")

Robert Manner

Funding Thesis

I’m bearish on Intel Company (NASDAQ:INTC) regardless of its turnaround initiatives comparable to a change of enterprise mannequin and price management measures. Acknowledged for its built-in circuits and microprocessors, Intel has been integral within the semiconductor sector for a few years. However, latest knowledge and tendencies point out that it won’t be funding in the meanwhile.

My lack of optimism even with the above strategic choices stems from the corporate’s poor financials significantly the excessive debt burden and the yet-to-deliver foundry enterprise. Additional, the aggressive panorama has confirmed a tough sea for INTC to sail in one thing which provides to my skepticism.

A Overview Of Value Motion: A Reflection Of Aggressive Strain

Whereas INTC is current within the majority of PCs, its inventory has not taken half within the latest huge increase marketplace for semiconductor shares.

Searching for Alpha

Since they laid the groundwork for the unreal intelligence increase, semiconductor firms comparable to Broadcom (AVGO), NVIDIA (NVDA), and Taiwan Semiconductor Manufacturing (TSM) have loved monumental rallies within the final yr. Over the previous 12 months, NVidia has soared 146%, Broadcom by 74%, and TSMC by 77%. All these booms have come towards INTC’s greater than 42% hunch not solely underperforming its friends but in addition the general ESOX: IND.

With a market share of about 78% in central processing items, the corporate leads the market, however it’s having problem maintaining with the sorts of semiconductor chips wanted for synthetic intelligence [AI], particularly graphics processing items. This competitors explains why its inventory efficiency has been poor. Its inventory has dropped over 61% yr to this point. In the long run, the stats are much more dismal: Intel is at the moment buying and selling at about $20 per share, down roughly 64% over the past three years.

The Aggressive Panorama: Intel Lags Its Opponents’ Innovation

At the moment, the discuss of the day within the tech business is the AI which is a revolutionary drive. This has taken impact even within the chip market, particularly within the GPU. With this in thoughts, it implies that for Intel to stay aggressive and viable within the business, it has to match and even outdo its rivals within the AI chip market. Quite the opposite, INTC seems to lag behind its rivals within the AI chip market.

When it comes to market dominance, as of 2023, NVDA was the main vendor with a market share of about 92% adopted by a 3% market share of AMD this meant that INTC made a part of the remaining 5%. In keeping with Financial institution of America, INTC has lower than 1% of the AI chip market with NVDA sustaining a better market share at excessive double-digit figures.

IoT Analytics

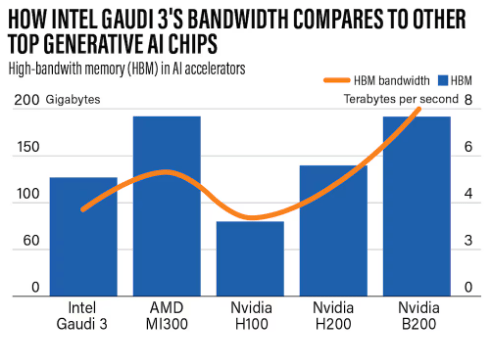

For my part, the corporate’s lack of great market share on this market is its lack of improvements to match its main rivals NVDA and AMD. As an example, in April, INTC unveiled the Gaudi 3, one in all its most revolutionary merchandise. It outperformed NVidia’s H100 GPUs by way of inference and energy effectivity by round 50% and 40%, respectively. Even whereas it seems that this gadget will compete straight with AMD and NVDA, I do not suppose it can current a lot of a menace to its two main rivals.

To start with, Gaudi 3 will not be anticipated to be out there for buy anytime quickly since quantity manufacturing is anticipated to start in Q3 2024. Conversely, NVDA anticipates transport H200 chips in Q3 2024 after finishing mass manufacturing in Q2; furthermore, INTC Gaudi 3 is being matched with H100, which is a technology older contemplating the H200 and B200 merchandise from NVDA and AMD’s MI 300.

IEEE

Given these occasions, it seems to me that INTC is considerably behind its rivals by way of innovation. This places them at a major aggressive drawback and bodes poorly for the efficiency of its inventory.

The Foundry Enterprise Mannequin: Far From Promising

Intel made a strategic shift from its conventional IDM-focused operations to a foundry enterprise mannequin. This transition is consistent with its IDM 2.0 technique, which intends to convey collectively the flexibleness of a foundry service mannequin and the strengths of inside manufacturing capabilities. The purpose of the relocation is to offer shoppers with cutting-edge options by ongoing technological developments and to construct a extra strong, sustainable, and safe provide chain.

The chief monetary officer, Dave Zinsner, states that this mannequin was meant to generate main price reductions, operational efficiencies, and asset worth. They anticipated accelerating to satisfy their 2030 targets of 40% non-GAAP working margins and 60% non-GAAP gross margins.

Whereas this formidable transfer appeared like a recreation changer and maybe a major turnaround technique, the outcomes have been astonishing and much from pleasing. The foundry part reported an astounding working lack of $7 billion in 2023 which was a lot greater than the $5.2 billion reported in 2022.

