Up to date on July twenty fourth, 2024 by Bob Ciura

Spreadsheet information up to date every day

On this planet of investing, volatility issues.

Traders are reminded of this each time there’s a downturn within the broader market and particular person shares which are extra unstable than others expertise monumental swings in value in each instructions.

That volatility can enhance the chance in a person’s inventory portfolio relative to the broader market.

The volatility of a safety or portfolio in opposition to a benchmark – known as Beta. Briefly, Beta is measured by way of a formulation that calculates the worth danger of a safety or portfolio in opposition to a benchmark, which is usually the broader market as measured by the S&P 500 Index.

It’s useful in understanding the general value danger degree for buyers throughout market downturns particularly.

Right here’s tips on how to learn inventory betas:

- A beta of 1.0 means the inventory strikes equally with the S&P 500

- A beta of two.0 means the inventory strikes twice as a lot because the S&P 500

- A beta of 0.0 means the shares strikes don’t correlate with the S&P 500

- A beta of -1.0 means the inventory strikes exactly reverse the S&P 500

Curiously, low beta shares have traditionally outperformed the market… However extra on that later.

You may obtain a spreadsheet of the 100 lowest beta shares (together with monetary metrics like price-to-earnings ratios and dividend yields) by clicking on the hyperlink under:

This text will focus on tips on how to calculate beta, the distinction between high-beta and low-beta shares, in addition to particular person evaluation of the one inventory within the S&P 500 Index with adverse beta proper now.

The desk of contents supplies for straightforward navigation of the article:

Desk of Contents

Excessive Beta Shares Versus Low Beta

Beta is useful in understanding the general value danger degree for buyers throughout market downturns particularly. The decrease the Beta worth, the much less volatility the inventory or portfolio ought to exhibit in opposition to the benchmark.

That is useful for buyers for apparent causes, notably these which are near or already in retirement, as drawdowns must be comparatively restricted in opposition to the benchmark.

Low or excessive Beta merely measures the scale of the strikes a safety makes; it doesn’t imply essentially that the worth of the safety stays practically fixed.

Securities could be low Beta and nonetheless be caught in long-term downtrends, so that is merely yet one more instrument buyers can use when constructing a portfolio.

Intuitively, it might make sense that top Beta shares would outperform throughout bull markets. In spite of everything, these shares must be attaining greater than the benchmark’s returns given their excessive Beta values.

Whereas this may be true over brief durations of time – notably the strongest components of the bull market – the excessive Beta names are usually the primary to be offered closely by buyers.

This wonderful paper from the CFA Institute theorizes that that is true as a result of buyers are ready to make use of leverage to bid up momentum names with excessive Beta values and thus, on common, these shares have decrease potential returns at any given time.

As well as, leveraged positions are among the many first to be offered by buyers throughout weak durations due to margin necessities or different financing considerations that come up throughout bear markets.

Whereas excessive Beta names could outperform whereas the market is powerful, as indicators of weak spot start to point out, excessive Beta names are the primary to be offered and customarily, far more strongly than the benchmark.

Proof suggests that in good years for the market, excessive Beta names seize 138% of the market’s complete returns.

Subsequently, if the market returned 10% in a yr, excessive Beta names would, on common, produce 13.8% returns. Nonetheless, throughout down years, excessive Beta names seize 243% of the market’s returns.

In an analogous instance, if the market misplaced 10% throughout a yr, the group of excessive Beta names would have returned -24.3%.

Given this comparatively small outperformance throughout good instances and huge underperformance throughout weak durations, it’s simple to see why we desire low Beta shares.

Whereas low Beta shares aren’t fully immune from downturns out there, it’s a lot simpler to make the case over the long term for low Beta shares versus excessive Beta given how every group performs throughout bull and bear markets.

How To Calculate Beta

The formulation to calculate a safety’s Beta is pretty easy. The end result, expressed as a quantity, reveals the safety’s tendency to maneuver with the benchmark.

Beta of 1.00 signifies that the safety in query ought to transfer just about in lockstep with the benchmark (as mentioned briefly within the introduction of this text).

Beta of two.00 means strikes must be twice as giant in magnitude.

Lastly, a adverse Beta signifies that returns within the safety and benchmark are negatively correlated; these securities have a tendency to maneuver in the wrong way from the benchmark.

This type of safety could be useful to mitigate broad market weak spot in a single’s portfolio as negatively correlated returns would recommend the safety in query would rise whereas the market falls.

For these buyers in search of excessive Beta, shares with values in extra of 1.3 could be those to hunt out. These securities would provide buyers at the very least 1.3X the market’s returns for any given interval.

