CatEyePerspective

Introduction:

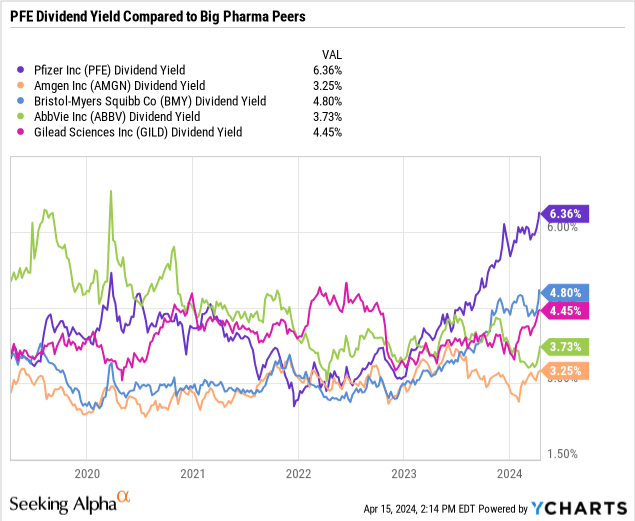

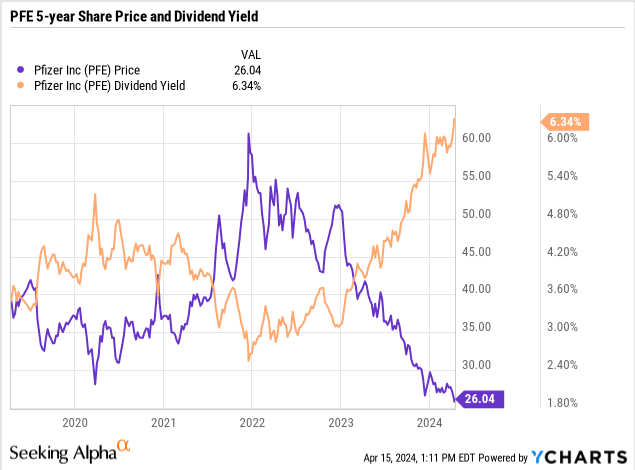

A biotech inventory with a big dividend is fairly unusual since biotechnology and pharmaceutical firms are inclined to focus extra on reinvestment into pipeline development fairly than shareholder returns. However as a biopharma grows bigger and there could also be a paucity of potential pipeline or partnership alternatives that could be price investing in, the corporate might look to return a few of its earnings to its buyers by both dividends or share repurchases. Pfizer (NYSE:PFE) appears to be one in all these firms, the place the mix of current share value declines and a steadily rising dividend had induced the corporate’s yield to eclipse the 6% stage.

Bristol-Myers Squibb (BMY) is one other firm with the next dividend yield, however one with some challenges as a result of upcoming losses of patent exclusivity for key merchandise. I’ve seemed into BMY in nice element, mentioned right here. To make a conclusion about investibility of PFE, I am going to take into account some comparable views. potential key at-risk product income, potential income development, and dividend sustainability/debt, PFE looks as if it could be a worth inventory with the potential to rebound as a result of overcoming of potential income declines. Whereas I do not at the moment personal shares, it is going to be one on my watchlist that I would take into account with a average “purchase” ranking. I am not contemplating a powerful “purchase” ranking right here, as there are potential danger components surrounding the efficacy-related efficiency of a number of the firm’s COVID merchandise which will probably emerge sooner or later as a headwind.

COVID-19 Rise and Fall:

Earlier than 2020, PFE was largely targeted on producing breakthrough therapies, largely in uncommon illnesses and oncology, in addition to the divestment of their generic and off-patent branded phase Upjohn. The corporate moved in a measured method, befitting an enormous pharma, making regular and strategic acquisitions to develop the place they noticed essentially the most accretive applications.

That modified in 2020 as PFE partnered with BioNTech (BNTX) to codevelop a vaccine for COVID-19. In what was then a foray into an virtually science-fiction-like expertise as no mRNA-based vaccine had but been efficiently deployed, PFE and BNTX (and naturally Moderna (MRNA) individually) put forth large efforts to convey their vaccine to market, and administered lots of of tens of millions of doses over the course of the pandemic. This produced a windfall for PFE, as nations bought huge quantities of vaccines to distribute to their populations.

