")

kontrast-fotodesign

After writing about Clear Power Fuels (NASDAQ:CLNE) and Montauk Renewables (NASDAQ:MNTK), in the present day’s article focuses on OPAL Fuels (NASDAQ:OPAL), a U.S. firm that operates vertically within the RNG market having each of the above firms as its most important rivals. In recent times OPAL has made an intensive funding marketing campaign to extend its RNG manufacturing, together with by changing renewable energy vegetation into RNG manufacturing services, in addition to upgrading its community to 298 gasoline stations within the U.S. as of December 2023. The RNG market is characterised by growing competitors, however I imagine OPAL may set up itself as one of many leaders due to its extraordinarily verticalized enterprise. Regardless of this, OPAL remains to be characterised by low working money circulation era in comparison with rivals in addition to greater debt and excessive threat of capital dilution. Contemplating these and different dangers analyzed in extra element within the article, in addition to the result of my Discounted Money Circulation mannequin, I presently assign to OPAL a Maintain ranking. If on this planet of renewable vitality, on EuroEquity Analysis you may discover a number of analyses of firms working in it.

Enterprise Overview

Demand for RNG is predicted to extend within the coming years each globally and within the US. IEA information spotlight potential development of 20% between FY23 and FY28. As well as, new technological developments corresponding to Cummins’ 15l engine may symbolize a major improve in RNG use with optimistic results on total biofuel demand. Inside this extremely dynamic ecosystem, OPAL Fuels operates inside three particular enterprise areas: RNG Fuels, Gasoline Station Providers and Renewable Energy.

OPAL SEC Filings and Creator’s Evaluation

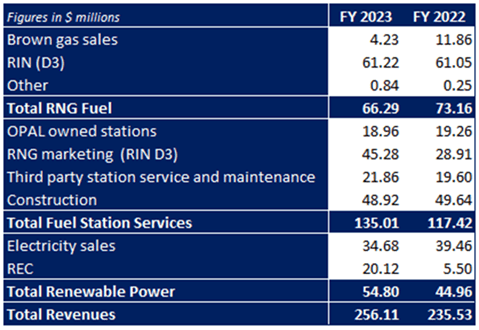

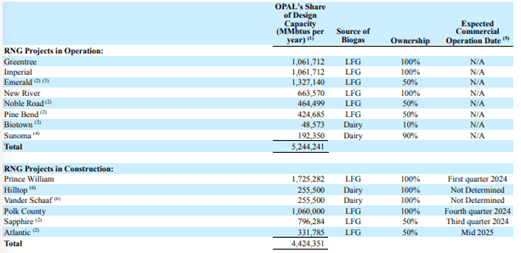

RNG Fuels offers with the manufacturing of RNG obtained from landfill, livestock waste and natural waste. As of December 2023, it has manufacturing of two.7 MMBtus obtained via 8 vegetation in operations, up from 2.2 MMBtus in FY22. In FY24, administration expects manufacturing of 4.4-4.8MMBtus. OPAL has reached 5.2 MMBtus when it comes to manufacturing capability, to which 4.4 MMBtus needs to be added by the second half of 2025, together with 1.7 MMBtus from the conversion of the Prince William renewable energy manufacturing vegetation. In FY23 the section produced 25.9% of complete revenues, down from 31% recorded in FY22 on account of lower in volumes associated to brown gasoline gross sales. 92.5% of RNG fuels revenues are derived from the cellulosic biofuel

RIN (D3).

OPAL Annual Report FY23

Gasoline Station Providers is engaged within the building and O&M of gasoline stations for third events, in addition to its personal. In finishing up its actions, OPAL can also be concerned within the administration and monetization of environmental credit. In FY23 it operates via 298 stations, up from 137 in FY22 and 68 in FY21, highlighting the corporate’s deal with this market section, which in actual fact is value 52% of complete revenues in FY23. Digging even deeper, 14% of the section’s income got here from owned stations, 16% from third -party station O&M, 36% from EPC exercise, and 33% from environmental credit. In FY23 the section skilled a 15% YoY development, virtually fully attributable to development in environmental credit revenues from $28.9m in FY22 to $45.3m in FY23.

Renewable energy engages in electrical energy era from biomethane for a nameplate capability of 112MW, anticipated to lower as early as FY24 as a result of conversion of Prince William I and II vegetation to RNG services. In FY23 it’s value 21.4% of complete revenues, up 21.9% YoY, attributable to elevated revenues from RECs (Renewable Power Certificates). Though it nonetheless constitutes a large chunk of revenues, it’s now not the main target of the corporate’s initiatives, as will be seen by the close to absence of investments within the section in comparison with these made in gasoline stations and RNG services.

