")

jetcityimage/iStock Editorial by way of Getty Pictures

It has been a curler coaster journey for the Lucid inventory (NASDAQ:LCID) this 12 months. After its valuation plummeted final 12 months following the onset of financial coverage tightening, which punished development shares most, alongside an industry-wide provide chain disruption that restricted Lucid’s skill to ramp up productions, the inventory regained some floor earlier this 12 months on the coat-tails of a broader market rally. But, the momentum was short-lived, as the corporate confronted rising demand dangers – which administration had alluded earlier within the 12 months to missing buyer consciousness of the model in addition to evolving dynamics in market circumstances.

And from the market’s perspective, Lucid’s unprofitable, but capital-intensive, enterprise amid the elevated borrowing value setting can also be dulling the enchantment of its development prospects. That is additional corroborated by strain noticed on the inventory’s latest efficiency after the corporate introduced an incremental fairness providing inside the previous month. Regardless of Lucid’s ongoing efforts in optimizing its value profile, and bettering its model consciousness as means to drive higher sturdiness in gross sales development, there are doubtless restricted catalysts inside the close to time period – particularly contemplating unsure market circumstances forward – with rising execution dangers pertaining to the underlying enterprise’ longer-term development initiatives, spanning Gravity SUV begin of manufacturing and worldwide footprint enlargement. The mix of Lucid’s unsure longer-term capital construction, elementary challenges in ramping up output volumes and gross sales, and valuation premium nonetheless at present ranges underscores dangers that stay skewed to the draw back for the inventory, in tandem with anticipated broader market volatility forward.

Unsure Longer-Time period Capital Construction

The capital-intensive nature of Lucid’s enterprise, alongside nonetheless being unprofitable, stays an overhang on its valuation prospects, particularly amid the at present unsure market local weather blighted by rising borrowing prices. In line with administration’s commentary through the first quarter earnings name, Lucid ended the interval with $3.4 billion in money and money equivalents, in addition to different sources of funding that might convey its liquidity as much as roughly $4 billion:

Now transferring to the steadiness sheet. We ended the quarter with simply over $3.4 billion in money, money equivalents and investments with complete liquidity of roughly $4.1 billion

Supply: Lucid 1Q23 Earnings Name Transcript

Particularly, the corporate ended with about $900 million in money and money equivalents on its steadiness sheet, in addition to near $2.5 billion in short- and long-term investments at present categorized as accessible on the market securities as of March thirty first, which alongside its present credit score amenities supplies complete liquidity of about $4 billion.

Lucid 1Q23 10-Q Submitting

Recall that Lucid has a protracted demonstrated its skill in sustaining a wholesome pipeline of funding sources, together with $1.75 billion in proceeds from a inexperienced convertible bond providing at 1.25% in late 2021, $1.5 billion from an at-the-market personal placement in late 2022, a $1 billion asset-based revolving credit score facility, and different working capital amenities and funding from the Kingdom of Saudi Arabia. Whereas a number of the associated proceeds have been invested into ongoing development initiatives, in addition to different normal company functions, administration had cited through the first quarter earnings name that Lucid’s complete liquidity of roughly $4 billion as of March 31 was adequate to maintain operations by the second quarter of 2024. This means additional capital elevating efforts inside the foreseeable future to assist its longer-term development initiatives – together with the launch and SOP of the Gravity SUV later subsequent 12 months. Regardless of weak market circumstances, Lucid had adopted up with a $3 billion fairness providing earlier this month, which pushed costs on its shares decrease. Particularly, the corporate issued a public providing of 173,544,948 shares at $6.91 apiece for gross proceeds of $1.2 billion, in addition to a personal placement to Ayar Third Funding Firm – an affiliate of the Saudi Arabia Public Funding Fund, its largest shareholder – of 265,693,703 shares at $6.77 apiece for gross proceeds of $1.8 billion.