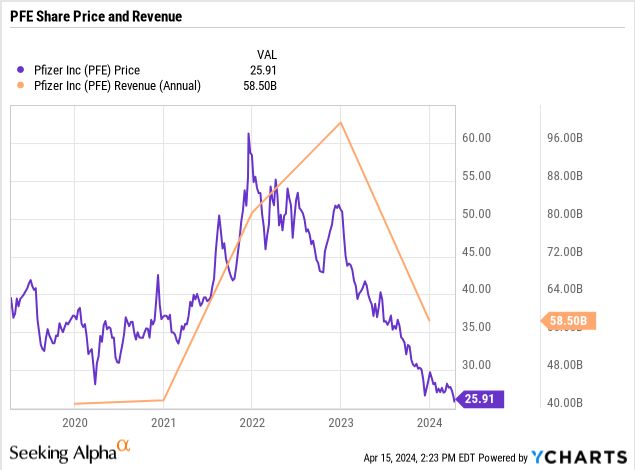

Throughout 2020-2023, PFE had a complete new phase added to its income: COVID-19 and associated merchandise, bringing firm biopharma-only income from ~$38B in 2019 (adjusting from Upjohn separation), to a peak of $99B in 2022. This meteoric improve was pandemic-fueled, however has given method to an inevitable decline following the downgrade of COVID-19 from pandemic standing because the globe recovered.

Because the pandemic subsided, income subsequently precipitously dropped, analysts confirmed their disappointment, and PFE’s inventory value adopted swimsuit. The corporate now has income from COVID merchandise at additional danger from decline in illness significance, in addition to some key merchandise with probably looming losses of exclusivity. That mentioned although, when contemplating the COVID/con-COVID product income cut up, the non-COVID income appears to be rising reasonably at a median annual price of ~4%.

PFE Income Breakdown (PFE Company Supplies)

This ~4% is optimistic, however not essentially spectacular, so might have performed an element in PFE’s resolution to sink a few of its COVID windfall into buying Seagen in 2023, hoping to drive development in oncology for the corporate. The acquisition was anticipated to contribute ~$10B in risk-adjusted income by 2030, which may go a great distance in offering a lift to firm development.

What Income Is perhaps at Threat?

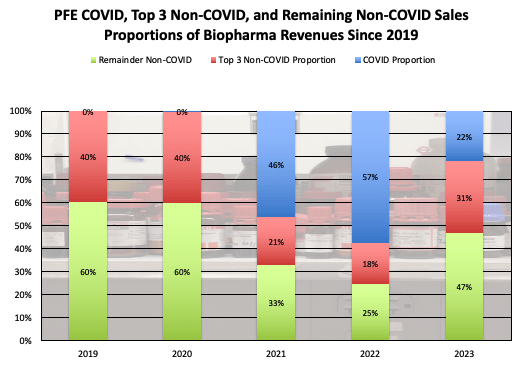

To think about a number of the potential declines that PFE could also be going through, there are 2 key segments to look extra carefully at. Considered one of course is the COVID-related merchandise, which comprise 22% PFE 2023 income. The opposite to contemplate are the highest 3 non-COVID merchandise, and the upcoming LOE (losses of patent exclusivity). In 2023, the highest 3 non-COVID merchandise (Eliquis, Prevnar, and Ibrance) made up ~30% of the corporate’s income, with some LOE occurring earlier than 2030.