OPAL Annual Report FY23

A Comparability with MNTK and CLNE

As evident within the enterprise overview, OPAL stands out as considered one of Montauk’s most important rivals in RNG manufacturing and considered one of Clear Power Fuels’ most important rivals in gasoline station building and O&M. Particularly:

MNTK produced 5.5 MMBtus of RNG in FY23, flat YoY, in comparison with 2.7 MMBtus produced by OPAL. When it comes to renewable energy, OPAL’s put in capability is considerably greater than Montauk’s, with 112MW versus Montauk’s 30MW. Furthermore, OPAL outperforms its competitor each when it comes to development perspective and Capex investments, though the distinction seems to be lowering primarily based on FY24 estimates. Lastly, an important distinction issues the overall focus of MNTK’s enterprise in RNG and renewable energy manufacturing, in comparison with OPAL additionally energetic in EPC and O&M of gasoline stations.

OPAL has 298 gasoline stations between owned and third-party services in FY23, promoting 44m GGEs of RNG up from 29m offered in FY22. CLNE quite the opposite, along with having extra owned stations, operates over 600 service stations for a complete of 225m GGEs offered in FY23, up from 198m in FY22. Regardless of decrease gross sales volumes, OPAL has a a lot greater RNG output than CLNE, which started to put money into RNG manufacturing solely since FY21, primarily via Joint Ventures, with very small volumes in the interim.

In consideration of the above, OPAL appears among the many three firms to be the one greatest positioned to realize full market verticalization, with the potential of creating synergies when it comes to each revenues and prices. This dynamic additionally appears to be thought of by the market, which assigns greater multiples for OPAL than for MNTK and CLNE. However, OCF’s greater debt and decrease output in comparison with them partly counterbalance the valuation.

Commentary on monetary and financial outcomes

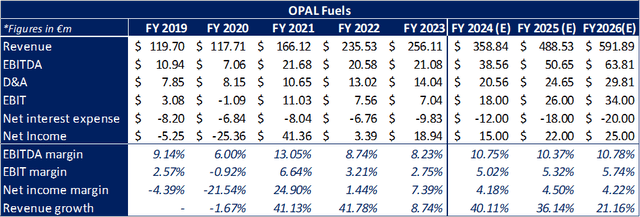

OPAL reported revenues up 8.74% in FY23, registering a lower within the development tempo, partly as a result of deconsolidation of VIEs, Emerald and Sapphire, which had a optimistic influence of $122m. This resulted in web revenue of $18.9m or $0.69 per share, a major enchancment from $0.12 per share in FY22. Excluding this accounting artifice, OPAL working margins decreased, primarily on account of a rise in some working prices associated to the Gasoline Station Providers section. EBIT margin seems to be 2.75% in FY23, down from 3.21% in FY22.

I anticipate a major improve in revenues in FY24, particularly if the ITC (Funding Tax Credit score) from Emerald and the three landfill RNG initiatives coming on-line this yr are confirmed, which ought to convey a optimistic influence of $40m. As well as, I anticipate development in working outcomes with an EBIT margin at 5% in FY24, following the improved working outcomes of the gasoline station providers section introduced by administration in Press Launch. However, I imagine a discount in web revenue margin is believable as FY23 outcomes have been considerably impacted positively by deconsolidation. A lot will probably be contingent on the value of RIN, LCFS, and whether or not it’s entitled to the abovementioned ITC.

OPAL SEC Filings and Creator’s Estimates

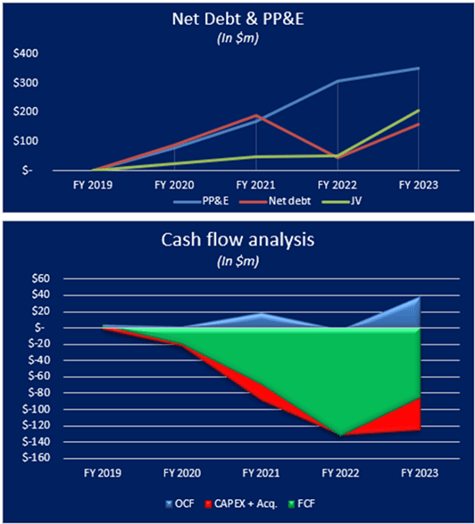

From a monetary perspective, OPAL is endeavor a major funding marketing campaign, a few of which I’ve mentioned in earlier sections. Capex and JV investments are estimated to be $230m in FY24, up from $126m in FY23. It will virtually definitely trigger a major improve in debt, already at greater ranges than its rivals, regardless of being effectively coated by PP&E and JV investments. For FY24, it has $263.4m out there below the delayed draw time period mortgage, and $36.2m below the revolver facility below the OPAL Time period Mortgage. For these causes, it ought to have sufficient liquidity to implement its funding plan, together with benefiting from the eventual assortment of the ATM program introduced in November 2023. OCF manufacturing nonetheless seems to be poor in comparison with the 2 rivals analyzed earlier, with closely detrimental FCFs as an impact of the big volumes of investments made. This dynamic is predicted to proceed in FY24, regardless of an anticipated improve in OCF in comparison with $39m in FY23.

OPAL SEC Filings and Creator’s Evaluation

Principal Dangers

The highest two prospects are value 47% of OPAL’s complete revenues, 36% and 11% buyer A and buyer B, respectively.

