")

D3Damon/E+ through Getty Pictures

Overview of the thesis

Rani Therapeutics (NASDAQ:RANI) is growing a robotic tablet to permit oral supply of in any other case injectable medicines. RANI has offered enough proof-of-concept information, each in animal fashions and in early-phase human research, demonstrating profitable and secure supply of drug payloads, reaching bioavailability just like or higher than subcutaneous injections. Importantly, the expertise is payload agnostic, that means huge potential to penetrate the large injectable medicine market. Celltrion partnership on adalimumab ($21.2B in Humira gross sales in 2022) and ustekinumab (Stelara gross sales of $6.4 billion in america and roughly $9.7 billion worldwide in 2022) additional validates the expertise and I would not be stunned if extra partnership information are introduced quickly on different property. Nevertheless, being an early-stage biotech, investing in RANI at this stage is just not with out threat, together with fierce competitors within the subject of oral drug supply and want for lots of money to assist the pipeline.

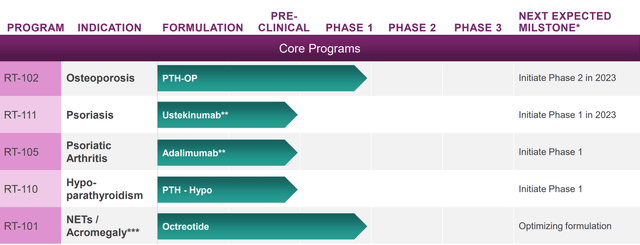

RANI’s present pipeline. Potential for enlargement past this pipeline is big (Rani Therapeutics Company Presentation September 2023)

Overview of the potential

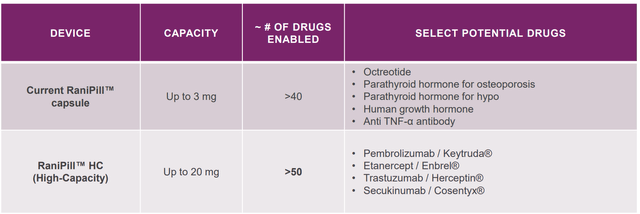

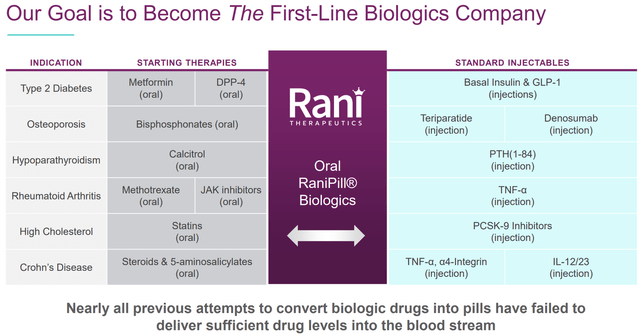

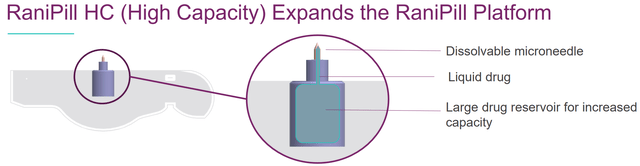

The worldwide injectable medicine’ market measurement is at present about $500B and anticipated to achieve $728B-$1251B by 2027-2032 in keeping with varied estimations (references 1, 2, 3). Clearly, many (if not most) sufferers would like a tablet in comparison with intravenous (IV) /subcutaneous (SC) supply. Subsequently, it’s not shocking that many biotechs have tried (some efficiently already) to penetrate the injectable medicine markets with oral options. Notably, the following era high-capacity RaniPill permits supply of bigger biologics, supporting RANI’s formidable purpose to turn out to be “the first-line biologics firm”.

Potential enlargement to extra biologics by the next-generation RaniPill (RaniPill HC Information Slides) Examples of indications to which RaniPill platform may very well be used. That is removed from an exhaustive listing of the chances (RANI presentation)

Overview of the expertise

There are 2 strategies to permit oral supply of injectables; (1) chemical strategies (utilized by different biotechs) that shield medicines from degradation and/or enhance absorption, and (2) oral mechanical system strategies. The primary method often leads to suboptimal bioavailability, whereas the latter (utilized by RANI) is rather more efficient and versatile.

