Rob Kim/Getty Photos Leisure

Funding Thesis

Snapchat’s (NYSE:SNAP) inventory has had a steep selloff since my final writeup in July, with shares dropping by 47.57%, pushed by what many buyers noticed as a lukewarm quarter.

Buyers are grappling with the corporate’s slower than competitor development in promoting income. This weak development is regarding for a lot of within the investor base as Snapchat continues to wrestle to compete for advert {dollars} with bigger rivals like Meta (META) and Google (GOOGL), which each dominate the digital promoting market via their bigger person visitors and extra established relationships with advertisers via their distinctive advert era engine.

I perceive why these buyers are involved however I believe this misses a giant level. Snapchat goes after distinctive advert {dollars}, which has been slower to develop however I believe presents a novel set of guarantees for them. With this, I believe there’s nonetheless a ton of room for enchancment of their common income per person (ARPU), one of many benchmark gauges for the way nicely their advert income is performing.

Snapchat’s give attention to direct response advertisements—those who encourage customers to take actions like making purchases in app—will doubtless assist drive ARPU increased. These advertisements have increased conversion charges in comparison with model consciousness campaigns, so they’re extra profitable, and Snapchat’s digicam first method with their app is vital to this.

Regardless of the market’s total bearish sentiment and the hefty drop in shares, I’m nonetheless a powerful purchase on Snap. Their potential for vital ARPU development, given the 3-year consolidation in ARPU charges, in addition to progressive advert codecs and AR investments, presents a extremely compelling alternative.

Why I am Doing Comply with-Up Protection

Like all Bull, I’m bummed at what number of shares have moved down because the final time I lined them in July, even because the S&P 500 has drifted down 2.95% throughout the identical interval.

CEO and Co-Founder Evan Spiegel has overtly acknowledged that the corporate’s slower advert development (in comparison with rivals) is a notable concern for buyers.

Snapchat has confronted mounting strain as different social media platforms, equivalent to Meta’s Instagram and ByteDance’s TikTok, have managed to seize a bigger share of the promoting market. He admitted that Snap’s promoting enterprise will not be increasing on the tempo wanted to match market expectations.

To this identical level, the market has been skeptical of Snapchat’s long-term profitability, given the corporate’s reliance on financing and heavy working losses. Whereas they’ve made lots of progress on innovation, significantly of their AR and ML-driven advert placements, these efforts haven’t but translated right into a return thus far.

I’ve personally been bullish on Snapchat as a result of I believe Snapchat+ with its development will begin to overpower issues round advert income. Nevertheless, the market hasn’t acknowledged this but, and is hyper-fixated on advert income.

The aim of this follow-up protection is to point out that each income paths have alternative, particularly advertisements because the market is so bearish.

Path To Increased ARPU

Over the past three years, Snapchat’s ARPU has stagnated. Whereas the advert market, significantly within the US, has grow to be more difficult, this alone doesn’t clarify the corporate’s efficiency.

On the floor, it seems that ARPU has stagnated within the mid $2 greenback vary, and this reinforces the issues lots of Wall Avenue analysts have about stagnating promoting.

