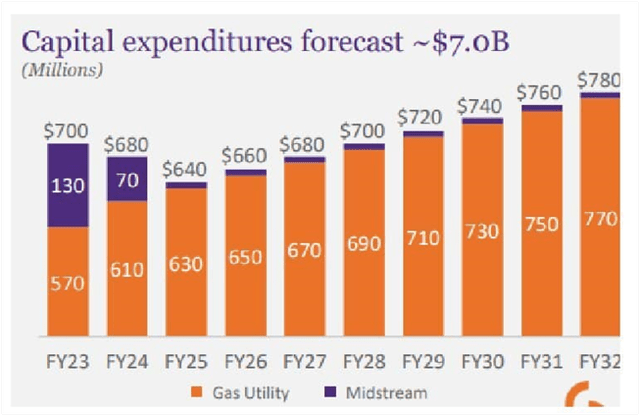

The corporate has a 10-year capital expenditure program of $7.0 billion, between 2023 and 2032. Capital expenditures for 2023 are estimated at $700 million. Quick-term will increase in capex need to do with the brand new Spire Storage West facility. The gasoline utility expenditures are largely for infrastructure upgrades.

Spire Capital Expenditure Plan (2023 Investor Presentation)

Present Valuation of Shares

I estimate the present worth of Spire’s shares to be US $60.78, so at at this time’s worth of $54.80, they’re about 10.0% undervalued. I used a reduced money circulate to worth the inventory, beginning with the earnings per share estimate of $4.20, the newest forecast, starting in 2023 after which projecting ahead. For the low cost charge, I thought-about the common annual return of the S&P 500. The long-term common is about 9.8%, whereas during the last 10 years, it has been greater at 12.4%. I’ve used a reduction charge of 10.0% right here, simply above the decrease finish of the vary, and discounting begins within the second 12 months. I’ve used a reversion charge of 8.0%.

Included beneath are Spire’s earnings per share between 2018 and 2023. Once more, the corporate additionally stories web financial earnings per share (NEE) that are non-GAAP and are adjusted for impairments, regulatory costs, and divestitures that happen with a gasoline firm. They supply a smoother means to have a look at earnings per share. Utilizing these, the compound annual development charge in earnings per share was 2.5%. Morningstar forecasts a median 6.0% annual EPS and dividend development throughout the general utility sector, however I think the quantity for Spire will likely be decrease.

Earnings per Share (Annual Stories)

To be on the conservative facet in evaluating the corporate, I’ve used an annual development charge of 5.0% to account for the range in Spire’s earnings. The ensuing valuation per share is introduced beneath.

Discounted Money Circulate (Writer Calculated)

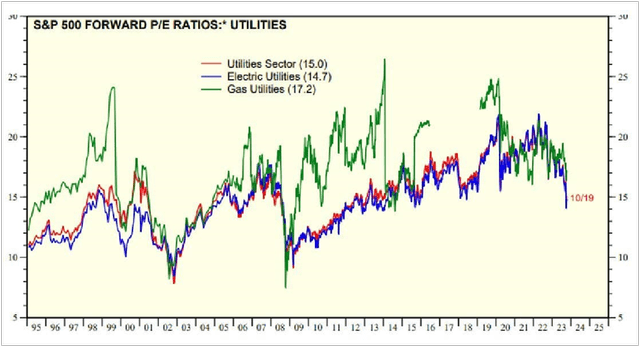

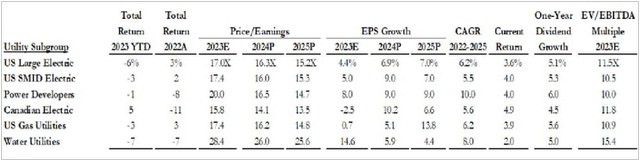

I’ve additionally appeared on the shares utilizing P/E Ratio multiples. In accordance with Morningstar, the present “median 16.0 P/E (of utilities) is at its lowest since exiting the 2008-09 recession.” Morningstar additionally estimates that the sector is 15.0% undervalued. I used to be in a position to find two different sources of P/E multiples together with Yardeni Analysis dated this October, which estimates the present P/E multiples for gasoline utilities as 17.2, above that of electrical utilities. Gabelli Funds additionally tracks utility ratios and lists US massive gasoline utilities as 17.4 for 2023, with a 2024 estimate of 16.2 instances earnings.

P/E Ratios October 2023 (Yardeni Analysis) Utility P/E Ratios (Gabelli Funds)

Utilizing the ahead multiples and the earnings estimate for 2023 of $4.20 per share, the worth by P/E comparable is estimated at 16.2 X $4.20 = $68.04. This could make the shares as a lot as 20.0% undervalued. I’ve concluded on the extra conservative and certain extra correct worth, the DCF estimate of $60.78 per share.

Dangers to Outlook

The first threat with Spire is selection – selection in local weather and selection in pure gasoline prices. The climate in its service areas has been about 20.0% hotter in recent times. Will the development proceed? It definitely lowers earnings per share. And gasoline utilities like Spire appear to have a good quantity of selection from 12 months to 12 months in earnings, though the adjusted web financial earnings are one of the simplest ways to have a look at the corporate. One other threat is rising rates of interest, a threat to all utilities, which appears to have already impacted Spire by means of decrease earnings per share brought on by greater curiosity bills.

Conclusion

The present P/E ratio is 13.0 utilizing the 2023 earnings per share estimate of $4.20 and the present share worth of $54.80. That is properly beneath the general utility a number of of 16.0 cited by Morningstar and properly beneath the gasoline utility multiples of 16.2 – 17.2 cited by Yardeni and Gabelli analysis. Nevertheless, I believe these multiples could also be a lagging indicator. The dividend is at 5.3% and may have one other improve quickly, possible introduced in November. I’ve little doubt that Spire is dedicated to rising its dividend over the long run. As for local weather points, the corporate has favorable riders within the states wherein it operates (particularly Missouri, which is its main market) that permit charge changes to be handed by means of to shoppers for swings or variances in climate norms. So its main markets are “utility pleasant.” I imagine the mixture of a considerably discounted share worth, a positive regulatory setting and a yield that’s already aggressive with cash market funds makes these shares a purchase. The present worth of $54.80 is a really defensible entry level. Even higher if shares development barely decrease. Additionally, the Farmers’ Almanac says Missouri may have a standard chilly winter this 12 months.

{kind=link}