")

NORRIE3699/iStock by way of Getty Photos

In our final protection of Realty Revenue (NYSE:O) we emphasised that buyers have been higher setup after an 8-year return drought. We went via two completely different longer-term situations on the excessive ends and felt it was arduous to see it as a foul funding, no matter what occurred.

This might create a incredible return profile with dividends reinvested. We predict it is a good funding for long run holders, so long as they maintain their time horizons lengthy and their expectations modest. We’re upgrading this to a Purchase right here.

Supply: 8 Yr Return Drought

This has labored out and the inventory has been virtually flying as if it had modified its identify to “Realty A.I.ncome”. We take a look at the current outcomes and the market pricing of charge cuts to let you know the place we stand.

Q2-2024

Realty Revenue beat Q2-2024 estimates barely, however the quantity gave the impression to be associated to timing of the funds from operations (FFO). The REIT stored its steering for the 12 months unchanged.

Realty Revenue Q2-2024 Presentation

Analysts yawned, we as nicely, and in no rush to alter their estimates.

Searching for Alpha

This was regardless of some considerably decrease rates of interest and credit score spreads that have been in place in comparison with its unique steering. It’s possible that a number of the headwinds bears have spoken about are taking part in out within the background as Realty earnings sells underperforming properties or those the place there’s a large threat of emptiness down the road. You usually do not see the injury from this in a direct manner, however the excessive cap charges (low costs) on these properties are inclined to offset the expansion numbers to an extent.

Europe

One of many huge themes for Realty Revenue has been the push into Europe over the previous couple of years. Lengthy again, it was usually talked about as a optimistic that Realty Revenue was purely US targeted. However bulls have begun to embrace the transatlantic capital move, and admittedly they haven’t any alternative. Realty Revenue is actually urgent its benefit there, with two-thirds of the Q2-2024 capital going there.

Realty Revenue Q2-2024 Presentation

It’s pretty fascinating to see Realty Revenue present some trillion greenback alternatives in Europe.

Realty Revenue Q2-2024 Presentation

It has even gone via the difficulty of exhibiting how precisely this advantages each side, the customer and the purchaser (Realty Revenue on this case).

Realty Revenue Q2-2024 Presentation

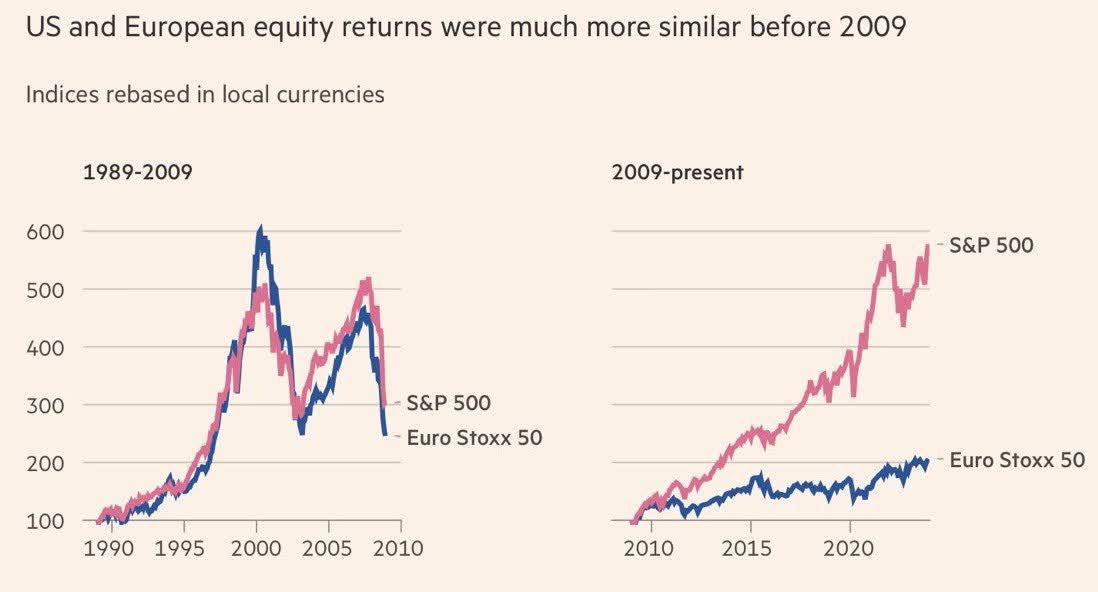

One fascinating factor to look at right here is that the REIT is working inventory buybacks into its mannequin. Clearly, which means it’s speaking in regards to the counterparty being a publicly traded firm. In the event you perceive this half, then you may also perceive the why. European corporations can afford to promote their properties for a comparatively increased cap charge to sale-leaseback transactions as a result of their shares are low cost. We are able to present that portion within the subsequent chart.

