Spencer Platt/Getty Photographs Information

The Labor Division reported Wednesday that the patron worth index (“CPI”) rose at its slowest tempo in additional than two years. Although optimistic, the report isn’t anticipated to alter the result on the Federal Reserve’s July 25-26 assembly.

June CPI Headline Inflation Fee

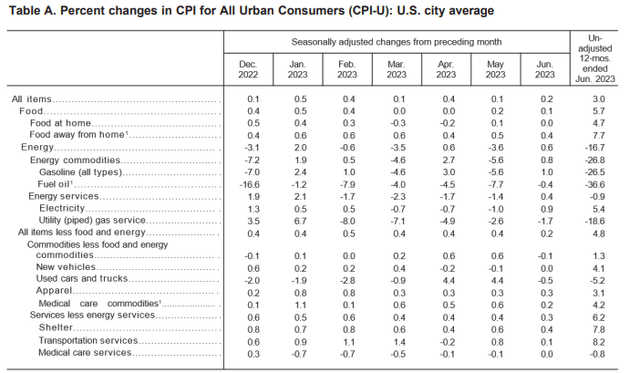

The index rose 3% in June, down from 4% in Could and properly under the current peak of 9.1% in June 2022. Observers must navigate again to March 2021 to see a comparable inflation studying.

For the month, CPI rose 0.2%, additionally under expectations. And core CPI, which excludes risky meals and vitality costs, was 4.8% in June, down from the 5.3% reported in Could.

Just like the topline fee, core CPI has been on a unbroken downtrend since its peak in September 2022. The month-to-month rise in core CPI was additionally the smallest since August 2021.

Market Response To June CPI Report

Shares rose by mid-afternoon buying and selling following the report. Each the Dow (DJIA) and the Nasdaq (NDX) climbed over 100 factors. The S&P 500 Index (SP500) was extra muted. Bond yields moved decrease, with the 10-YR word falling to three.867%.

Inflation Drivers In June

Vitality costs elevated within the month of June as vacationers launched into their summer season journeys. However costs are nonetheless down considerably YOY. The vitality commodities index, which incorporates gasoline and gas oil, is down about 27%. This primarily accounts for the general lower within the headline fee.

BLS – June CPI Report

Transportation providers, then again, are up 8.2%. This is because of car insurance coverage and upkeep/repairs, that are up greater than 4 instances the general CPI, at 16.9% and 12.7%, respectively. To the doubtless dismay of car homeowners, the speed of progress on this class has proven no indicators of slowing. In June, the 2 strains gadgets have been up one other 1.7% and 1.3%, respectively.

A rise in accidents and the related prices, comparable to medical payments and litigation, are driving the bumps in these classes. Losses suffered in pure disasters, comparable to Hurricane Ian, are also offering insurers, comparable to Allstate (ALL), extra trigger to get better their losses. And looking out forward, premiums are anticipated to proceed rising by the tip of 2024, with one other 5% to 10% improve potential, in response to business group Insurance coverage Info Institute.

In a single break to vacationers, airways and automotive/truck leases are every down 18.9% and 12.4% YOY. Flyers notably benefited in June as fares dropped 8.1%. Customers can thank decrease gas costs for the financial savings. Traders ought to count on Delta Air Traces (DAL) CEO, Ed Bastian, to elaborate additional on the pricing and demand setting when the corporate studies outcomes on Thursday.

Associated, however acknowledged individually, drivers and vacationers additionally may cheer decrease costs for used vehicles and vehicles. Following two consecutive months with month-to-month will increase of 4.4%, costs pulled again by 0.5% within the month of June. Based mostly on the Manheim Used Car Index, which reported its largest month-to-month drop in June, the outlook seems promising for additional declines within the months forward. Although new automobiles are nonetheless up 4.1%, the pattern stays optimistic. New costs have been flat in June following declines in April and Could.

Within the grocery aisle, the meals at dwelling index was flat in June following a 0.1% improve in Could. Although the index continues to be up 4.7% YOY, buyers have benefited from declines in key classes. The worth of eggs, for instance, is down 7.9% from final yr.

Within the vegetables and fruit class, costs are up 1.1%. Relying on what one eats, this might both be seen in a optimistic or adverse mild. Whereas potato costs are up 6.5%, with a 0.7% month-to-month improve, citrus fruits are down 5.5%, having declined 2.3% in June. Apples, too, seem like pulling again. Costs right here have been additionally down 2.3% in June.

Will The Fed Enhance Curiosity Charges?

The decline within the CPI to three% is promising. It additionally means that the Commerce Division’s index for personal-consumption expenditures (“PCE”), which can be launched later this month, additionally will report a decline. The anticipated decline within the PCE is vital since it is the Fed’s most popular studying.

Inflation, however, stays above the Fed’s 2% goal. This makes it doubtless that the Fed will improve charges by one other quarter share level once they meet in two weeks. This shouldn’t shock markets as minutes from the Fed’s June coverage assembly indicated that officers have been intending on two extra will increase this yr.

In a single sense, continuation is sensible. Costs in sure classes are proving sticky. The expansion in services-based spending, comparable to consuming out, continues to extend. The related meals away from dwelling class added one other 0.4% in June and is up 7.7% YOY.

Extra regarding is the expansion in costs for insurance coverage and upkeep/repairs. Granted, the general transportation providers index grew at a slower tempo from the prior month, however this was primarily because of the decline within the rental and airfare market.

The remoted strain from insurance coverage and upkeep/repairs, which impacts most Individuals, could show trickier to handle by way of the speed cycle. Losses from main climate occasions have factored in additional materially in current durations. Current flooding within the northeastern U.S. could additional compound this market. And additional fee will increase by the Fed could solely show counterintuitive within the insurance coverage market, since insurers are allowed to recapture their prices by way of elevated premiums.

Shelter additionally creates a complication for the Fed. In distinction with the possible continued stickiness in different classes, the shelter element could deflate extra rapidly than anticipated. In June, shelter prices accounted for 70% of the month-to-month improve in headline CPI.

By one measure, this class, too has proved resistant. June rents, for instance, have been nonetheless up 8.3% YOY, with homeowners’ equal lease up 7.8%, in line with prior months. Zillow’s (Z) not too long ago launched month-to-month rental report, nonetheless, confirmed that rental fee progress has normalized to pre-pandemic ranges.

Extra notably, Senior Economist Jeff Tucker famous in his report {that a} record-high variety of multifamily models have been underneath building in Could. These models will quickly hit the market simply as rental progress has stalled. The added provide, then, ought to start to position downward strain on rents. By Tucker’s estimates, CPI lease progress is predicted to fall to six.4% by December.

The anticipated decline within the rental element could have an outsized impression on total CPI as a consequence of its present weighting. However this can be on a lagged foundation for the reason that CPI metric contains each new and current leases. The inclusion of current leases inherently creates a lag since tenants’ rents sometimes change simply annually.

By transferring ahead with continued will increase, the Fed dangers overshooting key parts whose deceleration is predicted to extend within the again half of the yr. On the identical time, their will increase are unlikely to alter the trajectory on stickier line gadgets, comparable to insurance coverage premiums.

With these concerns in thoughts, I consider the Fed is on observe for a coverage mistake and can doubtless be compelled into pivoting to a fee slicing cycle starting within the first quarter of 2024.