Printed on January eleventh, 2023 by Jonathan Weber

LyondellBasell Industries (LYB) is a U.S.-based chemical compounds and refining firm that gives a excessive dividend yield of greater than 5% at present costs. Following latest positive aspects, its valuation isn’t ultra-low any longer, however LyondellBasell nonetheless is fairly cheap.

It is likely one of the high-yield shares in our database.

Now we have created a spreadsheet of shares (and intently associated REITs and MLPs, and many others.) with dividend yields of 5% or extra.

You’ll be able to obtain your free full checklist of all securities with 5%+ yields (together with vital monetary metrics reminiscent of dividend yield and payout ratio) by clicking on the hyperlink under:

On this article, we are going to analyze the prospects of LyondellBasell.

Enterprise Overview

LyondellBasell Industries was included in 2009 in its present kind (following a earlier chapter) and is headquartered in Houston, Texas. The corporate is a chemical compounds and refining participant that has organized its operations into six totally different enterprise models: Olefins and Polyolefins—Americas; Olefins and Polyolefins—Europe, Asia, Worldwide; Intermediates and Derivatives; Superior Polymer Options; Refining; and Expertise.

LyondellBasell is energetic in a variety of nations, together with america, the place it has expanded its asset base lately, Mexico, Germany, Italy, France, Japan, China, and several other extra. This geographic diversification helps shield LyondellBasell versus country- or area-specific points reminiscent of Europe’s present power disaster. Whereas operations in international locations reminiscent of Germany or France endure from that, U.S.-based operations profit from advantaged power costs.

LyondellBasell has exhibited enticing enterprise progress lately. Earnings-per-share have risen by 190% over the past decade, utilizing the $14.60 analyst consensus estimate for fiscal 2022 (This fall outcomes haven’t been reported but). There have been ups and downs in LyondellBasell’s earnings-per-share, nonetheless. The corporate is thus not a very regular grower, as a substitute, its outcomes could be cyclical, relying on components reminiscent of crack spreads and demand for sure chemical merchandise.

Supply: LyondellBasell Presentation

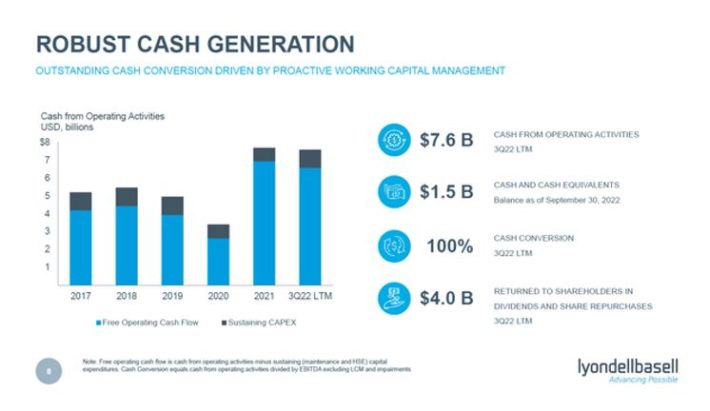

Throughout the newest quarter, Q3 2022, LyondellBasell generated stable, however not spectacular outcomes. Income was down by 3% yr over yr on smooth demand for a few of the merchandise it manufactures, e.g. as a consequence of lockdowns in China. EBITDA and money circulate remained wholesome, nonetheless, and LyondellBasell generated ample free money circulate to pay for dividends, buybacks, and internet debt discount on the identical time.

Supply: LyondellBasell Presentation

Distributable money circulate, or working money circulate minus sustaining/upkeep capital expenditures, totaled round $6.5 billion, which makes for a hefty money circulate yield of greater than 20% at present costs. It’s anticipated that money flows and income will pull again this yr as a consequence of an financial slowdown within the U.S. and another international locations, however that needs to be a short lived pullback solely, as demand for LyondellBasell’s merchandise ought to improve once more as soon as financial progress picks up.

Development Prospects

LyondellBasell isn’t within the fastest-growing business, however the firm experiences stable progress, adjusting for ups and downs within the financial cycle.

Development drivers, in the long term, embody natural investments, such because the spending the corporate has pursued in its U.S. and China enterprise models, because it seeks to increase the place power is affordable. Acquisitions are also a progress driver for LyondellBasell. The corporate acquired A. Schulman a few years in the past in a deal price $2.3 billion.

