remco86/iStock by way of Getty Photographs")

Human historical past has been flavoured by some nice comebacks over the centuries. Within the area of sport, there’s the Crimson Sox win that lastly ended the “curse of the Bambino.” We can also’t overlook the nice Tom Brady taking the Patriots from a 28-3 deficit to a Tremendous Bowl win in opposition to the Falcons. Army historical past, too, is plagued by comebacks, from the defeat of the Spanish Armada to Saratoga. Commercially minded folks, lots of whom peruse this web site, could keep in mind the Apple or Common Motors comebacks amongst many others. We love these tales as a result of they remind us that the human spirit can overcome unfathomably dangerous odds. I like such tales, however in my opinion, one story stands out above all of the others like a colossus. Doyle’s bearish Xylem name should be ranked at, or very close to the highest of, the checklist of the best comebacks in human historical past.

We now know that since Doyle put out his bearish name on Xylem Inc. (NYSE:XYL), the shares are down about 13.6% in opposition to a achieve of ~21.75% for the S&P 500. It wasn’t a simple journey for him, although. The worth was ~$101 when Doyle put out his bearish name, however the market ignored him because it very incessantly does, and drove the shares about 32% larger earlier than turning. Did Doyle crack beneath this strain? He didn’t. Did the worth strikes of the inventory alter his bearish perspective on this identify? They didn’t. Doyle held quick, because the residing embodiment of his household motto: fortitudine vincit (“he conquers by way of fortitude”). The shares cracked and started the grinding descent to the place they’re right this moment.

I clearly have a wholesome self picture, and who would not love individuals who brag excessively or converse of themselves within the third individual? Though I would like to proceed to indulge on this means, I am positive you are not right here for one more dose of my self-aggrandizements. I have been bullish on this enterprise prior to now, and I am open to being so once more. In spite of everything, a inventory buying and selling at $86 is definitionally much less dangerous than that very same inventory when it is buying and selling at $101. I will decide whether or not or not I need to purchase again in by the newest monetary historical past right here, and by wanting on the inventory as a factor distinct from the underlying enterprise. Lastly, I hope I am not spoiling the shock, however I shall be writing about put choices, too.

If it is not apparent by now, my writing might be “a bit a lot” for causes too quite a few to checklist. For that purpose, I put up a “thesis assertion” close to the start of my articles with a view to expose readers to as little of my stuff as completely vital. I do that for all of you. Not each hero wears a cape. Anyway, in my opinion, shares are nonetheless too costly, particularly in gentle of the truth that the newest monetary efficiency has been combined. I like the truth that the dividend rose, and I like the truth that it is fairly sustainable. The valuation trumps all, although, and I am unable to purchase at present costs. Simply because the shares aren’t value it but doesn’t suggest there’s nothing to be performed right here, although. I’ve earned about $10 per share in put premia on this identify, and I plan so as to add to the pile right this moment. Particularly, I will be promoting the October places with a strike of $65. I think about this to be a “win-win” commerce. If the shares stay above $65 over the following seven months, I will add the premium thus earned to the whiskey acquisition fund. If the shares fall in worth, I will be obliged to purchase, however will accomplish that at a 24% low cost to the present degree, at a dividend yield of ~1.8%. There you might have it. That is my thesis assertion, which means you can go away this text now, having obtained most of my, uh, “knowledge.” That implies that in case you learn on, that is on you. I do not need to learn any whining within the feedback part about my horrible jokes or odious self aggrandizement that I rise up to past this level.

Monetary Historical past

I would characterize the newest monetary efficiency right here as being a “combined bag” relative to the previous two years. Whereas income was about 6.5% larger in 2021 than it was in 2020, it was truly about 1% decrease than it was in 2019. Web earnings was a lot larger than the earlier two years, which was extra a operate of the actual fact that there have been no goodwill impairment or restructuring and asset impairment fees in 2021 relative to the earlier two years. Regardless of that softness, administration rewarded shareholders with a 7.7% uptick in dividend funds over the 12 months. The corporate additionally reversed the deterioration we noticed within the stability sheet in 2020. Particularly, long run debt is down about 21% from 2020, which I believe reduces the danger right here considerably.

Lastly, I believe the dividend in all fairness effectively lined. As an illustration, the corporate has about 6.5 instances additional cash available than they spend on dividends yearly. Moreover, of the corporate’s $2.44 billion of debt, absolutely 77% is due in 2026 or later. Given this, I would be completely satisfied to purchase again in on the proper worth.