Desk 1: PFE Whole Biopharma Revenues and Key Merchandise ($M)

|

Drug |

LOE |

2023* |

Proportion of FY2023 Income |

|

Comirnaty** |

2041 |

11,220 |

20% |

|

Paxlovid** |

2041 |

1,279 |

2% |

|

Eliquis |

2026 |

6,747 |

12% |

|

Prevnar |

2026/2033 |

6,440 |

11% |

|

Ibrance |

2027 |

4,753 |

8% |

|

Whole |

57,186 |

53% |

*Biopharma gross sales solely, excluding manufacturing partnership income; **COVID-dependent gross sales

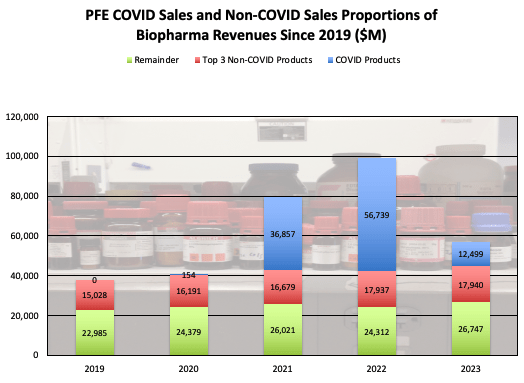

COVID-19 product income shall be thought of first. COVID merchandise have had a huge effect on PFE income since 2020, rising to almost 60% of firm biopharma income in 2022.

PFE Trailing Income Proportions (PFE Company Supplies)

The COVID contribution to PFE has declined considerably since then, nonetheless, and should proceed declining additional as COVID impression has continued to say no. The 2023 ranges of COVID income contribution had been ~$11B from their COVID vaccine Comirnaty, and ~$1.3B for Paxlovid. We’ll deal with Paxlovid first, which was initially seen as an efficient therapy for lively COVID-19, however has not too long ago proven solely questionable efficacy in some COVID-19 affected person segments. The decline in COVID-19 from pandemic standing to endemic (not overwhelming hospital programs, and now often occurring equally to a seasonal flu) mixed with a number of the less-stellar medical efficacy outcomes of Paxlovid might end result within the continued decline of the therapy gross sales, maybe as little as $500M annual gross sales. This estimate accounts for the CDC’s lifting of COVID isolation pointers and lowered hospitalizations and deaths, whereas recognizing there could also be some higher-risk sufferers that also discover want for the therapy. Comirnaty revenues might have additional declines as properly. The scenario of fast development over a brief timeframe skilled by PFE appears just like Gilead Sciences’ (GILD) success in Hepatitis C therapy almost a decade in the past. GILD’s HCV revenues soared on the launches of Harvoni and Solvaldi in 2013 and 2014, peaking in 2015 at ~$19B. Nevertheless as GILD handled many of the readily-presenting sufferers, their income plummeted over the subsequent 5 years by ~90% to ~$2B in 2020, the place it has largely stabilized, solely declining barely to ~$1.8B in 2023. Utilizing this identical estimate, PFE peak Comirnaty income was seen peaking in 2022 at ~$38B. A ~90% decline right here over the subsequent a number of years would put potential gross sales by ~2030 at ~$4B. This could be ~$7B potential decline from the 2023 income. On high of one other potential $700M decline from Paxlovid, there could also be probably ~$7.8B in future income declines for PFE’s COVID-19 phase by 2030.

PFE Prime 3 Non-COVID Drug Potential LOE Impacts:

PFE’s high 3 non-COVID merchandise in 2023 had been Eliquis (comarketed with Bristol-Myers Squibb ((BMY))), Prevnar (pneumococcal vaccine line), and Ibrance (for some sorts of breast most cancers). Collectively the three merchandise made up ~31% of 2023 revenues, and every is ready to lose some patent exclusivity in 2026 or 2027. The best one to deal with is Eliquis, as we have lined it in our earlier BMY LOE article (if you happen to learn it, many thanks). As a refresher, Eliquis is a small molecule drug, and people might decline ~80-90% from peak gross sales, when generic competitors enters the market and the branded merchandise lose pricing premium. BMY’s topline income for Eliquis contains the portion of income that shall be paid to PFE in alliance income, and we beforehand calculated Eliquis’ potential ahead development price utilizing the next: the compound annual development price of Eliquis gross sales from 2018 has been ~14%, however could also be a bit excessive to only carry ahead by 2026, as a result of scale of the therapy. To account for more moderen development charges, 2023 Eliquis development was ~4% over 2022, down from the ~10% development seen from 2021 to 2022. It could be affordable to forecast the Eliquis gross sales development at a price of ~6-7%, accounting for the newest development durations. After all we shall be assuming no change to the PFE/BMY Eliquis partnership phrases, or any potential impression to Eliquis costs from CMS negotiations as a part of the Inflation Discount Act.

