")

Oli Scarff/Getty Photos Information

Marks and Spencer (OTCQX:MAKSY)(OTCQX:MAKSF)(“M&S”) inventory has been on a terrific run in 2023. The enduring British retailer has seen its major London-listed shares surge simply over 120% this 12 months, with the USD-denominated ADSs up just a few factors extra as GBP has gained in opposition to the buck. Whereas a welcome efficiency for M&S stockholders, a little bit extra context is required right here, with the 2023 share worth positive factors solely taking the inventory again to roughly the place it was 5 years in the past earlier than COVID. Whereas the catalyst for constructive latest returns has been a welcome enchancment in each M&S’s important enterprise traces, the present share worth now absolutely displays administration’s medium-term gross sales and margin ambitions, leaving little margin of security for traders.

Supply: Searching for Alpha

M&S operates two important home retail traces: Clothes & House (“C&H”) and Meals. C&H accounted for round 30% of M&S’s gross sales in its final full fiscal 12 months, however with this being a better margin enterprise than Meals its contribution to adjusted working revenue is increased (~50% in fiscal 2022/23). Meals contributes ~60% of gross sales and ~40% of adjusted working revenue, with M&S additionally having a modest Worldwide enterprise (~13% of adjusted working revenue) in addition to a loss making 50:50 JV with Ocado Group (OTCPK:OTCPK:OCDDY)(OTCPK:OTCPK:OCDGF) known as Ocado Retail. That is principally a web based grocery service that delivers direct to prospects’ houses.

As talked about within the introduction, M&S shares have been on a tear this 12 months however solely to the purpose of recovering earlier misplaced floor. COVID was a major drag, with the agency additionally having to suck up massive prices to reposition its retailer property. That led to a complete reduce of its dividend again in 2020. Natural development is of course anaemic right here given M&S’s geographic profile and enterprise traces, however on high of that C&H had been battling very weak comps. The absence of a payout meant there was little help for the inventory following the dividend reduce in 2020.

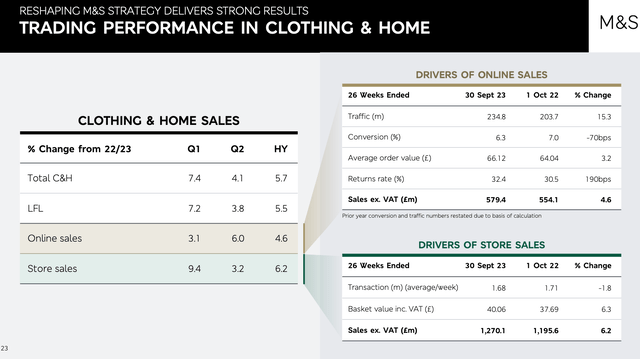

The excellent news for M&S is that underlying enterprise is unquestionably bettering. One key development to look at at trend retailers is the proportion of gross sales that entice full costs versus reductions. Vogue clearly tends to be fairly fickle, so a comparatively massive share of full-priced gross sales and a rising high line generally is a good signal that an organization’s merchandise are nonetheless in vogue with customers. C&H reported that its full-price gross sales combine was 82% in H1 2023/24 (i.e. the six months by September), representing the third straight half-year of 80%-plus combine and 14ppt forward of 2019 ranges (when like-for-like gross sales have been falling as customers have been clearly not impressed with its providing).

It additional reported that model notion has been bettering in its core product classes. Menswear, womenswear and lingerie are up wherever between 4-7ppt over the previous two years based on third-party shopper surveys, with general C&H market share up circa 40bps year-on-year to 9.5%. All mentioned, that helped energy H1 like-for-like gross sales development of 5.5% as per final month’s outcomes launch. With gross sales up and a few inflationary ache factors like transport prices beginning to ease, C&H working margin was up 230bps to 12.1%.

Supply: Marks and Spencer 1H 2023/24 Outcomes Presentation

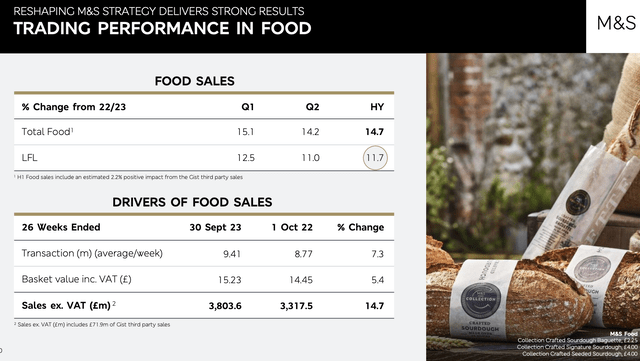

Meals can also be displaying constructive tendencies. M&S’s web promotor rating widened 3ppt year-over-year in H1, with volumes outpacing a falling market by mid-to-high single-digits in every month of the interval. Market share was up 10bps to three.4%. With common basket measurement additionally up, gross sales development was strong, growing by a little bit beneath 15% year-on-year in H1. That, in flip, helped energy a 210bps enlargement in adjusted working margin, which clocked in at 4.3%.