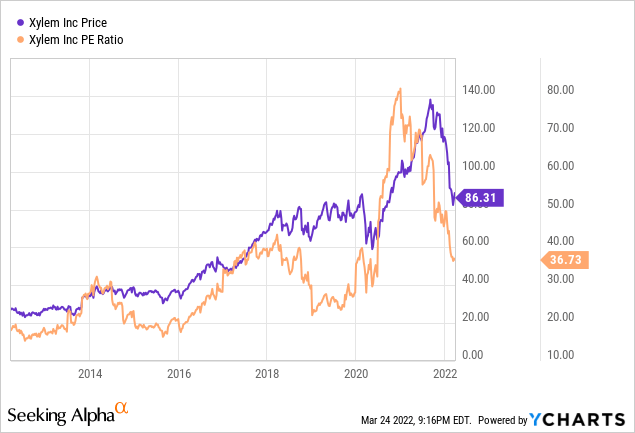

Xylem Financials (Xylem Investor Relations)

The Inventory

A few of you who comply with me repeatedly for some purpose know that it is at this level within the article the place I flip into an actual killjoy as a result of I begin yammering on about how a terrific firm generally is a horrible funding on the mistaken worth. Phrases like “on the proper worth” reveal the truth that I am concurrently each a “fuddy” and a “duddy.” I deal with the inventory as one thing aside from the enterprise, as a result of I am of the view that the previous is ruled extra by the temper of the gang than a lot that we are able to presently measure within the firm. The change in inventory worth is ruled by provide and demand for shares basically, what the market “feels” in regards to the very long run prospects of a given firm, and so on. Thus, I believe the inventory is usually a poor proxy for the altering fortunes on the enterprise, so we have to think about it as a factor unto itself.

Somewhat than bore you greater than is totally vital, I will use Xylem inventory itself to display the relevance of the inventory itself to returns. The corporate launched earnings precisely one month in the past. If an investor purchased early afternoon that day, they’d be down about 4.4% as of this morning. If an investor purchased this inventory on March eighth to select a date fully at random, they’re up about 4%. Clearly not sufficient modified on the agency between February 25 and March 8 to warrant an 8% swing in returns. The buyers who purchased just about equivalent shares extra cheaply did higher. Because of this I attempt to keep away from overpaying for shares.

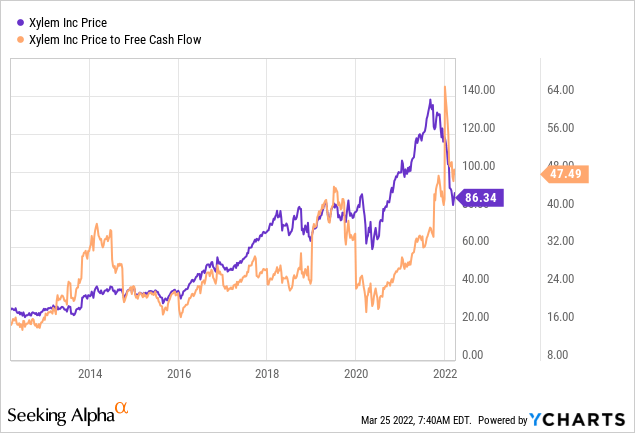

For those who’re considered one of my “regulars”, you already know that I measure the cheapness of a inventory in a couple of methods, starting from the straightforward to the extra complicated. On the straightforward aspect, I have a look at the ratio of worth to some measure of financial worth like gross sales, earnings, free money circulate, and the like. Ideally, I need to see a inventory buying and selling at a reduction to each its personal historical past and the general market. In my earlier missive, I needed to attain for considered one of my fainting couches as a result of the worth to earnings ratio was approaching 90 instances, and a worth to free money circulate of ~27.

I believe the state of affairs has improved in some methods, and deteriorated in others, per the next:

Supply: YCharts

Supply: YCharts

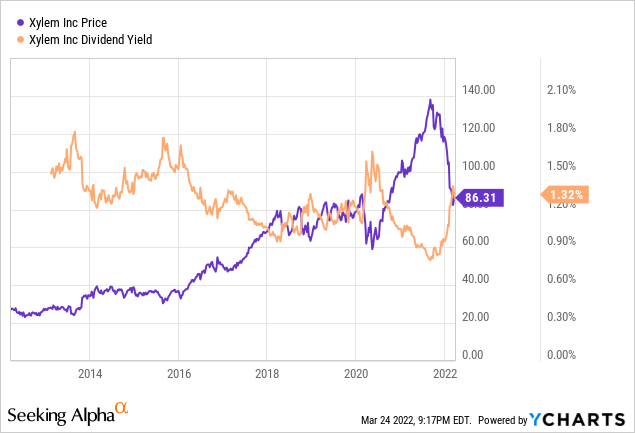

On the identical time, although, due to the current dividend will increase, the yield is definitely approaching a extra affordable degree in my opinion. This means that the corporate is definitely getting near a worth that I would think about shopping for at.