Desk 2: Forecast Progress of Eliquis By way of 2026 (M USD)

|

2023 |

2024 |

2025 |

2026 |

Put up-LOE |

|

6,747 |

7,188 |

7,658 |

8,159 |

1,632 |

Supply: PFE, BMY Company Supplies; Projections by Writer

Based mostly on these estimates, it could be doable that there’s ~$5B in income for PFE in danger for LOE erosion for Eliquis.

Ibrance Erosion Potential:

PFE’s Ibrance is a small molecule inhibitor of CDK (cyclin-dependent kinase) 4 and 6, and is used to deal with HR-positive and HER2-negative breast cancers. It is a small molecule oncology drug, so we’ll use the identical estimates of small molecule LOE erosion as above: ~80% potential erosion following LOE. Income has been beneath some strain as a result of competitors, and a few value decreases in worldwide markets. To mirror this development, the compound annual development price from 2019 for Ibrance has been just below 1%. If this development continues, then it could seem that Ibrance’s peak income occurred in 2021 at ~$5.4B. An 80% decline from this level could be ~$1.1B following LOE, which is ~$3.7B decrease than 2023 gross sales.

Prevnar LOE Impression:

Prevnar is a sequence of pneumococcal vaccines that Pfizer (and beforehand Wyeth earlier than the 2009 acquisition by PFE) has been advertising and marketing for over 20 years. The protection of this vaccine has been bettering, from focusing on 7 viral variations, to 13 types, to the newest iteration focusing on 20 viral types. Whereas Prevnar 13 LOE hits in 2026, Prevnar 20 LOE does not happen till at the least 2033. As the corporate transitions previous potential LOE impression of Prevnar 13, it is possible that Prevnar 20 will proceed to develop and incorporate potential misplaced gross sales from Prevnar 13, as Prevnar 20 accommodates the performance of Prevnar 13, whereas incorporating immunization towards 7 extra viral variations. The LOE impression earlier than 2030 for PFE’s Prevnar household will possible be minimal, and is probably not a major danger of firm income, as PFE seems to be frequently updating the product line to keep up competitiveness and profit for sufferers. So of the top-selling 3 merchandise and remaining COVID-19 strains, PFE has probably ~$7.8B from COVID strains and one other ~$8.7B in non-COVID high 3 income at potential danger by 2030.

Desk 3: PFE Potential Revenues at Threat for 2023 Prime-Promoting 3 and COVID-19 Merchandise

|

Drug |

LOE |

Peak Income |

Put up-LOE/Loss Income Degree |

Potential Erosion in comparison with 2023 income |

|

Comirnaty |

2041 |

37,806 |

4,077 |

7,143 |

|

Paxlovid |

2041 |

18,933 |

579 |

700 |

|

Eliquis |

2026 |

8,159 |

1,632 |

5,115 |

|

Prevnar |

2026/2033 |

Not earlier than 2030 |

N/A |

N/A |

|

Ibrance |

2027 |

5,437 |

1,087 |

3,666 |

Supply: PFE, Company Supplies; Projections by Writer

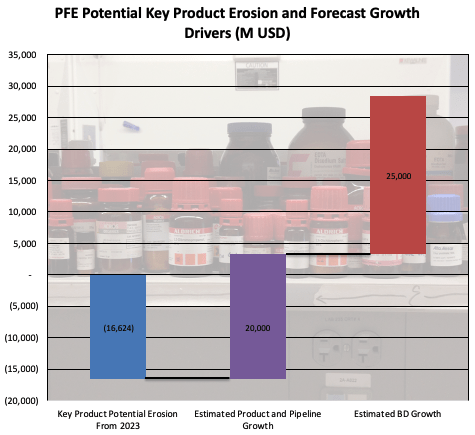

PFE is going through probably as much as ~$16.6B in income in danger from key merchandise, which can clarify the overall lack of enthusiasm from analysts and buyers that has introduced the corporate’s share value to its present lows. The corporate should make up the shortfalls by the mix of Seagen or different acquired belongings, and its present medical pipeline.