LyondellBasell additionally has been paying down debt in latest quarters, which ends up in declining curiosity bills, all else equal. Final however not least, LyondellBasell has been an avid purchaser of its personal shares: Between 2012 and 2021, its share rely declined from 570 million to 330 million, which resulted in a powerful earnings-per-share progress tailwind. It’s seemingly that LyondellBasell will proceed to decrease its share rely over time.

2022, and particularly 2021, have been two sturdy years for the corporate because of the advantageous pricing atmosphere for a lot of of its merchandise. It’s anticipated that 2023’s earnings-per-share will decline to round $9.80. From that decrease stage, we imagine that earnings-per-share will rise at a mid-single-digit charge to round $11.50 in 2027.

Aggressive Benefits

The chemical compounds business has excessive boundaries to entry. Constructing out new chemical crops by way of greenfield initiatives is expensive, and there are difficult and prolonged approval processes for that, no less than in lots of the markets LyondellBasell is energetic in, reminiscent of Europe and the U.S.

Which means that few new crops are coming on-line in these markets. Within the refining area, that is much more pronounced — no new refineries have been in-built america for many years. Current belongings thus are priceless and arduous to switch.

On high of that, LyondellBasell advantages from measurement and scale benefits. It’s the largest polypropylene compound producer on this planet, for instance. Its massive mental property portfolio additionally makes it an vital polyolefin applied sciences licensor, permitting it to generate money when friends produce sure merchandise.

Dividend Evaluation

LyondellBasell began to make dividend funds shortly after it emerged from chapter a bit of greater than a decade in the past. Over that time-frame, the corporate has elevated its dividend repeatedly, together with yearly of the final decade.

In these ten years, the dividend went up from $1.45 per share to $4.76 per share, which pencils out to an annualized dividend progress charge of 13%, which is kind of enticing. Dividend progress has been decrease within the final couple of years, nonetheless. Particularly in 2020, when there have been main uncertainties as a result of pandemic, LyondellBasell’s resolution to hike the dividend solely barely so as to stay defensive made sense, which is why there was only a 1% dividend improve in that yr.

With earnings-per-share being forecasted at $9.80 in 2023, the dividend payout ratio stands at 49% at present. 2023 will seemingly be a lot nearer to a backside than a high profit-wise, and but the dividend will needs to be simply lined. This makes us imagine that there’s little danger of a dividend lower when investing in LyondellBasell, though a dividend lower can’t be dominated out.

With LyondellBasell buying and selling for $93 at present, the dividend of $4.76 per share makes for a dividend yield of 5.1%, which is kind of enticing. Together with ongoing dividend progress, though bigger in some years and smaller in others, and an affordable dividend payout ratio, LyondellBasell seems to be like a stable high-yield earnings inventory at present costs.

Remaining Ideas

LyondellBasell’s shares have pulled again from the highs seen final summer time, as they’re at present buying and selling round 20% under the 52-week excessive. This has made its dividend yield rise to a compelling stage of greater than 5%, though it needs to be stated that LyondellBasell was much more enticing in the course of the peak of the market selloff that we noticed in the direction of the top of 2022.

LyondellBasell is valued at round 9 to 10x this yr’s anticipated income proper now. 2023 might be a down yr, however we imagine that there’s a good probability that earnings-per-share will begin to enhance in 2024, because the financial image ought to clear up once more. Primarily based on the truth that LyondellBasell trades at lower than 10x this yr’s earnings, regardless of 2023 seemingly being a trough yr, LyondellBasell seems to be comparatively attractively priced proper right here.

As a result of cyclical nature of the chemical compounds business and the refining enterprise, LyondellBasell is just not an ultra-low-risk alternative. However the dividend seems to be like it’s well-covered for the foreseeable future, and the mixture of a excessive beginning yield and a few progress potential is just not unattractive.

In case you are all in favour of discovering extra high-quality dividend progress shares appropriate for long-term funding, the next Certain Dividend databases might be helpful:

The foremost home inventory market indices are one other stable useful resource for locating funding concepts. Certain Dividend compiles the next inventory market databases and updates them repeatedly:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to help@suredividend.com.