Taken collectively, Lucid’s liquidity profile has been boosted to about $7 billion. Primarily based on its quarterly money run-rate within the first three months of the 12 months, inclusive of $801 million internet money utilized in working actions and $242 million capex, and administration’s information for full 12 months 2023 capex at $1.5 billion on the mid-point, its present liquidity profile will doubtless final by 2024 and assist the SOP of its Gravity SUV. However given its core automobile gross sales enterprise stay lengthy methods from being self-sufficient, we anticipate additional longer-term uncertainty to Lucid’s capital construction, which might stay a major overhang on the inventory’s prospects. At a time when traders crave worthwhile development and a powerful steadiness sheet, the dearth of readability over Lucid’s longer-term capital construction, because it continues to battle with ramping up its early-stage development aspirations, will doubtless additional amplify draw back dangers to the inventory.

Price Optimization Efforts Have But to Make a Dent in Narrowing Losses

Admittedly, auto manufacturing is a cost-intensive enterprise for even well-funded incumbents – therefore, the surge in loss-making EV applications amid legacy automakers’ transition to electrical – not to mention for vertically built-in, greenfield start-ups like Lucid. Whereas the corporate’s best-in-class automobile design and battery know-how have enabled differentiation by its flagship Air sedan’s report vary per cost, ramping up productions stay a bottleneck that’s nonetheless precluding it from reaching economies of scale. In the meantime, coming off of unprecedented provide constraints previously 12 months that has roiled the broader auto {industry} – particularly start-ups like Lucid with little negotiating energy with suppliers – is adopted by looming demand dangers as a result of deteriorating macroeconomic circumstances. And associated issues are already getting picked up by the Wall Avenue neighborhood, as corroborated by Guggenheim analyst Ron Jewsikow’s inquiry on how administration goals to deal with demand headwinds dealing with the posh EV phase, in addition to rising competitors, through the first quarter earnings name:

Ron Jewsikow

Good night, and thanks for taking my query. Peter, simply needed to get your ideas on form of aggressive dynamics out there proper now. From our vantage level, it seems like a reasonably difficult marketplace for luxurious electrical automobiles, however needed to get your view on if value cuts out of your — certainly one of your massive home rivals on their luxurious line of automobiles is having any affect on demand for used automobiles?

Peter Rawlinson

Effectively, I feel what you are referring to is maybe a unique a part of the market. I consider that there’s a problem to the complete market proper now due to macroeconomics and due to rates of interest, which really do have an effect on this place of the market. We’re seeing key rivals from Germany discounting their merchandise very closely that is not simply the U.S. producer that you could be be referencing the Germans are closely discounting their automobiles, and I feel there are challenges proper throughout {the marketplace}. I feel what we have to do is simply amplify consciousness simply how compelling our product is.

Supply: Lucid 1Q23 Earnings Name Transcript

To handle stated speedy elementary dangers dealing with its enterprise, Lucid has adopted the footsteps of its friends throughout the broader {industry} to chop prices and deal with enhance revenue margins, whereas additionally prioritizing “development and model consciousness” to drive realization of gross sales on its P&L.

Price Optimization

On the fee optimization entrance, Lucid has diminished its workforce by about 18% earlier this 12 months, which resulted in a one-time restructuring cost of $22.5 million through the first quarter. The corporate is anticipating one other one-time restructuring cost of $2 million within the present quarter attributable to the “last half” of its expertise optimization efforts. Taken collectively, Lucid expects annualized value financial savings of as a lot as $91 million from streamlining its workforce alone, which may have a extra evident affect on its backside line by the 12 months as associated efficiencies are already in impact and could be noticed by a “decrease base employees compensation” spend through the first quarter.

Along with job cuts, Lucid has additionally labored to additional cut back its automobile invoice of supplies by negotiating new provide contracts. The brand new agreements stipulate improved “piece value value” by leveraging incremental volumes on Lucid’s new automobile applications – together with the newest addition of recent Air sedan variants in manufacturing, in addition to its upcoming Gravity SUV (80% of associated elements have been sourced). The implementation of “engineering modifications”, spanning enhancements to the meeting line and incorporation of “new decrease value elements”, have additionally enabled reductions to Lucid’s automobile BoM, contributing additional to its ongoing margin enlargement efforts.

