")

Justin Sullivan

There are quite a lot of methods to speculate and plenty of extra methods to become profitable available in the market. There are additionally much more methods to lose cash when investing, however one of many key takeaways in our expertise facilities round having a plan when investing. Most individuals give attention to the analysis for the purchase/promote thesis and ignore the method of planning the commerce and understanding their private course of for reaching success. Why go to all of that work on researching to not set your self up for fulfillment?

Each time we take a look at portfolios for putting trades, we make the most of names on our purchase record on the time. Whereas many will argue that if one merely buys on the proper value, then one simply has to buy-and-hold to become profitable, we’ve discovered that to not all the time be the case – as a result of nicely, stuff occurs. Over lengthy durations of time, with sure names, that may maintain true – Warren Buffett has constructed a profession out of it (and that’s an understatement) – however understanding when to promote or your plan for exiting is simply as necessary. Our desire is to have an thought of what we are attempting to perform, not just for your complete portfolio, but in addition for that particular person holding.

This is without doubt one of the key variations between retail buyers and institutional buyers. Not saying that one is best than the opposite, however on the institutional degree there’s extra consideration paid to exit technique and managing threat.

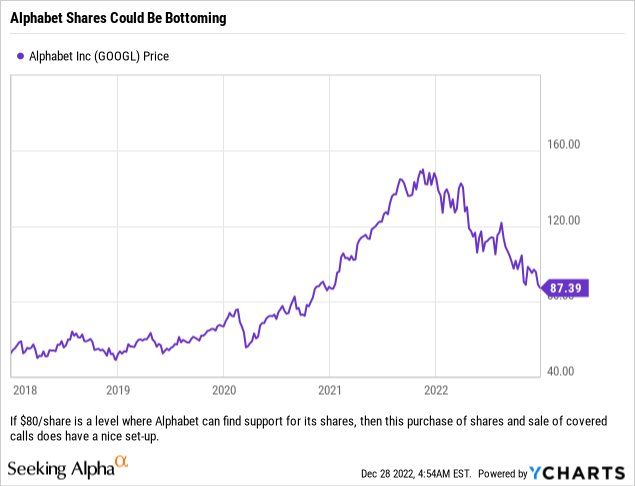

This brings us to yesterday when taking a look at a portfolio that had loads of room (on an allocation foundation) for Alphabet (NASDAQ:GOOGL) (NASDAQ:GOOG) because it has been sitting in principally money currently.

So What Was The State of affairs?

We had been questioned on why Alphabet was included on the buy-list for the portfolio with the potential for additional draw back. By no means thoughts our plan to hold an obese place, however the query centered round proudly owning the title in any respect. Our response was that sure, the market seems to be ugly, the inventory most likely has room to go decrease (particularly if the Fed continues to lift charges) and we almost definitely aren’t buying on the very backside, nevertheless we thought that going obese this title made sense for this specific portfolio, particularly if we utilized the portion we had been going obese to handle threat and higher outline anticipated returns for the portfolio.

So What Was The Plan?

Our considering for 2023 is that will probably be a tough 12 months. The Federal Reserve remains to be elevating charges, and in the event that they proceed to be aggressive, it could be unhealthy information for the market. It will even be unhealthy information for the market if their aggressiveness up so far proves to have been an excessive amount of, too quick, and so they need to shortly pivot. Sure, it could be excellent news that the Fed was carried out elevating charges, however then consideration will shift as to whether the harm is reversible or not. In our expertise, when that query is being requested, the reply is that harm was in truth sustained and that there might be some fallout. We do really feel that the harm won’t be too extreme if it performs out alongside the strains we anticipate, and that the tip of 2023 may very well be respectable for buyers.

Due to this considering, we had no challenge buying Alphabet shares at present costs, as a result of our intent was to concurrently promote coated calls towards many of the place. With the inventory closing the session at $87.39/share, and Alphabet’s historic returns, we thought that for this specific account the right transfer can be to arrange a commerce that will cap positive factors, have the potential to supply outperformance as long as the shares don’t rise sharply and generate a money circulate within the current and primarily hedge our draw back threat.

