")

wdstock/iStock Editorial through Getty Photographs

Funding Thesis

Salesforce (CRM) raises its fiscal 2023 steering and is predicted to develop by roughly 21% CAGR over the approaching 12 months.

With hindsight, it appears like Salesforce ended up paying roughly 23x ahead gross sales for Slack. It might be argued that maybe Salesforce’s almost $28 billion acquisition value turned out to be a fantastic success.

Salesforce excels in offering buyers with a gradual drip of constructive information and a scarcity of unfavorable surprises. This quarter was no totally different.

Observe, Salesforce’s calendar 12 months and monetary 12 months are misaligned. I will solely confer with its fiscal 12 months.

Investor Sentiment Holds Up For Salesforce Inventory

Not like numerous tech firms, Salesforce’s share value hasn’t meaningfully bought off previously 3 months. Sure, the inventory is down, but it surely’s removed from being on the heart of the carnage that has hit small and mid-cap names.

Moreover, the after-hours response was barely constructive, which within the present market, is much from assured, as numerous firms have reported what seems to be constructive outcomes simply being taken down meaningfully available in the market the following day.

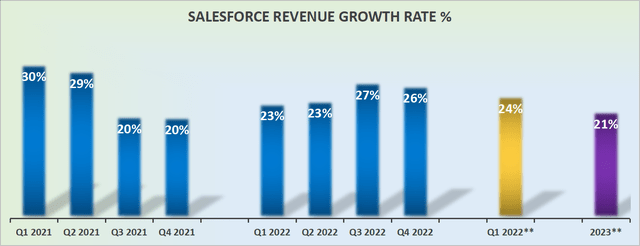

Salesforce’s Income Progress Charges Stay Sturdy

Salesforce reported income progress charges

Salesforce guides for simply over 20% CAGR for the 12 months forward.

Salesforce demonstrably exhibits buyers that regardless of its measurement, it nonetheless has what it takes to develop at an affordable fee.

Salesforce Reviews Finest Quarter in Its Historical past

Salesforce’s earnings calls are all the time upbeat. This time we heard from Salesforce’s co-CEO Marc Benioff speak in regards to the success of this 12 months’s in-person Ohana.

For those who’ve learn Classes From Titans, you may concentrate on the significance of instilling coaching and a assist system in your staff. This can be a sturdy indication of a profitable firm’s effort to put money into its workforce.

Shifting on, Benioff contended throughout the name that,

[We] proceed to see simply great, great demand from prospects throughout each trade, each geography and each product class.

Benioff went on to explain that Salesforce is firing on all cylinders and the way Salesforce simply reported what was arguably the perfect monetary quarter in its historical past.

The message from Salesforce is evident, an increasing number of firms are embarking on their digital transformation and this continues to offer Salesforce with significant tailwinds.

Do CRM’s Earnings Nonetheless Matter?

I ask this query as a result of I merely do not know the reply. This time final 12 months, even discussing earnings was a complete waste of time. Buyers merely did not look after profitability.

But, how shortly has the panorama modified? Proper now, buyers are critically placing much more concentrate on what an organization’s profitability profile appears like, in actuality, not what’s described as a ”long-term” goal.

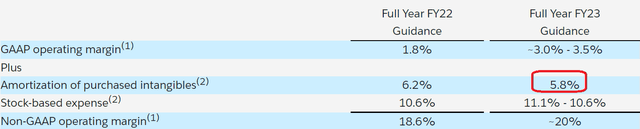

On this entrance, Salesforce’s steering reassures buyers that on a GAAP foundation it is anticipated to enhance its revenue margins by at the least 120 foundation factors over the following twelve months.

Salesforce press assertion

As I am assured you might be conscious, Salesforce’s playbook has been to serially purchase numerous firms after which amortize these purchases again into its working earnings line.

And this technique has clearly labored for a very long time. There is no query on anybody’s thoughts that within the grand scheme of issues Salesforce has been an enormous success.

Moreover, one may now comment that with so many firms so cheaply priced, the current setting could be the proper ”arrange” for Salesforce to go on an extra acquisition spree. Nonetheless, the very fact stays that Salesforce’s steadiness sheet is not all that versatile any longer.

For example, regardless of carrying money and equivalents of slightly below $9.4 billion, it additionally carries money owed of roughly $10.6 billion. This suggests that its steadiness sheet now holds roughly $1.2 billion of web debt.

Consequently, its capability to make significant needle-moving acquisitions goes to be considerably hampered. Here is an instance, Slack was acquired throughout fiscal Q2 2022 and put down almost $28 billion for the corporate.

But, because it transpired, after two quarters, Slack noticed its revenues attain $565 million (web of buying accounting). This might imply that for the 12 months as an entire, Slack will maybe see its revenues attain roughly $1.2 billion.

Consequently, it seems that Salesforce in the end paid near 23x ahead gross sales for Slack. With the advantage of hindsight, this now seems to be a really cheap a number of.

What’s extra, Salesforce is one in all solely a handful of firms which can be anticipated to develop at roughly 20% CAGR within the coming 12 months and can be pointing in the direction of GAAP profitability.

CRM Inventory Valuation – Pretty Priced

Salesforce has for a protracted whereas traded at a big low cost to different SaaS names.

Buyers have not been overly eager to reward Salesforce with a ”SaaS a number of” on the inventory, which is ironic as a result of Salesforce is among the ”unique” SaaS firms.

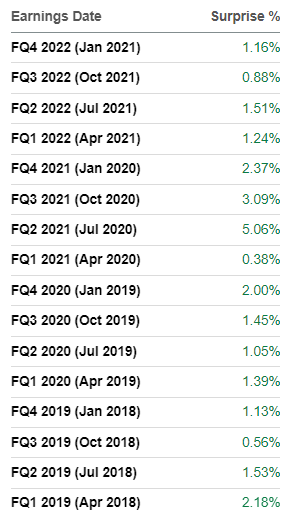

In reality, Salesforce is arguably the one SaaS inventory that has persistently given buyers multi-year income steering and never solely delivered in opposition to that steering, however persistently beat its personal steering for a critically very long time.

Salesforce income beat

With one exception, Salesforce has usually beat analysts’ income estimates by someplace round 1% to 2%, like clockwork.

Thus, I absolutely count on that Salesforce will proceed to tick alongside doing simply that.

The Backside Line

Regardless of Salesforce’s playbook of offering ample long-term steering, loads of visibility into its financials, along with a scarcity of unfavorable surprises, to not point out persistently growing its monetary targets, the market has not been all that excited to pay a premium for Salesforce inventory.

On the constructive facet, when so many excessive progress names are getting shot out of the sky and seeing their multiples meaningfully contract, Salesforce has succeeded in holding its floor and multiples regular.

Within the current market, the dearth of unfavorable surprises might be a value worthwhile paying for.

Nonetheless, I favor to be extra selective and deploy my very own capital into critically compelling alternatives. No matter you determined, good luck and completely satisfied investing.