The corporate additionally sees continued reductions in freight prices following the acute post-pandemic logistics bottlenecks skilled earlier final 12 months. Along with efficiencies realized by bringing the logistics perform in-house, Lucid has additionally transitioned from “air transit to sea” for worldwide freight late final 12 months. Paired with newly negotiated freight contracts through the first quarter, Lucid expects to appreciate value financial savings of 2x to 3x on logistics going ahead, which is able to “begin to present up extra in Q2 and Q3”.

Nevertheless, the aforementioned value optimization efforts will doubtless be partially offset by ongoing LCNRV impairment expenses on stock, in addition to agency buy dedication write-offs inside the foreseeable future. In line with administration’s commentary through the first quarter earnings name, the build-up of Lucid’s uncooked supplies stock over the previous 12 months in response to lingering provide chain uncertainties at the moment are leading to increased prices pertaining to storage and obsolescence, particularly after latest engineering modifications aimed toward decreasing its automobile BoM:

Over the steadiness of the 12 months, we anticipate a major discount in uncooked materials days of stock readily available, but provide chain pressures eased considerably. We obtained extra predictability within the transportation channel and we refine our stock administration processes and techniques… Over the previous 18 months, we’ve got held further stock as a result of issues on half availability and logistics slowdown… Nevertheless, this extra stock has important storage prices, reduces our skill to profit from commodity value reductions that at the moment are occurring and likewise will increase danger for obsolescence in some elements expire or are up to date as a result of engineering modifications. We consider that there’s important financial savings as we unwind a few of this extra stock to concurrently refine our monitoring and stock techniques.

Supply: Lucid 1Q23 Earnings Name Transcript

Whereas administration stays targeted on transitioning its uncooked supplies stock into completed automobiles, and cut back the corporate’s “uncooked materials days of stock readily available”, the alleviation of associated margin pressures usually are not anticipated to grow to be significant till later within the 12 months.

Demand Dangers

But, a lot of Lucid’s ongoing value optimization and margin enlargement efforts will rely on its skill to each ramp up manufacturing in addition to sending vehicles out the door to clients. Recall from earlier this 12 months through the fourth quarter earnings name, administration had already alluded to an absence of brand name consciousness that has been hampering its gross sales volumes:

Look, we have offered manufacturing that isn’t the gating concern right here now. My focus is on gross sales. And this is the factor. We have got what I solely consider to be the perfect product on the earth. And we have simply too few individuals are conscious of not simply the automobile however even the Firm, and so we have to amply focus now away from manufacturing to amplifying buyer consciousness that we have got this superb automobile with unprecedented vary know-how effectivity, unimaginable driving machine, a terrific driver’s automobile, simply unbridled pleasure of possession that we’re getting suggestions from homeowners who’ve skilled this. We have to amplify that message and broaden the notice, which in flip will drive gross sales. And that’s the focus proper now. It is not that we’re production-constrained.

Supply: Lucid 4Q22 Earnings Name Transcript

Administration now not discloses order volumes development, citing that “manufacturing and deliveries are a greater illustration of the progress of [Lucid’s] enterprise”, which supplies little readability on its demand setting in the meanwhile – particularly, a few of its Air sedan variants are taking pre-orders however usually are not but in manufacturing, and present supply volumes don’t replicate that pent-up potential demand. However primarily based on observations of Lucid’s sequential supply declines through the first quarter (4Q22 delivered 1,932 automobiles vs. 1Q23 delivered 1,406 automobiles), and administration’s cautious optimism on the tempo of ramp-up over the rest of the 12 months, quite a bit nonetheless hangs on progress in assembling the Air Pure variant, in addition to market circumstances. Particularly, primarily based on administration’s commentary through the first quarter earnings name, deliveries are anticipated to choose up within the present quarter, with additional enhance by the fourth quarter, although a lot nonetheless is determined by the ramp-up of output volumes within the real-world drive Air Pure variant which works into manufacturing later this 12 months:

We’re on monitor to supply over 10,000 automobiles in 2023 with company-wide initiatives ongoing that may allow increased volumes as market circumstances enable… For Q2, we’re focusing on deliveries to be up sequentially… We anticipate that Q3 manufacturing and supply numbers will in the end be decided by how briskly we’re capable of ramp the pure buildable configuration. And as for This fall, we predict that to be our largest quarter of the 12 months.