So What Was The Commerce?

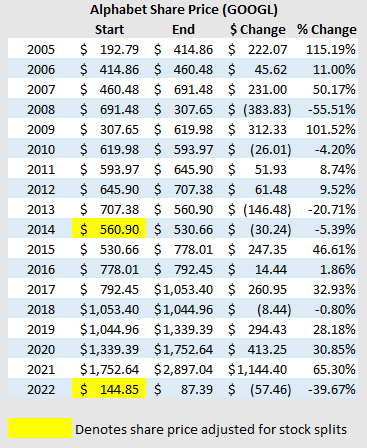

So the shares have to be bought. Utilizing the closing value from yesterday’s session, $87.39/share, we checked out potential returns over the subsequent 12+ months in addition to Alphabet’s historic returns. Beneath are Alphabet’s historic returns:

Historic returns for Alphabet/Google. The common is simply over 20% per 12 months. (Bloomberg)

With the common return being just below 21%, we additionally regarded on the annual returns individually and noticed that 8 out of 18 years Alphabet/Google shares have traditionally had returns over 25%. There are 5 down years additionally, and three occasions after these detrimental years noticed positive factors over 25%, though a kind of years was simply over 28%. The common for these subsequent years following a down 12 months was just below 36%, nevertheless when you pull out the very best and lowest return, you come again to a couple of 28% return.

For this specific account, we favored the January 19, 2024 Calls with a strike value of $100, which primarily based off of closing costs generates an possibility premium of $9.45, or a complete of $945. The choice premium doubtlessly offers the account with simply over 10.81% of outperformance as long as Alphabet’s inventory value doesn’t shut above $100/share. The commerce generates outperformance as long as Alphabet shares don’t commerce above 109.45/share, however most significantly, the commerce is designed to cap positive factors at 25.24% (10.81% from the choice premium and 14.43% from the achieve on the shares) however would offer us with almost 11% of outperformance (as long as the inventory value didn’t rise greater than $12.61/share) and shares can fall $9.45/share earlier than the portfolio can have losses on the place.

Since this account takes much less threat, this commerce is sensible and truly permits the account to get extra publicity to Alphabet as a result of we’ve minimized potential draw back by capping potential upside.

Last Ideas

We get that many Alphabet buyers will most likely hate this commerce because it caps positive factors at a value which appears so shut. Within the case of this portfolio, that 14%+ achieve on the inventory value appreciation can be loads for the account, however throw within the $9.45 possibility premium and the virtually 11% return that gives and this turns into a possible slam dunk for the portfolio. Ordinarily an obese for this portfolio wouldn’t work, however by capping the positive factors, we’re capable of cowl the primary virtually 11% of draw back threat if it happens. And getting upset with a 25%+ return, particularly after this 12 months, can be foolish.

This isn’t an ideal commerce as we’re not shopping for insurance coverage to the draw back to really hedge draw back threat, however with this 12 months wanting prefer it is likely to be the second worst down 12 months on a share foundation for Alphabet in its historical past we predict that almost all of the possible potential draw back threat is roofed by the choice premium generated by the coated name.

We might level out that for another portfolios at this time we are going to almost definitely make the most of the $100, $105 and $110 strikes with September 15, 2023 maturities which have the potential to generate returns of twenty-two.06%, 25.99% and 30.28%, respectively – ought to these positions be known as. These choices is likely to be extra enticing for readers eager to be extra aggressive as they place one to work out that possibility place forward of October (traditionally a unstable month) and leaves November and December (traditionally fairly robust durations) out as nicely…which means one would possibly be capable to pocket the choice premium with out having their shares known as and get to take part in a year-end rally. If known as in September, these returns are respectable…and much more so when annualized.

Remember that choices aren’t for everybody, and capping positive factors to attempt to engineer returns for the general portfolio may not go well with some buyers’ methods, however for this portfolio the commerce works and is a win-win. If in a 12 months shares are flat or down, there’s all the time the potential to arrange one other coated name commerce to generate a major possibility premium.