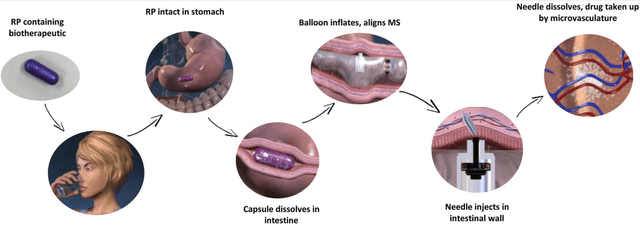

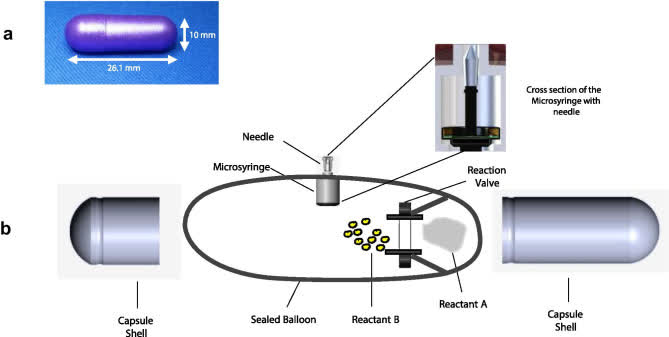

RaniPill is a robotic tablet (RP) for drug supply. The RP is a robotic auto-injector enclosed in a regular pharmaceutical “000”-sized capsule shell, enteric-coated to forestall its dissolution and deployment within the acidic setting of the abdomen. A exact dose of the biotherapeutic (payload) is packaged inside a dissolvable needle loaded inside a microsyringe, which itself is connected to a folded, self-inflating balloon. As soon as the RP reaches the small gut, the pH change dissolves the enteric coating and the capsule shell, exposing the RP to intestinal fluid. This triggers a chemical response which results in fast inflation of the balloon, which aligns the microsyringe perpendicular to the lengthy axis of the small gut, and injects the dissolvable needle carrying the drug payload into the intestinal wall. Because the gut is insensate to sharp nociceptive stimuli, the injection within the intestinal wall is painless. The present RaniPill capsule, the RaniPill GO, is designed to ship as much as a 3 mg dose of drug with excessive bioavailability. RANI can be growing a high-capacity model often known as the RaniPill HC, which is meant to allow supply of drug payloads as much as 20 mg with excessive bioavailability.

The expertise has main benefits; (1) Excessive bioavailability, (2) Agnostic to payload (can accommodate therapeutic peptides, proteins, antibodies and nucleotides), (3) Minimal discomfort, (4) Scientific information, (5) Scalable design, (6) Sturdy patent place. Related information for factors (1), (3) and (4) can be offered under in additional element.

RaniPill supply technique (PMCID: PMC8677648) RaniPill design (PMCID: PMC8677648) The upper-capacity 2nd era RaniPill will increase payload potential to as much as 20mg (vs 3mg) and permits potential supply of 90+ further drug candidates (Rani Therapeutics Company Presentation September 2023)

Proof-of-concept information for RaniPill GO

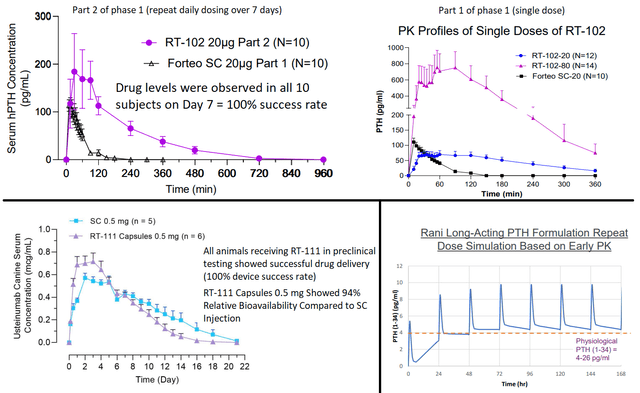

Scientific stage property embody RT-102 (oral teriparatide for osteoporosis, essentially the most superior candidate), RT-101 (oral octreotide for acromegaly/ NET tumors), RT-111 (oral ustekinumab, section 1 simply began) and RT-110 (section 1 to start out quickly). In all packages profitable supply has been proven in pre-clinical research. RT-101 and RT-102 are additional supported by section 1 information in people. Notably, “RT-102 delivered PTH with 300% to 400% greater bioavailability for 20 micrograms and 80 micrograms of PTH respectively when in comparison with 20 micrograms of Forteo delivered through subcutaneous injection.”