Supply: Lucid 1Q23 Earnings Name Transcript

In the meantime, completed stock volumes proceed to develop, which is per ongoing manufacturing ramp-up. Nevertheless, it’s tough to exclude issues of the rising steadiness’s implication of looming demand dangers. Contemplating administration’s repeated acknowledgment of decrease supply volumes through the first quarter as anticipated given ongoing efforts in shoring up model consciousness, and its cautious optimism over supply prospects by the 12 months, Lucid doubtless faces dangers of a weakening demand setting, which could possibly be additional exacerbated by deteriorating monetary circumstances and, inadvertently, client sentiment.

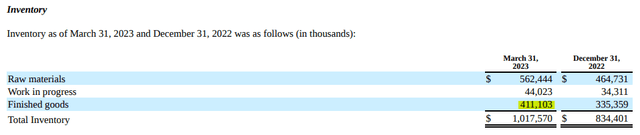

Particularly, the corporate completed the primary quarter with greater than $400 million of completed items stock. Primarily based on first quarter value of income of about $500 million on deliveries of about 1,400 automobiles, or about $356,000 per automobile (excluding value issues attributable to non-core software program and different service gross sales), Lucid’s completed items stock as of March 31 totaling $411 million implies greater than 1,150 items accessible on the market. Admittedly, the quantity could possibly be even decrease, contemplating potential for completed automobiles produced at a better value in prior quarters as output continues to ramp in the direction of economies of scale on a ahead going foundation.

Lucid 1Q23 10-Q Submitting

Whereas administration has alluded to the implied completed items stock steadiness primarily based on items to be inclusive of “take a look at fleet automobiles, loaner automobiles, [and] showroom vehicles” not but accessible however in the end might be accessible on the market, the scenario implies Lucid now not experiences a supply-constrained setting. This accentuates the corporate’s urgency in furthering its model consciousness to drive gross sales development, in keeping with administration’s strategic prioritization over the initiative this 12 months – which was talked about greater than ten occasions through the first quarter earnings name, with CEO Peter Rawlinson accentuating that the Lucid Air is way more inexpensive than media preaches through the convention:

And likewise as we amplify model consciousness. And likewise I come again to this false impression which appears to be on the market. However sure, individuals consider it is a $200,000 automobile Really, the entry degree value is $87,400. It is in all probability conceivable that folks consider it as a $300,000 automobile greenback depend as a result of it is so superb, however really, it is way more attainable, and we have to unfold that phrase as nicely.

Supply: Lucid 1Q23 Earnings Name Transcript

However even at a beginning value of $87,400 for the entry degree trim Air Pure, Lucid’s flagship providing successfully costs out the vast majority of potential automobile patrons in its core American EV market primarily based on latest market analysis reported by Bloomberg Information:

To afford an EV, although, customers have to be fairly nicely off. About one-third of American households make greater than $100,000 a 12 months and about 15% make between that and $150,000, in line with IBISWorld… Since most households personal two or extra automobiles, that lowers the variety of households that may afford EVs at right this moment’s costs to even fewer. As a result of for a family to purchase two EVs, you’d want two individuals making greater than $100,000. Most EVs are priced nicely above the common automobile, making the dollars-and-cents evaluation even harder for many People. Throw all of these numbers collectively and that tells me that lower than 15% of U.S. drivers can afford a battery-powered set of wheels.

