Robert Manner

NIO (NYSE:NIO) ended FY22 with 122,486 deliveries after two document months in November and December mixed for practically 30,000 items — an annual 180,000 unit run fee. Wanting forward for 2023, differing EV market forecasts for China supply a little bit of uncertainty round client demand and general market progress, however the items are in place for NIO to probably document 50% or greater supply progress ought to demand stay agency for its fashions and manufacturing and covid-19 associated headwinds ease.

Chinese language EV Market Outlook

Forecasts for progress for the world’s largest EV market supply some differing views for the place the business will finish in 2023 — the China Passenger Automotive Affiliation is anticipating progress of round 2.0 million automobiles to succeed in 8.5 million gross sales for the yr, about 31% progress.

Different forecasts for progress counsel barely decrease progress to 8.4 million items on the idea that the EV “market is set to lose steam in 2023 as Beijing phases out money subsidies and customers draw back from big-ticket gadgets over issues a couple of gloomy economic system.” Subsidies phasing out may characterize a significant headwind to the market ought to client demand reduce as automobiles turn into comparatively costlier.

Nonetheless, forecasts from UBS are suggesting “that passenger NEV gross sales would attain 8.8 million items in 2023, accounting for 38 p.c of complete passenger automobile gross sales.” This forecast sits about 4% greater than the CPCA’s 8.5 million projection, seeing the renewed progress coming as “client confidence is restored and automobile makers vie to launch new fashions.”

So the principle takeaway right here is that the business is extensively projected to document at minimal 30% progress, to at the least 8.3 million items, probably as much as 8.8 million or 8.9 million in upside forecasts.

Main Chinese language OEMs are additionally focusing on important progress throughout 2023 — Nice Wall Motor (OTCPK:GWLLY) is aiming to launch 10 NEV fashions through the yr to spice up progress, Geely-backed Zeekr desires to double gross sales in 2023 to over 140,000 items, and Mercedes-Benz (OTCPK:MBGYY) is launching six fashions within the nation. For NIO, the query now circles again to progress — will one other ~30% y/y progress fee in deliveries be robust sufficient? Ought to Zeekr hit targets, it is going to be simply 10k to 15k items shy of NIO with solely two fashions, barely two years after launching gross sales — this situation would seemingly mirror poorly on NIO because it struggles in opposition to aggressive strain.

This autumn Deliveries Hit A New Excessive

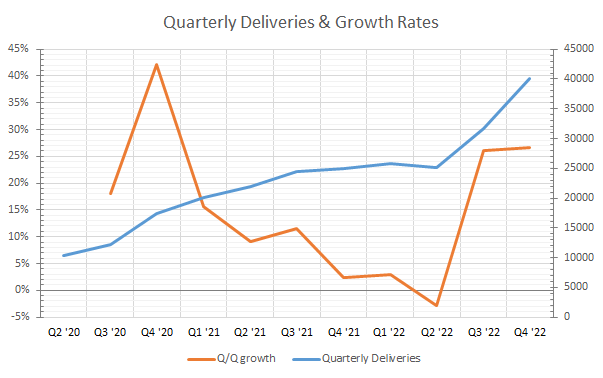

A really robust finish to 2022 helped NIO attain new highs for This autumn’s deliveries, totaling 40,052 automobiles, +60% y/y. This autumn marked two consecutive quarters of higher that 26% sequential progress after Q3 broke previous a 26k/quarter ceiling.

Primarily, NIO has shortly ramped up its common supply run fee from round 8.5k per 30 days as much as 15k per 30 days by the top of This autumn, with November and December combining for just below 30k deliveries. Nonetheless, sustaining this run fee is unlikely for the preliminary half of Q1 because of impacts from Lunar New 12 months affecting manufacturing and demand.

Creator calculations

The above graph reveals NIO’s quarterly ship totals [blue] alongside sequential quarterly progress charges [orange] from Q2 2020 to the top of 2022. What’s noticeable right here is that sequential progress charges have picked again up in direction of late 2020’s ranges, bouncing off a decline in Q2 ’22 after NIO had struggled for a number of quarters exhibiting lower than 5% sequential progress.