Chosen abstract of proof-of-concept information for RaniPill GO. Higher 2 photos; Outcomes of section 1 RT-102 research. Decrease left determine; pre-clinical outcomes of RT-111. Decrease proper determine; Simulated PK of each day RT-110 dosing based mostly on pre-clinical information. (RANI displays)

Proof-of-concept information for the next-generation RaniPill HC

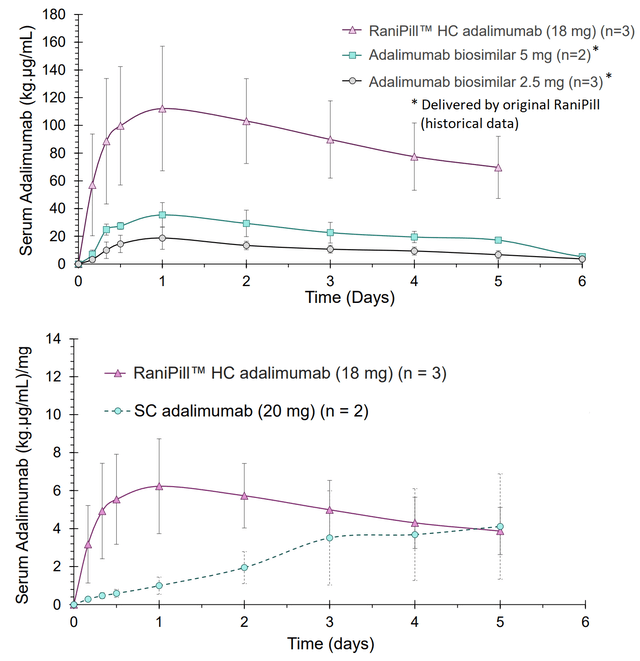

On the subject of RaniPill HC, proof-of-concept information show succesful adalimumab supply in canines, a lot improved in comparison with supply with 1st era RaniPill GO (determine). Moreover, in comparison with the subcutaneous route (present technique of supply in people) RaniPill HC confirmed greater Cmax (most serum focus) and shorter time to achieve most concentrations. For the first era RaniPill a each day dose could be essential to match PK of SC adalimumab. Information for RaniPill HC within the canine mannequin have been accessible solely as much as day 5, however clearly the mandatory frequency of administration could be a lot decrease.

RaniPill HC vs RaniPill vs SC adalimumab (in canines) (RaniPill HC Information Slides (Dec 2022))

Shallowability and tolerability of RaniPill and affected person choice in comparison with subcutaneous route