Monetary Occasions

So it is a pretty fascinating dynamic that Realty Revenue is exploiting, and one we do not see altering except US shares collapse by 50% or extra. Conversely, we might even see that if European shares have an enormous bull market. However in any case, Europe stays the play for now.

Realty Revenue Q2-2024 Presentation

The Closing Countdown

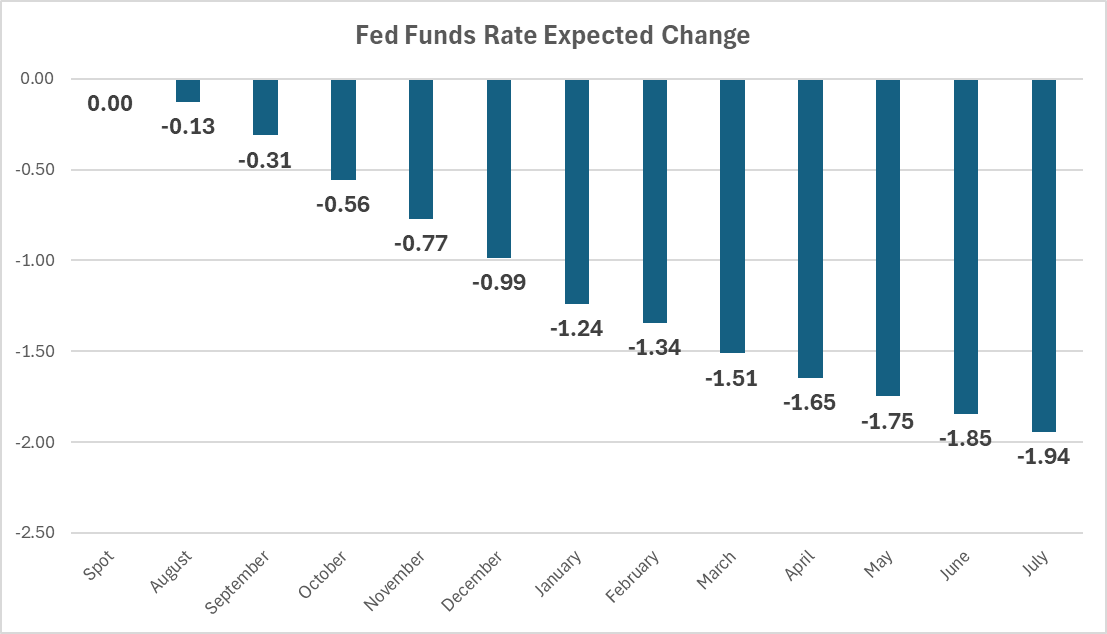

The Federal Reserve has embraced the concept of charge cuts with the markets at all-time highs and inflation remaining nicely above their very own targets. All that is still to be completed is to ship on the 200 foundation factors of charge cuts priced in.

X

To the extent this stays in line with an immaculate tender touchdown, this can assist increased valuation for Realty Revenue. We see no issues with the inventory rerating to a 17X a number of if one thing like this pans out. In any case, we’ve got far poorer high quality REITs like Iron Mountain Integrated (IRM) buying and selling at precisely twice that a number of. After all, the one actual tender touchdown we’ve got had after a barrage of charge hikes was in 1994 and that point the yield curve by no means inverted.

Financial institution OF America

So it stays to be seen whether or not we obtain this.

Verdict

If the speed minimize cycles grow to be too late to stave off a recession, there are as soon as once more dangers to the draw back for the corporate. Alternatively, we would not see the total extent of charge cuts being priced in as inflation resets at the next base and begins transferring up once more. The inventory appears pretty priced right here for what it delivers, and it actually just isn’t resoundingly low cost because it was simply 3 months again. We’re transferring this to a “Maintain” and suppose there are higher actual property shares to invest on for the medium time period.

Realty Revenue Company 6% PFD SER A (NYSE:O.PR)

If the speed minimize predictions are correct, then O.PR is a bit undervalued. That is prone to be redeemed if the Fed Funds transfer down by 200 foundation factors, and we’ve got a tender touchdown. Realty Revenue hates most popular shares, and this one comes courtesy of it buying Spirit Realty Capital. We merely do not personal it as a result of we went lengthy Rexford Industrial Realty, Inc. 5.875% PFD SER B (REXR.PR.B). That one had the next yield on the time (and nonetheless does) and in addition had extra upside to par (and nonetheless does). We charge O.PR as a maintain, however it’s a low-risk play for those who consider in all these charge cuts coming via.

Please be aware that this isn’t monetary recommendation. It could appear to be it, sound prefer it, however surprisingly, it isn’t. Buyers are anticipated to do their very own due diligence and seek the advice of knowledgeable who is aware of their targets and constraints.