akinbostanci/E+ through Getty Pictures

I’ve began a place in RCI Hospitality (NASDAQ:RICK) and now think about the corporate a high choose for 2023. There’s quite a bit to love right here as RCI’s administration continues to execute a particularly shareholder-friendly capital allocation technique in opposition to an aggressive build-out of their portfolio of grownup nightclubs and Bombshells, a military-themed chain of eating places and bars. RCI plans to publish its 10-Q for its fiscal 2023 first quarter ending December 31, 2022, on Thursday ninth February however has already launched gross sales figures for the quarter.

RCI Hospitality

Income from RCI’s portfolio of grownup evening golf equipment got here in at $55.9 million, a rise of 20.7% over the year-ago quarter. While pushed by the acquisitions of recent golf equipment, same-store gross sales had been nonetheless up 1.2% over their year-ago comp. This offset weak point from Bombshells which noticed complete gross sales drop by 9.7% from their year-ago comp. General, mixture gross sales for the quarter at $69.2 million was up by 13.3% from the year-ago interval. So why am I bullish?

Continued Acquisition Momentum Units The Backdrop For 2023 Outperformance

RCI acquired round 15 nightclubs in fiscal 2022 and has maintained this buyout momentum with the acquisition of 5 extra grownup nightclubs in the course of the first quarter of its fiscal 2023. The corporate bought three Chicas Locas and two Child Dolls adults nightclubs within the Dallas-Fort Price and Houston markets for $66.5 million and expects these golf equipment to drive $11 million in EBITDA of their first 12 months, finally rising to round $14 million to $16 million after. This could symbolize a return of round 22.5% on the midpoint of this vary. RCI financed the take care of round $25 million in money, a 10-year 7% $25.5 million vendor financing notice, and 200,000 restricted shares.

Bears would in fact level to a dilution of round 2.17% anticipated in opposition to common diluted shares excellent of round 9.2 million as of the top of the RCI’s fiscal 2022 fourth quarter. Certainly, while this could at a really excessive stage seemingly go in opposition to the corporate’s buyback technique, the annual curiosity expense of the 7% vendor financing notice sits at round $1.75 million. Therefore, the majority of those earnings ought to feed by means of to free money flows and permit the corporate to purchase again extra shares sooner or later.

Utilizing the primary quarter’s income as a baseline and adjusting it for the feed-through of latest acquisitions I would anticipated RCI’s full fiscal 12 months 2023 income to come back in at round $300 million to $350 million, round 21% increased than its fiscal 2022 income on the midpoint of this vary. To be clear right here, that is fully forecasted and precise income could possibly be decrease. Eric Langan in the course of the first quarter gross sales replace acknowledged there was some intermittent softness at some golf equipment.

Potential 2023 Finish Worth On Forecasted Financials

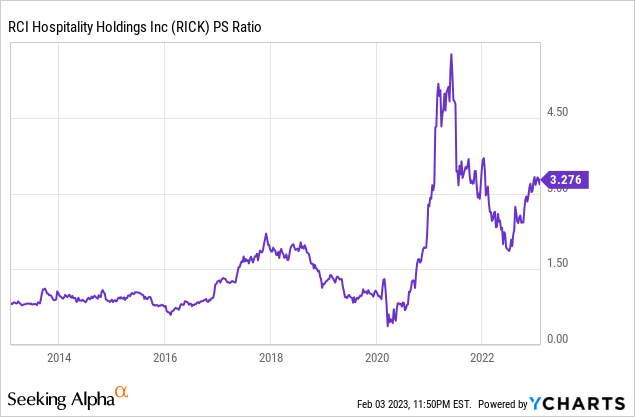

With RCI at present buying and selling at a market cap of $860 million in opposition to forecasted fiscal 2023 income of $325 million, its price-to-forward gross sales a number of at 2.65x is decrease than the present retrospective a number of of three.28x. While this has been risky, we might see the market cap transfer up simply north of $1 billion, or round $108 per share for a 16% capital uplift if the retrospective PS a number of as of the top of RCI’s fiscal 2023 displays its present determine.

Bears would in fact spotlight the scope for the valuation to expertise compression this 12 months particularly if the economic system turns bitter. RCI has been using an upturn in investor enthusiasm for the reason that summer time of 2022 and this might flip again south on the again of broader macroeconomic circumstances. That mentioned, RCI has constructed its operations on an exceptionally cash-generative enterprise and the corporate’s return on its investments continues to come back in at spectacular ranges.

RCI Hospitality

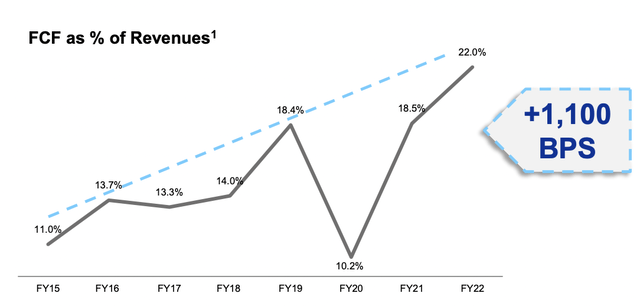

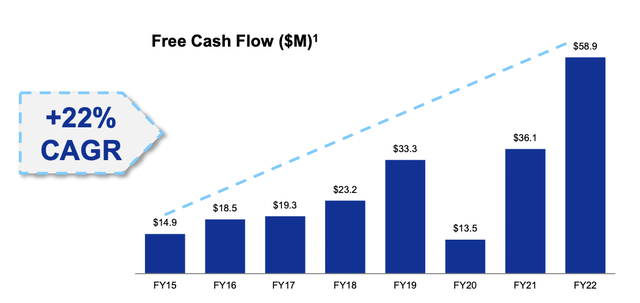

Additional, with RCI’s free money circulate as a per cent of income at present at 22%, the corporate might see free money circulate for 2022 are available in at $71 million, up from $58.9 million within the year-ago comp. This locations into view why RCI varieties one in every of my high picks for 2023.

RCI Hospitality

The corporate is printing money and utilizing that to drive an formidable program of share buybacks, which kind the opposite methodology of returning money to shareholders exterior of dividends. My portfolio is heavy on dividend-paying shares, these critically kind pillars of wealth creation and I believe RCI matches into this bracket. Fixed share buybacks are in themselves a technique of returning worth to shareholders and assist create the circumstances for focus, the inverse of dilution, the place your possession of the corporate rises every interval. Therefore, I see RCI as complementary to my long-term dividend-paying positions. The corporate has moved to outline itself by the hyper-aggressive and fixed buyback of its widespread shares which serves to extend the focus of my holdings.

{kind=link}