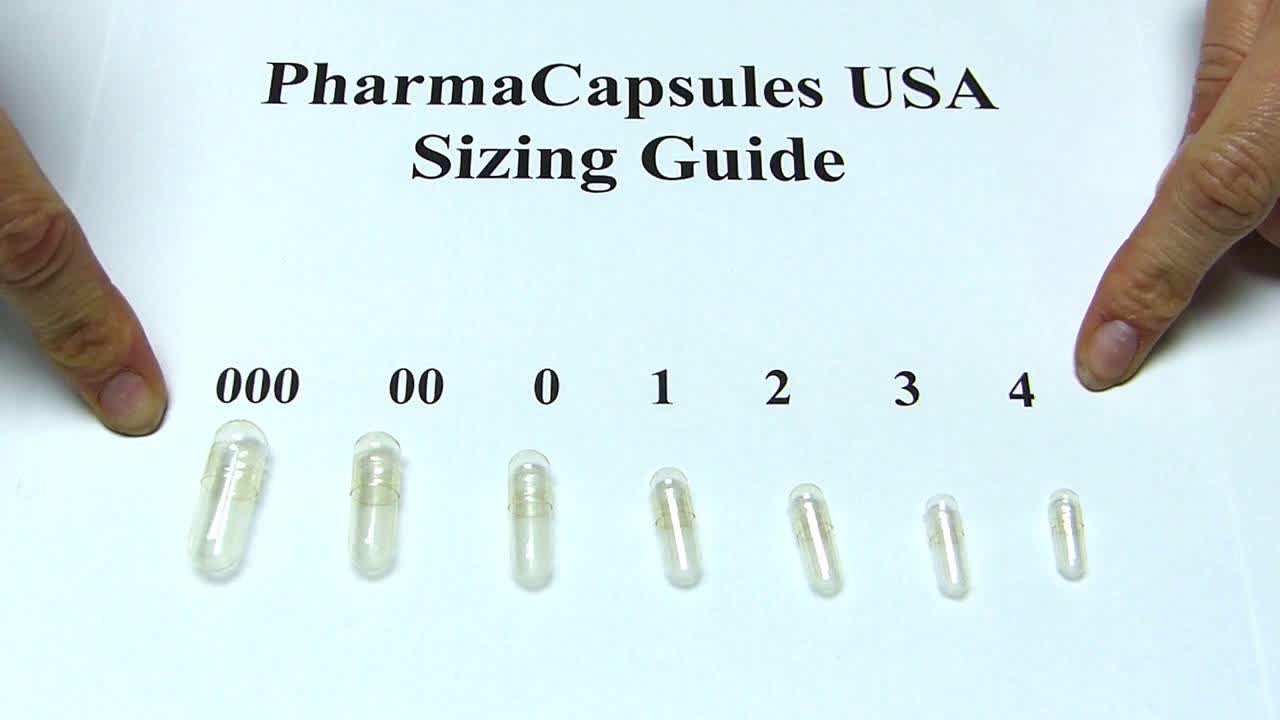

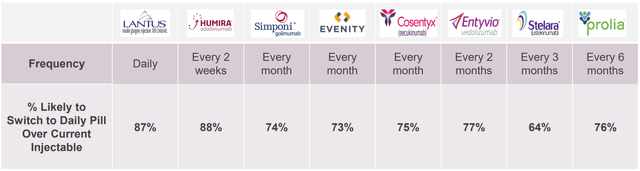

RaniPill capsule measurement is “000”, the most important for human consumption. Subsequently, I’m a bit involved concerning the tolerability of shallowing RaniPill capsule and whether or not sufferers would like this to SC injections. Fortuitously, RANI has performed analysis to deal with these considerations. Based on market analysis by RANI 87-88% of sufferers would like a each day tablet in comparison with each day/biweekly SC supply (the share drops to 64-76% for much less frequent SC administrations, i.e. each 1-6 months). Nevertheless, the outcomes of this survey are theoretical and don’t account for the tablet measurement (i.e. sufferers who participated within the survey did not really strive RaniPill).

I’m very glad that RANI has addressed the tablet measurement concern as effectively. The shallowability and palatability of mock-RaniPill (similar weight and measurement as RaniPill however crammed with potato starch) was assessed in n=50 sufferers (age vary 21-75) at present taking injections of assorted medicines (particulars of the kind and frequency of the subcutaneous injection will not be reported). All sufferers efficiently shallowed the tablet and the bulk (91%) said they would like the tablet to the subcutaneous injection.

So far as unintended effects are involved, these look like unusual. Particularly, based mostly on two section 1 research together with n=91 topics, RaniPill associated antagonistic occasions have been reported by solely 3 sufferers and have been all gentle and transient (n=2 gentle transient stomach ache, n=1 burping lasting for two days).

“Capsule Sizing Chart Gelatin Capsule Dimension Information” by Wholesome Life Provide (YouTube video) Affected person choice survey (RANI presentation)

Drug supply success charge by RANI platform

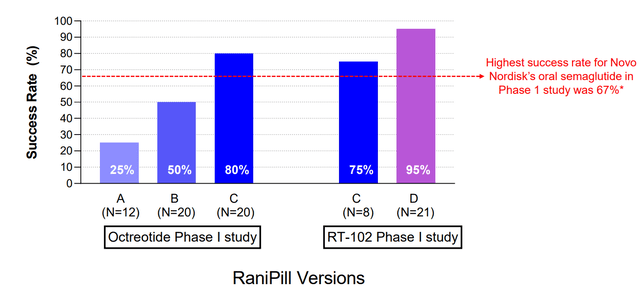

Sadly, the expertise does not at all times work as deliberate. Preliminary testing (aiming to high quality tune the product) confirmed succesful supply in 25-80% of doses. Based on RANI ‘s newest firm presentation this has improved to >90% based mostly on accessible section 1 research (for comparability, permitted oral semaglutide formulation leads to measurable absorption in 67%). Though this share appears ok it implies that sufferers could miss 1 out of each 10 doses. For each day/frequent dosing that is unlikely to trigger issues for many indications, however it may be an issue for some indications, which may restrict enlargement potential of the expertise (e.g. I would not be comfy with a affected person lacking 1 out of 10 insulin doses, if RANI have been to develop a tablet for oral supply of insulin). Moreover, lacking a dose of a long-acting agent (=much less frequent dosing, e.g. weekly/ biweekly) may have dangers. Subsequently, the potential for RANI to pursue improvement of long-acting RaniPills may very well be problematic. A plus is that system efficiency is just not affected by presence of meals.