Supply: Marks and Spencer 1H 2023/24 Outcomes Presentation

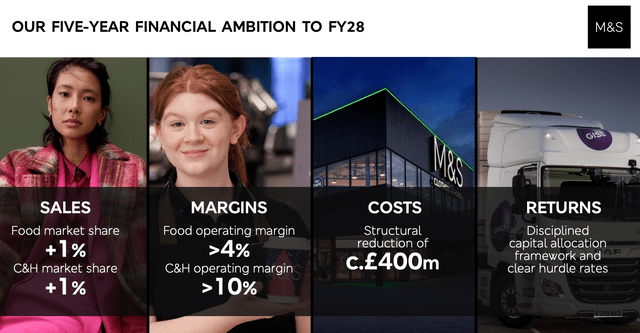

Whereas M&S continues to submit welcome enhancements in each its core enterprise traces, my important problem with the inventory is that the present share worth already displays administration’s medium-term working targets. These targets embody 1ppt market share positive factors in each C&H and Meals by FY 2028, with adjusted working margins focused above 10% within the former and above 4% within the latter. Whereas margin targets look modest given H1 figures have been already increased in each segments, keep in mind that full-year earnings will likely be weighted towards the primary half of the 12 months as per administration:

Nevertheless, as we enter 2024, we’re not counting on the beneficial latest market circumstances persisting. The outlook stays unsure with the possible affect on the patron of the best rates of interest in 20 years, deflation, geopolitical occasions, and erratic climate. However this backdrop, we are going to proceed to put money into trusted worth for our prospects and we’re growing our funding within the reshaping of M&S within the second half. Due to this fact, in opposition to tougher comparatives, we anticipate revenue earlier than tax and adjusting gadgets to be weighted in the direction of the primary half, as we stay laser-focused on our long-term ambition to reshape M&S for future development.

Marks and Spencer, 1H 2023/24 Outcomes Launch

Now, these margin targets will not be really my important fear. The rationale for that’s that a part of this consists of round £400 million in deliberate value discount. As I discussed close to the start, M&S has been repositioning its retailer property to higher match its enterprise. This includes closures, transferring present shops to extra acceptable places and so forth. This has been a drag as M&S has a reasonably excessive share of freehold and lengthy leasehold actual property, however the constructive side is that rental and occupancy prices ought to characterize numerous low hanging fruit when it comes to value chopping. I’d fear extra about sustained market share positive factors given how fiercely aggressive the style and grocery markets are within the U.Okay.

Supply: Marks and Spencer November 2023 Capital Markets Day Presentation

Now, C&H holds a present market share of 9.5% as per above. On trailing-twelve-month gross sales of circa £3.8 billion, that places the worth of the U.Okay. market at round £40 billion in whole. Assuming low single-digit annual development and a one level achieve in share, implied C&H high line can be round £4.5 billion by FY 2028, with adjusted working revenue touchdown at a minimal of £450 million.

For Meals, present share of 4.3% maps to a complete home market worth of £180 billion. Once more assuming low single-digit annual market development, a one level achieve in shares will get us to FY 2028 income of circa £9.9 billion, with a 4% margin resulting in working revenue of ~£400m. Assuming £100 million in annual Worldwide adjusted working revenue (was ~£43 million in 1H 2023/24), we get to round £950 million in implied company-wide adjusted working revenue by FY 2028.

At the moment, M&S has an enterprise worth of circa £8.1 billion, which maps to a a number of of roughly 11x TTM adjusted working revenue. On a flat a number of, implied enterprise worth can be circa £10.4 billion by fiscal 2028, which after subtracting web debt (~£2.5 billion) would result in a share worth of round £3.80 ($9.70 per ‘MAKSY’ ADS at present trade charges) primarily based on 2.1 billion shares in problem. The present share worth is £2.72 (~$6.93 per ADS), implying circa excessive single-digit annualized share worth development out to FY 2028. M&S is tentatively reestablishing its dividend, having declared a £0.01 per share interim payout alongside H1 outcomes, so I anticipate that to contribute low single-digits every year on high of that.

The above would get us to double-digit annualized returns over the subsequent few years – roughly the minimal degree that many traders demand from their inventory portfolio. With that absolutely incorporating administration’s development targets with little room for error, I do not see the worth in M&S shares proper now. I’d be in search of a 20% low cost to construct in an acceptable margin of security, akin to a present truthful worth of £2.18 (~$5.55 per ‘MAKSY’ ADS). Traders can afford to attend for a extra engaging entry level right here. Maintain.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.