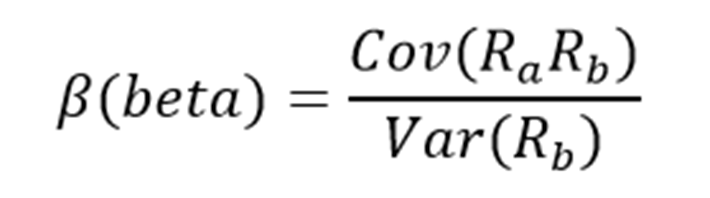

Right here’s a take a look at the formulation to compute Beta:

The numerator is the covariance of the asset in query whereas the denominator is the variance of the market. These complicated-sounding variables aren’t really that troublesome to compute.

Right here’s an instance of the information you’ll must calculate Beta:

- Danger-free charge (usually Treasuries at the very least two years out)

- Your asset’s charge of return over some interval (usually one yr to 5 years)

- Your benchmark’s charge of return over the identical interval because the asset

To point out tips on how to use these variables to do the calculation of Beta, we’ll assume a risk-free charge of two%, our inventory’s charge of return of 14% and the benchmark’s charge of return of 8%.

You begin by subtracting the risk-free charge of return from each the safety in query and the benchmark. On this case, our asset’s charge of return internet of the risk-free charge could be 12% (14% – 2%). The identical calculation for the benchmark would yield 6% (8% – 2%).

These two numbers – 12% and 6%, respectively – are the numerator and denominator for the Beta formulation. Twelve divided by six yields a price of two.00, and that’s the Beta for this hypothetical safety.

On common, we’d count on an asset with this Beta worth to be 200% as unstable because the benchmark.

Serious about it one other manner, this asset must be about twice as unstable than the benchmark whereas nonetheless having its anticipated returns correlated in the identical path.

That’s, returns could be correlated with the market’s total path, however would return double what the market did through the interval.

This may be an instance of a really excessive Beta inventory and would provide a considerably greater danger profile than a median or low Beta inventory.

Beta & The Capital Asset Pricing Mannequin

The Capital Asset Pricing Mannequin, or CAPM, is a standard investing formulation that makes use of the Beta calculation to account for the time worth of cash in addition to the risk-adjusted returns anticipated for a specific asset.

Beta is an integral part of the CAPM as a result of with out it, riskier securities would seem extra favorable to potential buyers as their danger wouldn’t be accounted for within the calculation.

The CAPM formulation is as follows:

The variables are outlined as:

- ERi = Anticipated return of funding

- Rf = Danger-free charge

- βi = Beta of the funding

- ERm = Anticipated return of market

The danger-free charge is similar as within the Beta formulation, whereas the Beta that you just’ve already calculated is solely positioned into the CAPM formulation.

The anticipated return of the market (or benchmark) is positioned into the parentheses with the market danger premium, which can also be from the Beta formulation. That is the anticipated benchmark’s return minus the risk-free charge.

To proceed our instance, right here is how the CAPM really works:

ER = 2% + 2.00(8% – 2%)

On this case, our safety has an anticipated return of 14% in opposition to an anticipated benchmark return of 8%.

In idea, this safety ought to vastly outperform the market to the upside however take into account that throughout downturns, the safety would undergo considerably bigger losses than the benchmark.

If we modified the anticipated return of the market to -8% as an alternative of +8%, the identical equation yields anticipated returns for our hypothetical safety of -18%.

This safety would theoretically obtain stronger returns to the upside however definitely a lot bigger losses on the draw back, highlighting the chance of excessive Beta names throughout something however sturdy bull markets.

Whereas the CAPM definitely isn’t excellent, it’s comparatively simple to calculate and provides buyers a method of comparability between two funding options.

Evaluation On The S&P 500 Inventory With Damaging Beta

Now, we’ll check out the S&P 500 inventory that at the moment has a adverse beta worth. On the time of publication, there was just one inventory within the S&P 500 Index with a adverse beta worth, based on a inventory display screen from FinViz.

Damaging Beta Inventory: Biogen Inc. (BIIB)

Biogen is a large-cap pharmaceutical firm with a present market cap of roughly $32 billion. Biogen doesn’t at the moment pay a dividend. The inventory has a adverse Beta worth of -0.04 proper now.

Within the 2024 first quarter, Biogen reported GAAP earnings-per-share progress of 1% and adjusted EPS progress of 8% year-over-year. First quarter income got here to $2.3 billion, down 7% year-over-year. Product income declined 3% from the identical quarter final yr.

For the total yr, Biogen reaffirmed steering which requires adjusted EPS in a variety of $15.00 to $16.00. On the midpoint, Biogen expects EPS progress of roughly 5% for 2024.

Closing Ideas

Beta is likely one of the most widely-used measures of inventory market volatility. Beta generally is a precious instrument for buyers when analyzing shares for inclusion of their portfolios.

Shares with adverse betas are anticipated to maneuver inversely to the broader market. Damaging-beta shares might be notably interesting in a recession or a market downturn.

In case you are fascinated with discovering extra high-quality dividend progress shares appropriate for long-term funding, the next Certain Dividend databases will probably be helpful:

The key home inventory market indices are one other stable useful resource for locating funding concepts. Certain Dividend compiles the next inventory market databases and updates them repeatedly:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}