Bettering supply success charge with later variations of RaniPill (Rani Therapeutics RT-102 Section 1 Half 2 Repeat Dose Information Slides)

Subsequent steps

Following succesful completion of section 1 research, RANI is progressing RT-102 (oral teriparatide for osteoporosis) to the section 2 stage in H2 2023. The section 2 can be a small (n= 25 Forteo SC arm vs n=25 RT-102 20μg arm) and brief (major consequence= adjustments in bone progress biomarkers at 8 weeks) research. RANI additionally plans to start out a section 1 research with RT-110 containing PTH for hyperparathyroidism.

On the subject of the injectable biologics market, RANI simply introduced initiation of a section 1 research of RT-111 (ustekinumab). The research is performed in co-operation with Celltrion. Based on the settlement; ustekinumab biosimilar (CT-P43) utilized in RT-111 is manufactured and equipped by Celltrion, RANI is granted an unique license to make use of CT-P43 within the improvement and commercialization of RT-111, and Celltrion is granted a proper of first negotiation to accumulate worldwide rights to RT-111 following a Section 1 medical trial that meets its major endpoint(s). Outcomes are anticipated in Q1 2024. Additional validating the platform’s potential RANI’s partnership with Celltrion was expended to incorporate adalimumab (RT-105) beneath an identical settlement, representing the primary partnership for the next-generation high-capacity RaniPill HC. RANI is planning initiation of a section 1 research for RT-105, which like prior section 1 research ought to have outcomes inside a couple of months following initiation. I would not be stunned if extra offers with different pharmas are introduced within the meantime, or following constructive section 1 outcomes, given the potential of RaniPill HC.

Lastly, RANI is engaged on its preclinical pipeline aiming to broaden its oral supply platform to extra molecules. E.g. RANI has already offered preclinical outcomes exhibiting bioavailability akin to SC route for GLP-1, oligonucleotides (an essential rising market) and FSH, however as already mentioned there are quite a few extra prospects.

Competitors

Contemplating the market measurement it’s not shocking that a number of different firms are pursuing penetration of the injectables market by oral options, largely by chemical strategies that are nonetheless restricted each when it comes to achievable bioavailability, in addition to when it comes to the molecules that may be delivered (technique not appropriate for bigger biologics).

Nevertheless, at the least 2 firms (talked about in RANI’s 10-Okay) are growing device-based oral drug supply;

- Novo Nordisk; Novo Nordisk is growing oral supply in co-operation with MIT. To date 2 applied sciences have been licensed from MIT, “LUMI” and “SOMA”. LUMI is just not talked about in both the 2022 Annual report or 2023 Q1-Q2 experiences of Novo Nordisk. Subsequently, solely SOMA seems to nonetheless be in lively medical improvement. Nevertheless, based mostly on accessible revealed information the capability of SOMA is far decrease in comparison with RaniPill HC, thus limiting its potential to smaller molecules. Notably, SOMA is described in NOVO’s newest annual report as a “system for the oral supply of peptides and proteins” (i.e. no point out to bigger biologics). The one candidate in medical improvement seems to be DV3395 for kind 1/2 diabetes. Based on the Q1 SEC filling “in February 2023, Novo Nordisk accomplished a section 1 trial with the DV3395 oral system idea. The trial investigated security and gastrointestinal transit of the DV3395 system, with out lively pharmaceutical ingredient. Novo Nordisk is now evaluating additional development of DV3395”. No outcomes have been revealed/introduced to my data and the candidate is just not even talked about within the newest quarterly report. LUMI expertise is just not talked about in both the 2022 Annual report or 2023 Q1-Q2 experiences.

- Biograil; Biograil is growing BIONDD. A bonus of Biograil is the smaller tablet measurement, at present at “00” with Biograil claiming being near a good smaller tablet measurement of”0″. The corporate additionally seems to have large pharma assist. Nonetheless, progress seems to be gradual and the asset continues to be within the pre-clinical stage, with no ongoing trials at the least in keeping with ClinicalTrials.gov.

Past the above 2 firms there are at the least a couple of extra firms/applied sciences I may discover (assessment article) e.g. Biora therapeutics (nonetheless within the preclinical stage, with a lot decrease money steadiness) and Baywind bioventures (preclinical stage, no latest information since 2018 within the firm’s web site).