Firm-owned services are sometimes primarily based on agreements like leases, often 20 years in length with renewal choices. This issue makes the corporate’s belongings extraordinarily depending on the choices of third events.

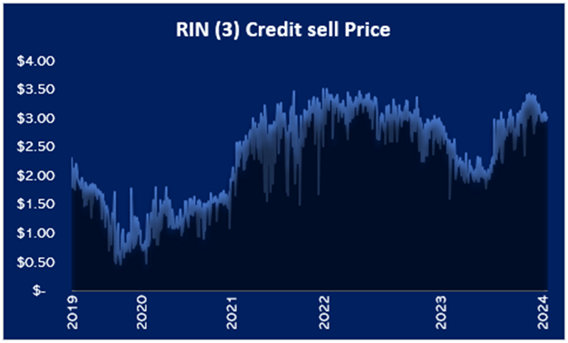

About 50% of revenues are derived from environmental attributes corresponding to RECs, RIN(D3) and LCFS, an element that makes revenues extraordinarily risky as will be seen within the graph beneath.

www.epa.org

Like all firms working on this enterprise, OPAL is extraordinarily depending on business regulation in the US. Modifications to the rules presently in place can due to this fact have important impacts both positively or negatively. An instance of that is the introduction of the Inflation Discount Act wherein the ITC, a tax credit score that can lead to a 30% decrease value when it comes to the preliminary funding of a brand new venture. For the time being, nevertheless, it’s nonetheless unclear whether or not RNG manufacturing services fall below the rules, creating confusion within the business with the potential of delaying or ensuing within the elimination of already deliberate investments.

On Nov. 17, 2023, OPAL introduced the launch of an ATM program for a minimum of $75m in capital, resulting in attainable dilution of shareholder capital. Furthermore, it has a considerably greater stage of web debt than Montauk and Clear Power, implying larger problem in taking up new debt and making future capital will increase extra doubtless.

As of December 2023, the Chairman of board of administrators Mr. Mark Comora controls 94.1% of the voting rights. This focus could in the long term result in overshadowing the pursuits of minority shareholders.

Discounted Money Circulation

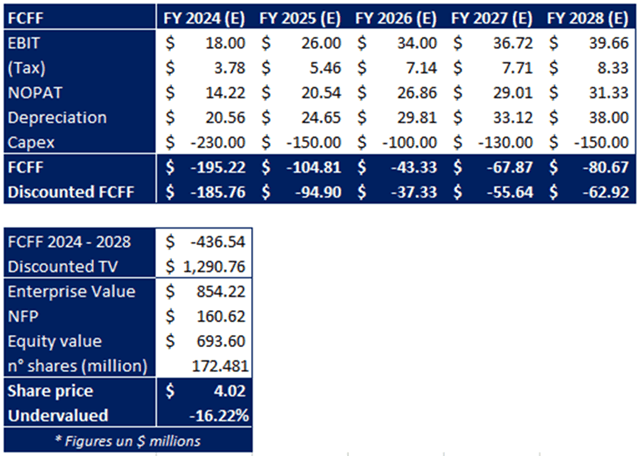

I carried out a DCF evaluation to evaluate OPAL intrinsic worth, returning a valuation of €4.02 per share, roughly 15% beneath the present market worth. The next assumptions have been used to find out the truthful worth:

Beta: 0.51 obtained from Investing.com.

MRP (5.7%) and Threat-Free fee (3.8%) have been obtained through the use of 2023 Fernandez’s information, weighted by the geographic breakdown of the corporate’s revenues. A price of fairness of 4.77% was obtained.

Value of debt (4.71%) was obtained from the ratio of curiosity bills to complete debt as of December 2023.

WACC = 5.09% elevated by 0.5% to contemplate the chance related to the restricted market cap.

g = 2% consistent with the inflation goal within the US.

Creator’s Evaluation & Estimates

Conclusion

Creator’s Evaluation & Estimates

I imagine that from a top quality and organizational perspective, OPAL Fuels represents top-of-the-line funding alternatives within the RNG sector. The working mannequin is extremely specialised and verticalized, with one of the vital in depth networks of RNG gasoline stations in the US and rising in-house RNG manufacturing that would quickly exceed that of Montauk, as early as FY24 or FY25. This success has been achieved via a major funding marketing campaign, nonetheless ongoing, geared toward constructing a ten MMBtus manufacturing chain by the tip of 2025. Nonetheless, I imagine OPAL is barely overvalued even contemplating anticipated future multiples. As well as, in my opinion there’s a truthful quantity of capital dilution threat from greater debt than its rivals, which may restrict its capability to tackle further debt within the medium time period and power a capital improve. Elevated money flows and lowered dependence on exterior financing sources may act as catalysts to make the corporate a sexy alternative. Total, I assign a Maintain ranking to OPAL, pending a major enchancment in margins and, most significantly, a rise in working money circulation era, which is presently at too low a stage.