PFE Potential Future Progress:

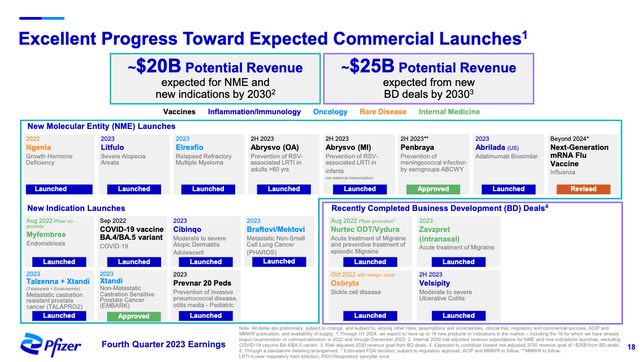

Whereas PFE accomplished the Enviornment Prescribed drugs acquisition in 2022, it was solely on the dimensions of ~$6.7B, and a much less probably transformational transaction than the $43B buyout of Seagen. The Biohaven acquisition additionally accomplished in 2022 for ~$11.6B, however Seagen as the biggest appears essentially the most vital. PFE has estimated that Seagen merchandise will enhance PFE revenues considerably, and $3.1B of that in 2024. We may attempt to analyze PFE’s pipeline ourselves and would in all probability get an honest approximation of the potential income development by 2030, however PFE has accomplished these forecasts themselves, and have been type sufficient to share the excessive stage views of their This fall 2023 presentation.

PFE Income Forecasts (PFE Company Supplies)

A mixed ~$45B in new income by 2030 is estimated by PFE (accounting for all applicable chances of medical success ), from numerous pipeline applications and up to date and new enterprise improvement offers, together with these from Enviornment, Biohaven, and Seagen. Assuming these merchandise obtain the degrees of success PFE has estimated, the corporate will be capable to handily overcome the potential estimated LOE and COVID-related potential erosion by 2030.

PFE At Threat Income and Income Progress (PFE Company Supplies, Chart and Erosion Estimates by Writer)

This seems to be fairly good for PFE, so relying on the timing of launches and product development, their income development potential seems possible to have the ability to outweigh the important thing potential destructive income strain confronted from the reported 2023 information.

Dividend Payout:

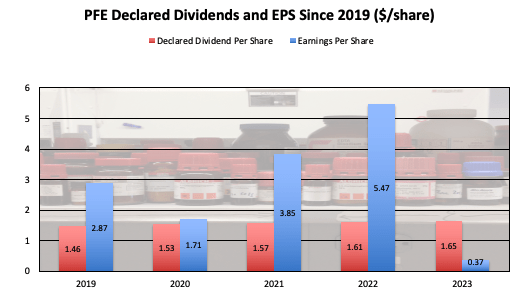

On the present stage, the dividend is one thing that may be inspected additional. Over the previous a number of years, the dividend appears to have been well-covered, aside from 2023’s decline that was largely associated to decreased COVID phase gross sales.

PFE Dividends and EPS (PFE Company Supplies, Chart by Writer)

It ought to be watched transferring ahead, however as PFE’s revenues enhance from different applications, EPS is probably going to enhance as the corporate right-sizes its operational scale.

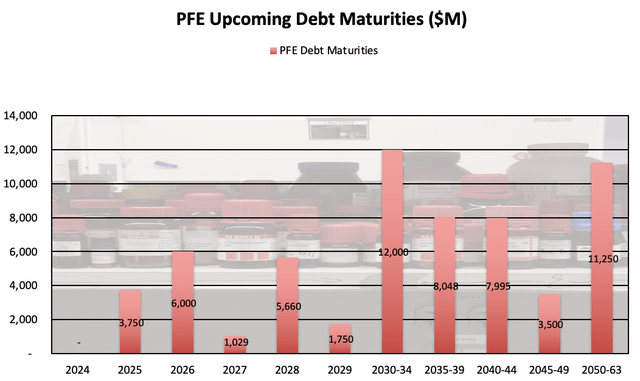

Debt Ranges:

PFE debt can also be price a more in-depth look, as the corporate has spent vital funds on acquisitions over the previous a number of years. Whereas the corporate holds ~$12.6B in money, equivalents, and quick time period investments, PFE’s short-term borrowings and debt of ~$10B and long-term debt of ~$62B advantage a detailed watch as properly. The maturities for long-term debt are pretty well-laddered, with manageable maturities earlier than 2030.