Primarily based on the above, RANI expertise seems to be much more superior in medical improvement and seems to be progressing sooner in comparison with different firms growing device-based oral supply strategies. Nevertheless, regardless of disadvantages (primarily poor bioavailability) of chemical strategies, competitors seems to achieve success in some indications. Examples of permitted merchandise embody Rybelsus (oral semaglutide) and Mycapssa (oral octreotide), each using permeation enhancers. Notably, the latter is competing with RANI’s RT-101 pipeline, with additional a lot stronger competitors by CRNX’s paltusotine that not too long ago introduced a constructive section 3 trial. Moreover, RANI’s most superior candidate (RT-102), faces competitors by Entera bio (growing a teriparatide oral formulation at present within the section 3 stage).

To improved competitiveness RANI is engaged on a sustained launch formulation for RT-110 and RT-101 candidates. This is able to certainly be a serious industrial benefit if profitable, permitting each oral supply, in addition to much less frequent dosing vs competitors. Nevertheless, missed doses (as a consequence of failure of supply, even when rare) may very well be an issue for sustained launched formulations.

Financials

Money, money equivalents and marketable securities as of June 30, 2023, totaled $74.6M. Whole working bills have been $18.3M (R&D $11.1M, G&A $7.2M). At present burn charge RANI has money for about 4 quarters (as much as Q2 2024). Moreover, contemplating planed initiation of a section 2 and three section 1 research working bills are prone to enhance. Subsequently, RANI will very quickly want money. Hopefully, potential dilution impression can be minimized by additional progress within the pipeline and/or extra partnerships.

Main dangers forward

Regardless of the guarantees of the expertise there are main dangers for RANI;

- Variable success in supply of the payload (i.e. some doses could fail to work as deliberate, which is equal to lacking a dose). The thus far reported 90% success charge is sweet sufficient for many however not all indications which may restrict RaniPill’s potential goal markets. Nonetheless, at this charge of profitable supply I do not anticipate main issues for RANI’s pipeline.

- The selection of first indications to focus on was unlucky given success of competitors, as mentioned above. Personally, I would like RANI to focus its sources on penetrating injectable biologics markets. Regardless of competitors RANI seems to be taking all the suitable steps and has progressed a number of molecules to the clinic.

- Novo Nordisk has efficiently challenged 4 European patents, though RANI has appealed the selections. Based on RANI; “our present patent portfolio gives us with significant safety of the RaniPill expertise in Europe even other than the 4 European patents that are the topic of the present opposition proceedings. Nevertheless, if any of the present oppositions leads to a revocation or discount in our patent safety, it may encourage Novo Nordisk As or different events to hunt to invalidate or scale back further patents in Europe or different jurisdictions”.

- Capsule measurement. As mentioned above RANI analysis signifies that this does not look like an issue. Nevertheless, I wish to see extra information with long term use.

- RANI wants companions to advance its pipeline, however could fail to take action in time. Nonetheless, as said by RANI’s founder and CEO “as we generate extra information, I feel there’s a potential that pharma firms can be much less inclined to allow us to compete towards them versus working with us”. Subsequently, given outcomes thus far I anticipate RANI with the ability to kind extra partnerships quickly.

- RANI inventory value has been in a gradual downward pattern and has a “sturdy promote” quant score. Subsequently, there could be a greater (or at the least safer) entry level to start out shopping for the inventory.

Conclusion

The upside potential for RANI if profitable is big as it might probably disrupt a number of multi-billion greenback markets (even 1% penetration of those markets would equate to >$5B income). Notably, RaniPill (each the first era and the 2nd era higher-capacity tablet) has been confirmed to be an efficient and well-tolerated oral supply technique for varied molecules (together with bigger biologics, like monoclonal antibodies) in each pre-clinical and early-phase medical research, thus considerably de-risking the platform. Nevertheless, contemplating fierce competitors, challenged patents in Europe, giant tablet measurement, inconsistent payload supply, very early stage in medical improvement (a few years forward of potential commercialization), money steadiness and working bills there are main dangers forward. For my part, most promise comes from next-generation high-capacity capsules that enables supply of bigger biologics, an enormous goal market. The inventory has been crushed down not too long ago and beginning constructing place could be price it, so long as potential traders perceive the dangers and have a long-term perspective. Personally, regardless of above dangers, I are typically optimistic. I see RANI as a speculative long-term funding with uneven risk-reward and I’m keen to carry for a number of years.

Your suggestions is appreciated

Please remark under in case you have any suggestions (unfavorable or constructive), should you spot any errors or should you consider I missed one thing essential within the article.