Laurence Dutton

Funding motion

Primarily based on my present outlook and evaluation of PTC Inc. (NASDAQ:PTC), I like to recommend a purchase ranking. I imagine the long-term progress outlook for PTC could be very constructive given its publicity to key progress verticals. I anticipate the underlying industrial firms to ultimately undertake these superior technological options as they compete with their friends to turn into extra productive and cost-efficient, and PTC is well-positioned to seize these calls for.

Primary Info

PTC is a software program resolution supplier for purchasers in industries which might be heavy in design, manufacturing, and undertaking administration. The three predominant options that PTC gives are computer-aided design (CAD), product lifecycle administration (PLM), and augmented actuality (AR). PTC has additionally lately entered the Web of Issues (IoT) vertical. The enterprise reporting is segmented into three components: recurring income, perpetual licenses, {and professional} providers. The recurring income section is the biggest of the three, representing 91% of FY23 income. f

PTC

Publicity to rising verticals

PTC has a protracted runway of progress forward given its publicity to rising verticals: CAD, PLM, AR/IoT.

First, let’s discuss in regards to the CAD market. As a bit of background, CAD is software program that was developed to boost the design course of by making it extra environment friendly, higher organized, and extra documented. It additionally launched the flexibility to iterate. By basically automating the once-manual means of drawing and design calculations, CAD tremendously enhances effectivity. For sectors like building and civil engineering, the place large-scale initiatives necessitate quite a few revisions and nil tolerance for error, the worth proposition is thus exceptionally compelling. In response to third-party analysis, the worldwide CAD market is predicted to proceed rising at mid-single-digits for the approaching decade. For my part, progress goes to be increased than mid-single-digits due to AI, because the infusion of AI into CAD considerably enhances productiveness, which might scale back the general value of initiatives.

PLM is the following enticing market that PTC has publicity too. To supply some background, PLM software program makes it simpler for purchasers to streamline their design and manufacturing processes by centralizing and organizing the entire necessary product information generated throughout the growth course of. Primarily, PLM aids purchasers in lowering bills, simplifying processes, and shortening lifecycles. As applied sciences like AR and the Web of Issues achieve traction, PLM performs an more and more necessary position in making info extra accessible throughout organizations, which in flip improves the effectivity of engineering and manufacturing processes. With the assistance of IoT (extra under) sensors, PLM can cowl extra floor than simply product growth and now encompasses the entire product lifecycle. As the quantity of knowledge, documentation, specs, and computations related to initiatives continues to rise together with the sophistication of the underlying fashions, I foresee a rising demand for PLM within the years to come back.

Touching extra on IoT, it’s the usage of software program options to hyperlink extra industrial and manufacturing machines and crops for the aim of accelerating information aggregation, reducing manufacturing threat, and enhancing effectivity and productiveness. In contrast to consumer-based IoT merchandise, I imagine industrial IoT merchandise have much more worth as they’re a more cost effective resolution that may be included throughout crops and factories moderately than having staff do checks on a periodic foundation (which is inferior to the 24/7 surveillance that IoT can present). This Because of this, information aggregation has turn into much more necessary, as companies want these information to boost their digital twins and get extra worth from them by way of superior information evaluation. The best way I see it, IoT has turn into a desk stake for industrial firms. They should ultimately implement IoT options (solely 60% are utilizing IoT now) as a way to keep aggressive on value and productiveness, and PTC is right here to choose up share.

Lastly, I’ve a powerful perception within the demand inside the augmented actuality vertical. With regards to industrial firms, augmented actuality permits for extra sturdy coaching applications that optimize workforces by lowering onboarding necessities and enhancing early success charges. Companies may also achieve a aggressive edge with industrial AR software program by creating and projecting augmented actuality coaching directions into industrial settings like crops and factories.

Robust partnership improve distribution capability

A very good product requires a powerful distribution technique to drive progress; if not, it’s only a good product. Happily, administration has gotten this a part of the expansion equation proper as effectively. As a part of the hassle to transition right into a subscription enterprise mannequin, PTC invested closely in its go-to-market group, with a deal with being a buyer success group that’s constructed round a buyer success supervisor. Whereas PTC doesn’t disclose the precise renewal charges, from the transcripts, we are able to inform that renewal charges have been robust, which is a sign that the GTM technique is working. I additionally spotlight that this GTM mannequin works very effectively for the character of PTC merchandise, which have a protracted period because of the underlying industrial undertaking durations; therefore, it provides PTC a number of alternatives to upsell new merchandise and options that may make life simpler for its purchasers. Apart from that, PTC additionally has three vital partnerships, one every with trade leaders Microsoft, Rockwell Automation, and Ansys. Of the three, I feel the partnership with Microsoft goes to be a key one, as PTC can leverage the MSFT world enterprise gross sales pressure to promote PTC cloud-based merchandise linked to MSFT’s Azure IoT Hub for ingesting information.