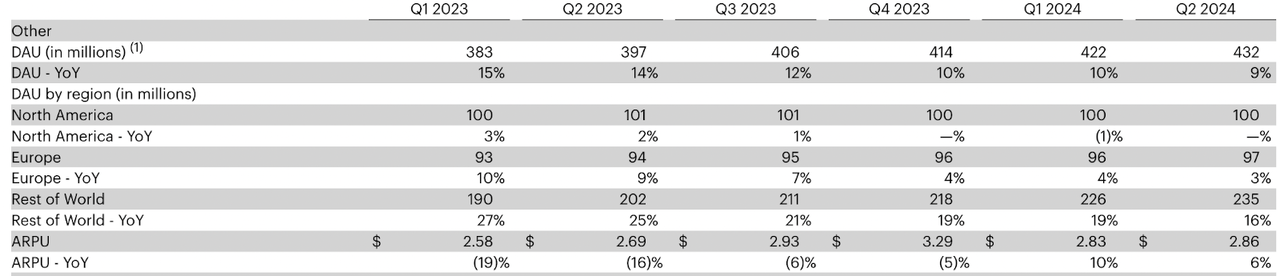

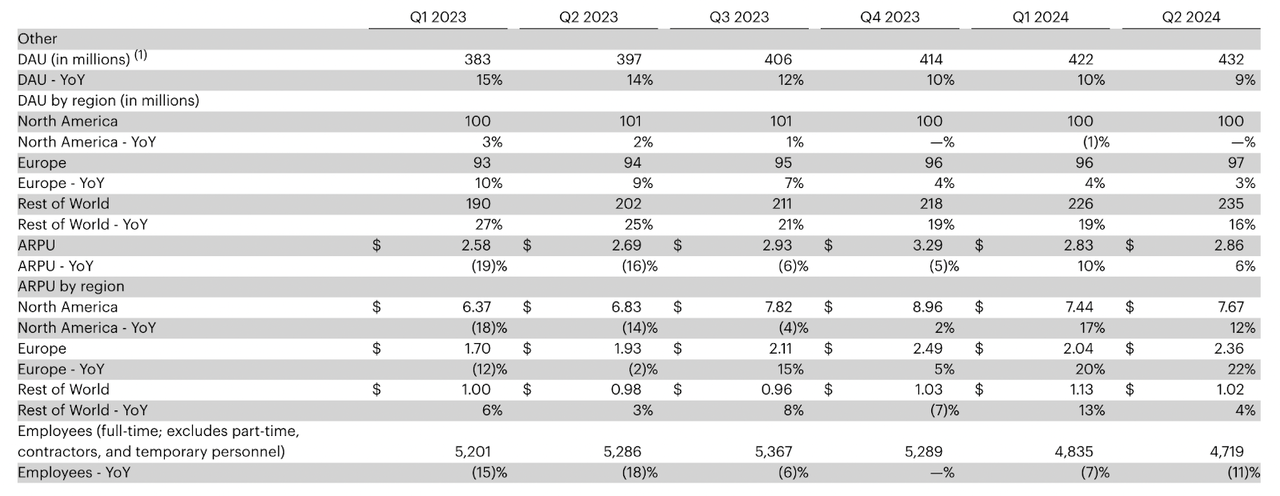

ARPU Knowledge (Snapchat)

However below the floor, that is an averages sport, like I discussed earlier than.

ARPU By Area (Snapchat)

If we minimize the information by area, we will see that ARPU per person in all main areas has grown because the begin of 2023. What has modified is that the proportion of customers which can be in excessive ARPU zones (the US) has declined, whereas the proportion in creating nations has elevated.

In essence, the corporate’s complete ARPU seems weaker as a result of rising share of worldwide customers, however their efficiency throughout the U.S. stays robust. The U.S. market stays very important to Snapchat’s long term plan to be worthwhile, the place promoting demand is increased, and the ARPU has been extra strong.

Throughout Snapchat’s Q2 earnings name, administration went over a number of methods to extend ARPU. Spiegel mentioned the corporate’s efforts to optimize their promoting platform, significantly specializing in direct response (DR) promoting. The DR enterprise, which noticed 16% year-over-year development, has been a driver in ARPU enchancment, benefiting from improvements just like the 7-0 Pixel Buy Optimization mannequin.

He famous:

We continued to make progress on three foundational promoting platform initiatives, together with bigger ML fashions, improved indicators, and extra performant advert codecs. Our 7-0 optimization for purchases continues to drive encouraging outcomes for promoting companions. For instance, Ridge, an on a regular basis necessities e-commerce firm, continued to lean into Snap’s DR greatest practices to drive success. Leveraging 7-0 Optimization, Conversions API, and our ML-based Auto-Bidding, Ridge drove a 73% increased ROAS in comparison with their prior marketing campaign technique.

We additionally expanded 7-0 Optimization to app set up and app buy and, after testing confirmed constant enchancment in cost-per-install and cost-per-purchase, we lately started scaling these merchandise with our promoting companions. We’re inspired to see that quite a lot of gaming app purchasers, together with Roblox, are seeing a 30–50% enchancment in ROAS on Snapchat -Q2 Name.

Administration has additionally reiterated their investments in AI-powered options that improve person engagement and promoting potential via superior AR lenses and AI Snaps. I believe this actually exhibits how far Snapchat has are available in creating richer, extra interactive experiences.