Supply: Bloomberg Information

Whereas Lucid’s main technique is to focus on the extra prosperous, much less recession-prone cohort, its enterprise is just not resistant to looming macroeconomic weak spot forward. Whereas EV gross sales have remained resilient, whether or not Lucid can make the most of that may doubtless rely on its skill to ramp up bot output and supply volumes on the decrease priced Air Pure and Touring trims because it continues to work on bolstering its model consciousness. The endeavour continues to counsel large execution dangers inside the foreseeable future, particularly given the worldwide EV value battle instigated by {industry} chief Tesla (TSLA) – which, admittedly, because the gross margin leverage to take action – including additional strain to unprofitable rivals like Lucid. And administration has clarified their stance on the tightening pricing technique noticed within the {industry} right this moment, rejecting the thought of optimizing quantity by compromising on value through the first quarter earnings name:

Very first thing, I might say that from a principal perspective and given the place we’re within the life cycle maturity of our firm, we do suppose it is necessary to steadiness between quantity and value to not optimize one to the detriment of the opposite.

Supply: Lucid 1Q23 Earnings Name Transcript

The mix of demand dangers and slim margin enhancements inside the close to time period regardless of ongoing value optimization efforts implies Lucid stays lengthy methods from attaining profitability. Paired with important capital outlays required to maintain its ongoing development initiatives – spanning abroad enlargement and new automobile R&D – Lucid’s near-term elementary prospects continues to bode unfavourably with the at present unsure market local weather, which harbingers additional volatility to the inventory forward.

Comparatively Overvalued

Regardless of ongoing elementary headwinds in addition to macroeconomic challenges to market circumstances, which has worn out the majority of the Lucid inventory’s worth over the previous 12 months, it nonetheless trades at a premium to its friends at present ranges.

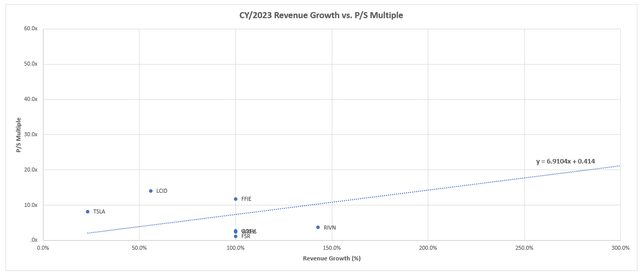

Lucid’s premium to friends regardless of near-term elementary headwinds dangers a downward adjustment amid ballooning uncertainties out there local weather. (Creator, with information from In search of Alpha)

The premium implies that market continues to cost the inventory as if Lucid may double its gross sales inside the subsequent 12 months. In the meantime, the inventory’s quick float of 8% stays considerably decrease than its friends with comparable development profiles, together with Rivian’s (RIVN) near 10% and Fisker’s (FSR) greater than 34%. The mix of market observations underscores resilient traders’ confidence within the inventory regardless of looming macroeconomic challenges and elementary dangers dealing with the underlying enterprise. Admittedly, the inventory’s resilient premium may nonetheless profit additional on the coattails of market tailwinds – particularly as valuation positive factors realized by {industry} chief Tesla may doubtlessly drive multiples throughout the EV sector increased. Nevertheless, we predict dangers stay skewed to the draw back for Lucid as its valuation premium lacks sturdiness, particularly given the underlying enterprise’ difficult elementary outlook and restricted near-term catalysts for driving incremental upsides. Lucid’s present market valuation premium to friends will doubtless topic the inventory to higher vulnerability to a downward rebalancing amongst its peer group valuations.

The Backside Line

Whereas Lucid continues to profit from a technological benefit in addition to broader longer-term secular development traits on the again of the worldwide transition to electrical, its near-term elementary prospects stays blighted by burgeoning execution dangers. The evolving macroeconomic dynamics, although anticipated to be transient, additionally stays a persistent strain that’s weighing on the enchantment of its valuation prospects, that are underpinned by money flows additional out sooner or later. Taken collectively, we anticipate dangers to stay skewed to the draw back inside the foreseeable future for the Lucid inventory, with restricted catalysts to mitigate its publicity from higher volatility in tandem with the broader market forward.