Trying over the near-term efficiency (FY24)

The expansion momentum continues to be robust as administration reiterated a continuing foreign money ARR of $2.19 billion to $2.25 billion, implying a progress fee of 11 to 14%. This steerage additionally implies that PTC progress is again to a extra normalized degree, consistent with its pre-covid progress vary of low-teen percentages. Income steerage can be reiterated at $2.27 billion to $2.36 billion, implying a progress fee of ~10%. The income information reiteration is important as a result of it implies that normalized progress (I take advantage of the time period normalize right here as a result of ARR is trending again in direction of a normalized vary) is now above the ten% threshold, a degree that PTC has failed to realize outdoors of the COVID interval (FY20/21).

There are a variety of qualitative indicators that progress goes to be sturdy sooner or later as effectively. For instance, PTC’s on-premise Windchill programs are nonetheless within the early levels of being the client base’s central repository for product information. ServiceMax and ALM (software lifecycle administration) led by Codebeamer and augmented by PureVariants are two extra cross-selling alternatives for PTC. The previous tremendously improves PTC’s SLM (service lifecycle administration) portfolio and permits PTC to supply an entire resolution for optimizing service processes. Extra alternatives embody increasing CAD and shifting to SaaS for all merchandise. These two paths will cross paths to a sure diploma as PTC sees Creo prospects transitioning to Creo Plus, a SaaS providing much like Windchill Plus.

In order we talked about, I feel final earnings name, we have been seeing Codebeamer as a tip of the spear, the place we’re significantly in automotive suppliers, the place now we’re getting within the dialog as we’re displaying them the Codebeamer worth prop.

A second cross-sell alternative is ServiceMax. We acquired ServiceMax in January 2023, and the strategic match with PTC is strong. For a lot of of our prospects, rising the providers enterprise is their high precedence.

Clearly, persevering with to develop CAD and changing our put in base over to SaaS throughout all merchandise are two extra alternatives, which overlap to some extent as a result of we’ll see conversion of Creo prospects to our Creo+ SaaS providing over time, very similar to Windchill+. 1Q24 name

Valuation

Creator’s work

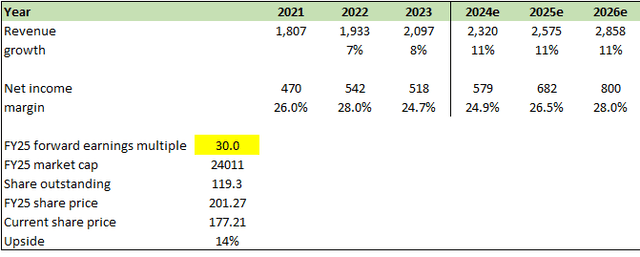

I imagine PTC can develop at 11% for the approaching 3 fiscal years because the influence of COVID lastly goes away, permitting it to indicate its normalized progress, which I imagine administration has guided. Supporting this progress are a number of progress drivers inside the CAD, PLM, AR, and IoT markets that I anticipate to see steady demand within the coming years as industrial firms must leverage these applied sciences to turn into extra productive on each value and effectivity fronts. As PTC scales its income, it must also drive margin growth because it has a excessive incremental margin, which will be seen from the growing EBIT margin (from 20% in FY19 to 36% in FY23). I might additionally notice that friends like Dassault Systemes and Autodesk have internet margins of 18% and 17%, respectively, so there are precedents for PTC to proceed increasing margins. In figuring out the fitting a number of for PTC, I benchmark its fundamentals in opposition to the identical friends (Dassault Systemes and Autodesk). Each friends have an analogous progress outlook however increased margins and a greater stability sheet profile. As such, I feel PTC ought to commerce at a reduction to them. I assumed PTC to commerce at 30x, which is a 1x low cost vs. Autodesk and in addition its personal historic common.

Threat and ultimate ideas

Demand for PTC options is not directly impacted by the macroeconomic state of affairs. In a recession, there may be prone to be fewer new building actions and initiatives as purchasers take a risk-off method (keep away from large capital outlay with tender financial outlook, and weak pricing setting), which implies there’s a lesser want for PTC options (lesser want for CAD, as an illustration). Whereas the product is sticky due to all the info mixed, companies might look to downsize their wants (i.e., scale back tier), thereby impacting ARPU for PTC.

All in all, I like to recommend a purchase ranking for PTC given its robust publicity to key progress verticals. PTC’s strategic partnerships and a strong distribution technique are key elements that helps PTC to seize demand. Primarily based on administration steerage, near-term efficiency for FY24 displays a return to normalized progress ranges, and a good outlook. I anticipate PTC to see progress of low-teens over the following three fiscal years, pushed by ongoing demand in key markets and potential margin growth.