Supply: YCharts

My common victims know that along with easy ratios, I need to attempt to perceive what the market is presently “assuming” about the way forward for this firm. With a purpose to do that, I flip to the work of Professor Stephen Penman and his e-book “Accounting for Worth.” On this e-book, Penman walks buyers by way of how they will apply the magic of highschool algebra to a typical finance components with a view to work out what the market is “pondering” a few given firm’s future development. This includes isolating the “g” (development) variable in a reasonably commonplace finance components. Making use of this strategy to Xylem in the meanwhile suggests the market is assuming that this firm will develop at a perpetual price of ~7.5%, which I think about to be very optimistic. Given the entire above, the shares are nonetheless too wealthy for my blood, so I will not be shopping for again in but.

Choices As An Various

Forged your minds again, if you’ll, to my earlier work on Xylem. In my earlier missive on this identify, I identified that I’ve earned about $10 from promoting places on this inventory over time. When it was buying and selling at $101, although, I could not promote places as a result of the premia on provide for affordable strike costs was too skinny. Now that the shares are cheaper, and the dividend yield is larger, we’re again in enterprise. I am now capable of earn an affordable premium from put choices, so I’ll do exactly that. Earlier than moving into the specifics, I will remind you, but once more, that I think about sure brief places to be “win-win” trades. If the shares stay above the strike worth, I will merely add the premium thus earned to the whiskey acquisition fund. If the shares fall under the strike worth, I will be obliged to purchase, however will accomplish that at a worth that I’ve already determined is appropriate. Both consequence works effectively, therefore, “win-win.”

Now that the not-so-subtle bragging and concept spiel are performed, it is time to get into specifics. I am recommending promoting the October places with a strike of $65. These are presently bid at $1.00. I think about this sale to be a “win-win”, clearly, as a result of I am snug with both consequence. If the shares stay above $65 for the following seven months, I will throw this premium onto the pile. If the shares fall one other 24% from present ranges, I will be obliged to purchase, however will accomplish that at a worth that strains up with a dividend yield of ~1.8%. On condition that I believe the dividend is protected, I would be completely satisfied to purchase at this price.

It is time to change tone just a little bit. In case you are the type to take the phrase of a stranger on the web, I’ve an ethical obligation to rein you in just a little bit by writing about threat. In spite of everything, it is all effectively and good for me to characterize this stuff as “win-win” trades as I incessantly do, however every part comes with some measure of threat, and brief places are not any exception. I am beginning to divide the dangers right here between the financial and the emotional. Let’s evaluation these in flip.

Beginning with the financial dangers, I would say that the brief places I advocate are a small subset of the overall variety of put choices on the market. I am solely ever keen to promote places on firms I would be keen to purchase, and at costs I would be keen to pay. As an illustration, I wasn’t keen to promote Xylem places when the shares have been buying and selling at $101, as a result of the premium was too skinny. Had I performed so, I could have picked up a couple of {dollars} in premium, however I would be sitting on a reasonably large loss on the inventory thus “put” to me. So, rule one is to solely ever promote places on firms you need to personal at (strike) costs you would be keen to pay.

The 2 different dangers related to my short-put technique are each emotional in nature. The primary includes the emotional ache some individuals really feel from lacking out on upside. To make use of this commerce for instance, let’s assume that the market actually likes what’s occurring at Xylem, and the shares bounce to $100 once more this 12 months. In spite of everything, individuals far smarter than me are rising bullish on the long run prospects for this inventory. The brief put solely affords you the choice premium. The return from the brief put could also be decrease threat, however it’s definitely restricted, and that may be emotionally painful for a lot of.

Secondly, I can say from a few years of painful expertise that it may be emotionally painful when the shares crash under your strike worth. Whereas these trades have labored out effectively within the medium to lengthy phrases, largely as a result of my strike costs are normally “screaming buys”, it’s emotionally painful within the brief time period. So, I could make an affordable argument that Xylem shares are a cut price at $65, but when they drop to $50 due to a market meltdown, as an example, that may take an emotional toll. I believe individuals who promote places ought to concentrate on these emotional dangers earlier than promoting.

I will conclude this slightly lengthy, drawn out, ponderous dialogue of dangers by wanting once more on the specifics of the commerce I am recommending. If Xylem shares stay above $65 over the following seven months, I will merely add the premium to my winnings and transfer on. If the shares fall in worth, I will be obliged to purchase, however will accomplish that at a worth that strains up with an affordable dividend yield and a PE of ~27.5, which is sweet for this inventory. All outcomes are very acceptable in my opinion, so I think about this commerce to be the definition of “threat decreasing.” I do know. It is bizarre of me to finish a dialogue of brief put dangers by writing about how these cut back threat. If that is the primary “bizarre” factor you have seen on this article, you are not paying any consideration.

Conclusion

I believe Xylem is an efficient enterprise with a sustainable dividend. The issue is the valuation. Regardless of the truth that I am not keen to purchase the shares at present ranges, I believe it is attainable to earn an honest return promoting the places described above. For those who’re snug promoting places, I would suggest this or an identical commerce. For those who’re not, I would suggest you await shares to fall to a extra affordable degree earlier than pulling the set off right here.