PFE Long run Debt Maturities (PFE Company Supplies)

Whereas this debt actually will have to be addressed, it appears to be one thing the corporate will be capable to deal with.

Last Ideas:

Because the COVID-19 pandemic has receded, PFE’s COVID-related income has likewise fallen, bringing concerning the unlucky decline in share costs. That mentioned, it could seem that many of the principal income declines have already occurred for PFE’s COVID-related merchandise. PFE’s different key merchandise the place LOE is imminent have some vital potential losses to contemplate, however PFE’s forecast development for its present pipeline in addition to potential development from BD transactions might fairly outweigh the potential at-risk income. General it could seem that PFE’s income will possible start to rise past a number of the key losses, and with a income rebound, a share value rebound could also be doable. Mixed with a excessive dividend that will look like largely sustainable, the shares could also be price buying. I might take into account them to be a average “purchase” right here, and can maintain them on my watchlist to probably purchase shares when in a position.

Potential Threat Components:

Whereas the basics for PFE appear steady and able to a return to development, there are a pair components stopping me from ranking a stronger purchase. Paxlovid efficacy was not clearly demonstrated in comparison with placebo in lower-risk sufferers, though security was reiterated. This may increasingly probably restrict future addressable affected person populations. Moreover reviews of “Paxlovid rebound”, or return of COVID-19 signs in some sufferers who taken Paxlovid and noticed symptom restoration, might additional impression potential sufferers’ notion of Paxlovid, and proceed to restrict the addressable inhabitants.

Comirnaty has had some challenges as properly adapting to an evolving pandemic scenario. When initially launched in late 2020, the vaccine confirmed ~96% efficacy towards hospitalization or demise after the 2nd dose, in Alpha variant COVID-19 sufferers. Nevertheless, because the virus started to mutate, the efficacy adjusted accordingly.

Desk 4: Comirnaty Efficacy Towards A number of Main COVID-19 Variants

|

Variant: |

Efficacy in adults towards symptomatic COVID-19 an infection following the 2nd dose |

|

Alpha |

89% |

|

Beta |

87% |

|

Gamma |

88% |

|

Delta |

84% |

|

Omicron |

15% (BA.1 subvariant); 28% (BA.2 subvariant) |

Supply: Int. Immunopharmacol.

This displays the problem of utilizing a newly-successful expertise after a fast development by the medical trial course of throughout a time of worldwide pandemic impression. Nevertheless, there could also be some that query the decline, and should probably be a goal of litigation, just like a comparatively current problem from the state of TX.

Moreover, whereas most uncomfortable side effects encountered had been delicate, there have been some accounts of myocarditis or pericarditis (coronary heart muscle or outer lining irritation, respectively) which have occurred in sufferers. Given the potential seriousness of those latter occurrences, there might probably be challenges to PFE right here. Whereas vaccine producers are typically not answerable for damages in civil actions which might be associated to a vaccine damage/demise, extra protections had been prolonged to guard PFE and MRNA from vaccine side-effect-related lawsuits till at the least this 12 months. My warning right here will not be that PFE could also be liable to potential lawsuits relating to probably reported uncomfortable side effects that could be vaccine-related. My warning is that it’s a political/governmental safety prolonged to PFE right here, and as such, the winds of politics shift regularly. Relying on potential future shifts, there could also be sentiments that permit future motion towards PFE, MRNA, or different firms that contributed to the vaccine-related push throughout the COVID-19 pandemic. Whereas this can be a distant probability that doesn’t impression my consideration of PFE as a “purchase”, it is this potential that causes me to keep away from a powerful “purchase” consideration for PFE.

{kind=link}