Resumption of ~26% q/q progress charges is a powerful optimistic for shares shifting ahead, as a result of it represents near-exponential scalability — a 26% q/q fee for every quarter in FY23 would land at 293k items, or 140% y/y progress. Reining that in to a extra manageable ~11% common sequential fee would mission deliveries at 210k for FY23, or ~72% y/y progress. Reaching 72% y/y progress for 2023 can be a significant accomplishment and a significant restoration from 2022’s 34% progress.

Deliveries By Car: A Crimson Flag?

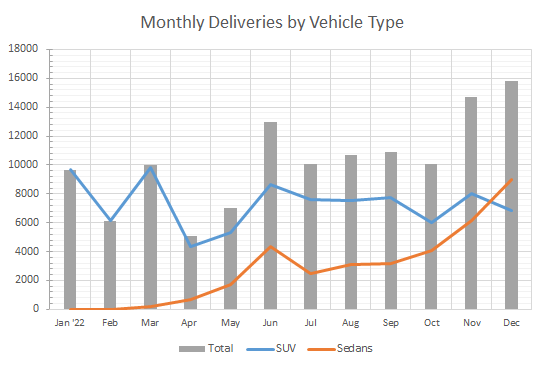

For the primary time in December, sedan deliveries overtook SUV deliveries, with over 2.1k extra sedans delivered through the month as SUVs dropped. Sedan deliveries have recorded a fifth straight month of progress, with a trajectory simply suggesting NIO may ramp above 10k/month fee through the early levels of FY23.

Nonetheless, the supply breakdown by automobile is elevating some purple flags about progress potentialities — NIO is closely reliant on its latest fashions, the ET5 and ET7 (ES7) for progress.

Creator calculations

Wanting deeper into NIO’s deliveries reveals that ET5 contributed 48% of December’s complete deliveries, whereas the ET5 and ES7 [EL7] mixed for over 74% of that complete. Demand for the ET5 has been significantly excessive — the mannequin scaled from 221 items in September to almost 7,600 by December, NIO’s quickest ramp of its latest fashions.

This means that NIO is extraordinarily concentrated and intensely reliant on these two new fashions to drive progress — both demand for NIO’s 5 older fashions has fallen considerably, or manufacturing has been reallocated to prioritize the 2 new fashions.

From a progress standpoint, the previous can be an enormous unfavourable for NIO — as rivals intention to turbocharge progress in 2023, demand destruction for NIO’s long-standing fashions factors to a tougher progress image with extra EV fashions hitting the market. The latter situation isn’t essentially a optimistic or a unfavourable, slightly it provides a glimpse into how NIO may allocate manufacturing with as much as 5 new fashions launched as capability expands in direction of 30k/month.

2023 Outlook

Successfully dealing with business headwinds and holding pretty constant manufacturing by way of the yr (in contrast to April and Q3 2022) may put NIO on monitor to document 180k to 195k automobiles, or >50% y/y progress, for FY23. Capability definitely helps such progress, as NeoPark’s operations ought to present the power to succeed in a 20,000 to 25,000 items/month run fee. A five-year settlement with CATL will present the required battery provide to assist such progress.

Financially, there’s nonetheless room to enhance — automobile margins dipped barely q/q in Q3 whereas gross margin rose barely. Web losses widened 50.2% q/q as working bills, significantly R&D, jumped. EBITDA is shifting farther into the purple, with Q3 posting unfavourable $484 million EBITDA in comparison with Q1 2021’s unfavourable $5.2 million.

With break-evens nonetheless removed from view, as gross margin has fallen 700 bp y/y as of Q3 whereas working bills proceed to rise, upside could also be restricted by way of FY23 whilst deliveries are projected to rise 50% or extra. At an preliminary income estimate of $13.8 billion and 3x EV/income a number of for FY23, shares may discover significant upside to $27 ought to NIO execute accordingly and scale deliveries to 180,000 items or above, whereas additionally reversing a pattern of rising losses.