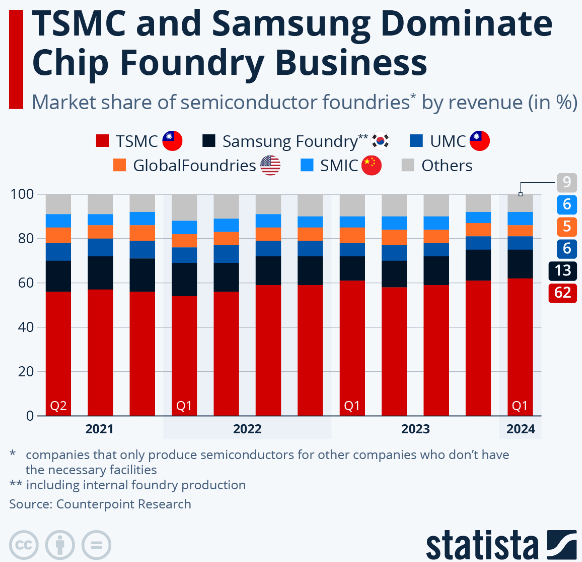

With a whopping internet revenue of $26.88 billion in 2023 in comparison with Intel’s monumental loss, Taiwan Semiconductor Manufacturing, a longtime chief within the foundry business, might be a formidable competitor for INTC which provides to the aggressive woes.

Statista

Within the Q2 2024 report dated 1st August 2024, the foundry’s working loss was $2.8 billion, and the corporate anticipates that working losses will stay roughly the identical in Q3. This terrible trajectory which speaks volumes about how far the brand new mannequin is from profitability and worse sufficient, how far the corporate is from matching its competitor’s profitability milestones.

Why I Consider The Foundry Mannequin May Be Unsustainable

Whereas the mannequin has been characterised by declining revenues from $27.5 billion in 2022 and $18.9 billion in 2023 in addition to the worsening profitability talked about above, I discover it an uphill process for Intel to show this mannequin fruitful, particularly given the competitors highlighted above.

First off, at the moment, Intel’s foundry generates a major quantity of income from inside sources versus exterior shoppers. This reduces the potential of elevated income from rising markets. Whereas the corporate anticipates breakeven in 2027 and realizes exterior income of about $15 billion in 2030, it calls for large investments and improvements to not solely match but in addition exceed competitors. Having stated that, INTC is nearly incapacitated to do that for it requires intensive capital one thing which might stretch what I consider is overstretched debt burden.

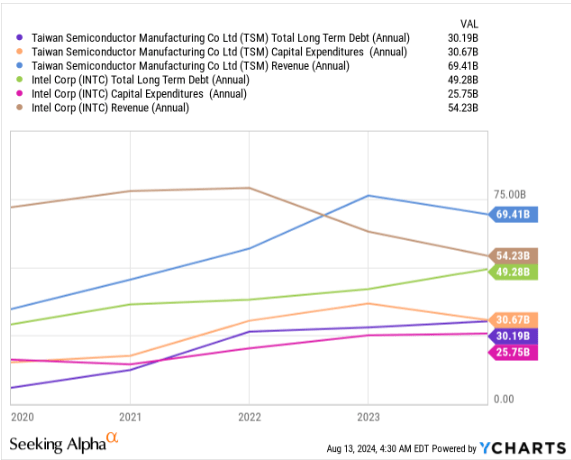

In comparison with TSM a significant foundry competitor, INTC has an annual complete debt of $49.28 billion towards $30.19 billion for TSM. This isn’t solely a better burden than its competitor but in addition very unsustainable contemplating Intel’s low income base in comparison with TSM.

YCharts

Moreover, its debt has elevated considerably over the previous 5 years, practically doubling in simply that point, from $29 billion in 2019 to its present degree. Its $9.77 billion detrimental unlevered money stream additional signifies that the mounting debt is a burden. As a result of its growing debt and insufficient money flows to pay it off, the corporate is unlikely to achieve TSM as a result of funding additional developments and improvements to meet up with rivals could name for added debt which might additional add to what seems as unsustainable debt.

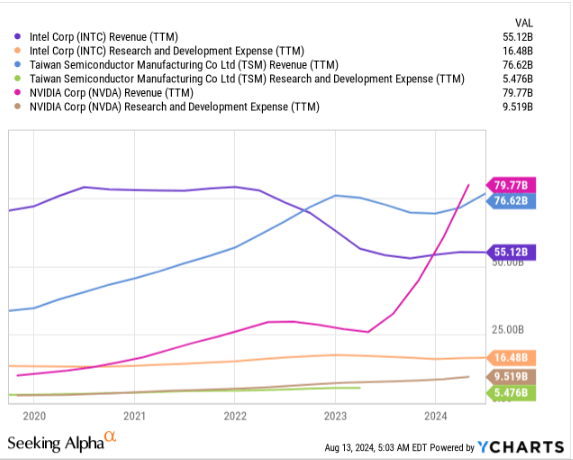

Debt burden apart, I’m involved in regards to the firm’s R&D and Innovation. The company has had a major R&D expenditure, at the moment trailing at $16.48 billion, accounting for about 30% of its income. Regardless of this monumental funding, the company has struggled to show its R&D spending into market-leading merchandise. Opponents, like as NVIDIA and TSM, have been extra profitable in capturing market share and driving innovation regardless of decrease R&D investments than Intel.

YCharts

Conclusion

Whereas Intel remains to be a key participant within the semiconductor sector, a number of causes point out that it will not be funding possibility at this second. Lagging technological developments, excessive debt burden considerations, strategic hurdles, significantly the foundry enterprise mannequin, R&D and innovation points, and underwhelming inventory efficiency all contribute to my bearish outlook for Intel. I consider it additionally explains its 31 EPS and 38 income downward revisions and nil upward revisions which additional inform my promote determination.