Our sponsored AR promoting options provide entrepreneurs the chance to leverage distinctive and fascinating augmented actuality experiences that elevate the measurable efficiency of their model campaigns. Particularly, analysis has proven that campaigns that pair AR Advertisements with Video Advertisements on Snapchat ship 1.6x advert consciousness elevate when in comparison with Video Advertisements alone.

Analysis from our partnership with OMD and Amplified Intelligence discovered that Snapchat campaigns that embody AR of their combine drive 5x extra lively consideration in comparison with trade friends. With a purpose to increase the attain and impression of our AR promoting options, we lately launched AR Extensions for companies, which prolong our AR promoting merchandise past the digicam to all of our advert surfaces, together with our Dynamic Product Advertisements, Snap Advertisements, Assortment Advertisements, Commercials, and Highlight -Q2 Name.

CTO Bobby Murphy beforehand touched on Snapchat’s Lens Studio—enhanced with AI—that allows quicker and extra complicated AR content material creation, which could be leveraged for promoting functions.

The large takeaway from all of this: the promoting scenario will not be almost as dangerous because the market thinks it’s. They’re making all the proper investments (for my part) and I believe these are going to repay. ARPU seems to be robust below the floor too. The trick from right here can be elevating the common with a better share of customers in nations which have decrease ARPUs. I believe they’ll be capable to do it.

Valuation

A part of the rationale the market continues to depress Snapchat’s shares has been issues over their dual-class construction that leaves Evan Spiegel and the opposite founders in management. What this implies is that the market is aware of that as a result of this voting construction, activist buyers can not get entangled in Snapchat to push for change from the skin. It should be the group that’s in place (or a group that’s blessed by the present administration) that will get the job accomplished.

Even with this restriction, I disagree with the market’s sentiment. I’m assured within the group.

The corporate remains to be making the proper investments, with a spotlight in the direction of AI and AR that I believe presents alternatives for actual development. With deliberate AI investments reaching $1.5 billion yearly, I believe they’ve lots of room to assist enhance their advertisements engine.

At the moment, Snapchat’s ahead P/S a number of stands at 2.67, above the sector median of 1.25 however considerably under the P/S a number of of Meta (7.83) and Reddit (RDDT) (7.92). The market and Wall Avenue analysts really feel significantly better about each Meta and Reddit monetizing their customers than they do about Snapchat as evidenced by the upper Value to Gross sales ratio. To be clear, I’m bullish on each Meta, Reddit, and Google for this matter, however I believe the % upside is highest right here for Snapchat.

I believe we should always see Snapchat commerce at a Value/Gross sales nearer to six right here. That is pushed by an advertisements platform that’s in significantly better form than what I believe the market is pricing in, and the Snapchat+ platform that’s rising at a powerful fee.

If we noticed shares transfer as much as this Value/Gross sales of 6, this might characterize 124.72% upside.

I do know this will sound like an exaggeration, however the market is admittedly bearish on the inventory proper now. I believe it has room to run.

Dangers

One of many massive issues round their Advertisements platform is many on Wall Avenue view the Snapchat advert service as much less refined than what Google or Meta can produce as a result of they every have a big AI group in-house to assist every create robust advert platforms. I perceive this concern.

However I disagree with this sentiment total, and wish to reiterate Snapchat’s personal efforts in AI, and their area of interest give attention to AR as being key pillars to overcoming this notion. These efforts have been paying off, with the corporate partnering with Amazon in 2023 to point out how their distinctive AR angle will assist corporations like Amazon promote and promote their merchandise in distinctive settings.

Any startup or non trade incumbent stands a greater likelihood to area of interest down and give attention to dominating one a part of a market (on this case digital advertisements) earlier than branching out. Snapchat is doing that. The efforts are beginning to repay.

Backside Line

I believe the market is just too bearish on the present state of Snapchat’s advert mannequin, with Administration honing in on growing ARPU via inventive content material channels whereas Snapchat+ scales towards spectacular ARR. Whereas ARPU has stagnated over the previous three years, I believe this statistic is being distorted by Snapchat’s robust development in rising markets. Markets you simply entered usually are typically much less profitable than markets which can be developed. I count on APRU to develop from right here.

Don’t get me mistaken, it is undoubtedly a high-risk funding, however I believe the risk-to-reward ratio right here seems extremely favorable. With this, I proceed to consider shares are a powerful purchase. There’s strong upside accessible for buyers keen to tolerate the danger of Snapchat’s distinctive method to the advert market.

{kind=link}